At its 212th meeting held on December 17, 2025, the SEBI Board approved a wide-ranging set of regulatory reforms aimed at simplification, investor protection, and ease of doing business across capital markets. Key decisions included replacing the SEBI (Stock Brokers) Regulations, 1992 with streamlined Stock Brokers Regulations, 2025, cutting length by nearly half and modernising compliance, supervision, and reporting. The Board also approved an overhauled SEBI (Mutual Funds) Regulations, 2026, reducing regulatory bulk while revising expense ratio norms, rationalising brokerage caps, strengthening transparency, and enabling digital-first compliance. Amendments to ICDR Regulations were cleared to address IPO lock-in issues involving pledged shares and to introduce a concise abridged prospectus at the DRHP stage to improve retail investor participation. SEBI further permitted incentives for select investor categories in public debt issues, simplified transfer and credit of securities under LODR Regulations, eased norms for High Value Debt Listed Entities, aligned unclaimed amount timelines with company law, expanded CRA rating scope with safeguards, and took note of the High-Level Committee report on conflict of interest within SEBI.

Securities and Exchange Board of India

SEBI Board Meeting

Press Releases No.84/2025-SEBI | Dated: December 17, 2025

The 212th meeting of the SEBI Board was held in Mumbai today.

The SEBI Board, inter-alia, approved the following:

1. Review of Securities and Exchange Board of India (Stock Brokers) Regulations, 1992

1.1 The Board approved the proposal to replace Securities and Exchange Board of India (Stock Brokers) Regulations, 1992 with Securities and Exchange Board of India (Stock Brokers) Regulations, 2025 (“SB Regulations”) with the objective of

i. Streamlining the regulations to ensure simple and clear language

ii. Omission of repetitive and redundant provisions

iii. Updating regulations with contemporary changes

iv. Modification/inclusion of certain provisions to provide more clarity and to ensure ease of compliance

1.2 Some of the features of new Regulations approved by the Board are as follows:

1.2.1 Reorganisation of the Regulations

a) SB Regulations have been organised into eleven chapters, comprehensively covering critical aspects of the regulatory framework for stock brokers.

b. Some schedules (not required at present) have been altogether deleted and the relevant ones have been integrated as chapters in the regulations to enhance ease of readability and understanding of the regulations

c. Forms for registration will be prescribed by way of a circular, in consultation with the Industry Standard Forum.

1.2.2 The overall structure has been streamlined by deletion of duplicate or repetitive provisions, re-arrangement and consolidation of provisions such as provisions related to underwriting, code of conduct, other activities permitted to stock brokers etc.

1.2.3 Amendments of certain key definitions such as clearing member, professional clearing member, proprietary trading member, proprietary trading, designated director etc. to provide clarity.

1.2.4 Modifications or inclusion of certain provisions to provide for ease of compliance and ease of doing business by enabling provision for joint inspection and maintenance of books of accounts by brokers in electronic form etc.

1.2.5 Rationalisation of the criteria for stock brokers to be identified as qualified stock brokers so that the brokers meeting criteria such as large number of active clients and greater trading volume etc. are covered for enhanced supervision and compliance.

1.2.6 The reporting responsibilities have been changed to account for the stock exchanges as the first line regulators for stock brokers. For example, reporting of non-compliance, furnishing of financial statements, intimation of place of maintenance of books of accounts by stock broker to stock exchange.

1.2.7 Removal of obsolete and non-applicable historical provisions such as provisions pertaining to physical delivery of shares, Forward Market Commission sub-brokers etc.

1.2.8 Drafting has been done to enhance ease of reading and understanding.

1.2.9 Total pages have been reduced from existing 59 pages to 29 pages.

1.2.10 Total words count has been reduced from existing 18846 words to 9073 words.

The SB regulations are expected to enhance ease of compliance by ensuring simplified language and overall structured provisions, updated with the continually evolving compliance requirements.

SEBI earlier had issued a discussion paper on August 13, 2025 soliciting public comments for reviewing SEBI (Stock Brokers) Regulations, 1992, The overhauled SB regulations have factored in the suggestions received in the public consultation.

2. Comprehensive review of SEBI (Mutual Funds) Regulations, 1996

2.1 The SEBI Board, at its meeting held on December 17, 2025, approved the changes proposed, pursuant to the review of the SEBI (Mutual Funds) Regulations, 1996. The new SEBI (Mutual Funds) Regulations, 2026, are designed to offer stakeholders greater clarity, improved readability, and enhanced structural coherence. While simplifying compliance, the revised framework retains the core principles, safeguards, and regulatory intent built over the years, and further strengthens investor protection, transparency, and governance standards within the mutual fund ecosystem.

2.2 For nearly three decades, the SEBI (Mutual Funds) Regulations, 1996 have served as the foundational regulatory architecture for the Indian mutual fund industry. Over time, multiple amendments were incorporated to address evolving market practices, resulting in an extensive and layered regulatory structure.

2.3 Some of the key features of the SEBI (Mutual Funds) Regulations, 2026 are:

A. Simplification and consolidation

The restructuring emphasises on clearer structure and simplified language, consolidation of related provisions and removal of overlapping clauses. Key restructuring measures include:

i. Streamlined eligibility criteria for sponsors of Mutual Funds and Mutual Fund Lite, presented in a consolidated, easy-to-reference format.

ii. Reorganisation of roles and responsibilities of AMCs and Trustees under common thematic headings for greater clarity.

iii. Reorganisation of provisions related to the prudential investment limits and valuation of securities for consolidation and ready reference.

B. Transparency and strengthening investor protection

A major component of the review is the revision of the Expense Ratio framework, with the following key measures:

i. Clarity on statutory levies

-

- Expense ratio limits, now called Base Expense Ratio (BER), shall exclude all statutory levies.

- Statutory and regulatory levies such as STT/CTT, GST, Stamp Duty, SEBI Fees, Exchange Fees, etc., incurred for execution of trades shall be charged on actuals, over and above permissible brokerage limits.

- Total Expense Ratio shall now be the sum of BER, brokerage, regulatory levies and statutory levies.

- The revised base expense ratio limits are as indindicated below:

>Index funds/ Exchange Traded Funds (ETF):

Current (including statutory levies)-1.00%

Revised (excluding statutory levies)– 0.90%

>Fund of Funds (FoFs):

- Investing in liquid schemes/index funds/ETFs

Current (including statutory levies)- 1.00%

Revised (excluding statutory levies)– 0.90%

- Investing >65% of AUM in equity oriented schemes

- Current (including statutory levies)- 2.25% Revised (excluding statutory levies)– 2.10%

- Other FoFs

- Current (including statutory levies)- 2.00%; Revised (excluding statutory levies)– 1.85%

- Other open ended schemes:

| AUM slab (in crore) | Equity oriented schemes | Other than equity

oriented schemes |

||

|

Upto 500 500- 750 |

Current (including statutory levies)

2.25% 2.00%

|

Revised (excluding statutory levies)

2.10% 1.90%

|

Current (including statutory levies)

2.00% 1.75%

|

Revised (excluding statutory

levies) 1.85% 1.65%

|

–

| AUM slab (in crore) | Equity oriented schemes | Other than equity oriented schemes | ||

| Current (including statutory levies) | Revised (excluding statutory levies) | Current (including statutory levies) | Revised (excluding statutory levies) | |

| 750-

2,000 |

1.75%

|

1.60%

|

1.50%

|

1.40%

|

| 2,000-

5,000 |

1.60%

|

1.50%

|

1.35%

|

1.25%

|

| 5,000-

10,000 |

1.50%

|

1.40%

|

1.25%

|

1.15%

|

| 10,000-

15,000 |

1.45%

|

1.35%

|

1.20%

|

1.10%

|

| 15,000-

20,000 |

1.40%

|

1.30%

|

1.15%

|

1.05%

|

| 20,000-

25,000 |

1.35%

|

1.25%

|

1.10%

|

1.00%

|

| 25,000-

30,000 |

1.30%

|

1.20%

|

1.05%

|

0.95%

|

| 30,000-

35,000 |

1.25% | 1.15% | 1.00% | 0.90% |

| 35,000-

40,000 |

1.20% | 1.10% | 0.95% | 0.85% |

| 40,000-

45,000 |

1.15%

|

1.05%

|

0.90%

|

0.80%

|

| 45,000-

50,000 |

1.10% | 1.00% | 0.85% | 0.75% |

> Close ended schemes-

-

- Equity oriented schemes-

- Current (including statutory levies)– 1.25%

- Revised (excluding statutory levies)– 1.00%

- Equity oriented schemes-

- Other than equity oriented schemes-

- Current (including statutory levies)– 1.00% Revised (excluding statutory levies)- 0.80%

Note: The base expense ratio thresholds proposed for equity oriented schemes in the consultation paper dated October 28, 2025 (i.e. for slabs with AUM of INR 2,000 crores and above) have been revised upwards to limit the impact on cost structure of AMCs broadly to the extent of exclusion of statutory levies from the base expense ratio limits.

ii. Rationalisation of brokerage limits

-

- Cash market transactions: The existing brokerage cap of 12 bps includes statutory levies. The cap on brokerage, net of statutory levies amounts to 8.59 bps, which has now been reduced to 6 bps (exclusive of levies).

- Derivative transactions: The existing brokerage cap of 5 bps includes statutory levies. The cap on brokerage, net of statutory levies amounts to 3.89 bps, which has now been reduced to 2 bps (exclusive of levies).

iii. Removal of additional expense allowance

Additional 5 bps currently permitted to be charged to schemes with exit loads as a transitory measure, has now been removed.

C. Ease of Compliance

The new regulatory framework aims to simplify operational and compliance requirements through:

i. Rationalization of reporting requirements such as fewer annual trustee meetings and removal of separate half-yearly portfolio disclosures.

ii. Elimination of duplicative filings such as discontinuation of separate filing of trustee transactions under the Mutual Fund Regulations as Mutual Fund units are now covered under SEBI (Prohibition of Insider Trading) Regulations, 2015.

iii. Digital-first disclosures such as discontinuation of physical submission of advertisements to SEBI following automation of online monitoring and email/SMS communication and website disclosures in place of newspaper advertisements.

iv. Streamlined borrowing framework such as enabling borrowing by equity-oriented index funds and equity-oriented ETFs for execution-related needs, and clarifying the permissibility of intra-day borrowing mechanisms to manage redemption-related timing mismatches.

D. Deletion of redundant chapters/clauses such as the chapters on Real Estate Mutual Funds and Infrastructure Debt Fund schemes, as separate frameworks for such products already exist.

2.4 Impact of the review:

The exercise has resulted in a 44% reduction in the size of the regulations from 162 pages to 88 pages. The word count has been reduced by approximately 54%, from 67,000 words (including footnotes) in the current regulations to 31,000 words in the new draft. Further, the number of provisos have been reduced from 59 to fewer than 15 and all ‘notwithstanding’ clauses have been eliminated, except for its limited use under the ‘Repeal and savings’ provision. This restructuring is expected to improve readability and ease regulatory compliance.

2.5 SEBI conducted a stakeholder survey through the Association of Mutual Funds in India (AMFI) to identify regulatory provisions that may require a review. Based on industry feedback and internal analysis, a consultation paper including the draft SEBI (Mutual Funds) Regulations was issued in October 2025 for public comments. Thereafter, the proposals were placed before the Mutual Fund Advisory Committee in November 2025 for deliberation. The feedback received was duly examined, and relevant changes were incorporated and placed before the Board for consideration.

3. The Board approved the amendments to SEBI (ICDR) Regulations, 2018 to streamline certain requirements relating to public issue to enhance ease of doing business and increase the engagement and participation of retail investors

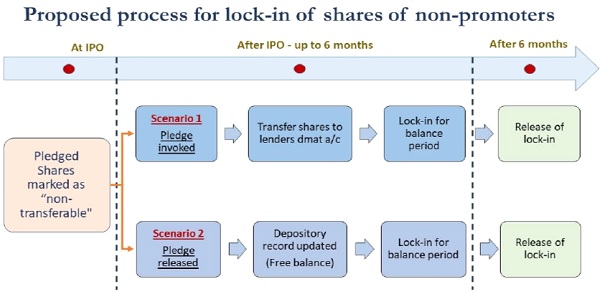

3.1 In terms of ICDR Regulations, the entire pre-issue capital held by persons other than the promoters, except shares held by certain specified categories of shareholders, is required to be locked-in for a period of six months from the date of allotment in the IPO. Certain issuers face challenges in complying with such lock-in requirements, particularly in cases where pledges have been created by non-promoters prior to the IPO. In this regard, the Board has approved amendment to ICDR to prescribe that in case lock-in of the specified securities cannot be created, the depositories shall record such securities as “non-transferable” for the duration of the applicable lock-in period. The depositories through their system shall ensure that, subsequent to the invocation or release of pledge, the shares in the account of the beneficiary (pledger or pledgee) shall automatically be locked-in for the balance period, as required under the ICDR Regulations. The new procedure will ensure compliance with the requirement of lock-in of certain shares even when they are pledged.

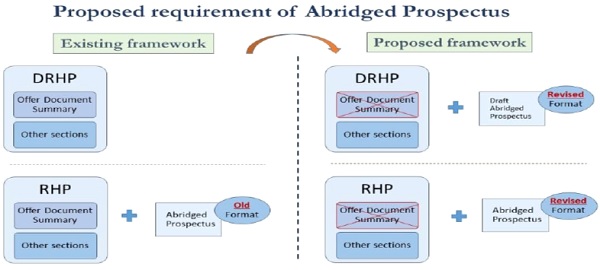

3.2 As per the existing provisions, all material aspects of the public issue are required to be disclosed in the draft offer document (DRHP) and offer document (RHP). The key disclosures relating to the public issue are dispersed across multiple sections. In order to increase the engagement and participation of the retail investors in the IPO process, the Board has approved that a focused, concise and standardized summary of offer documents in the form of draft abridged prospectus shall be available at the DRHP stage as well, in addition to the current requirement of filing of abridged prospectus at the RHP stage. Board has also approved the proposal to rationalise the disclosures in the abridged prospectus. The abridged prospectus shall be hosted on the websites as required under these regulations. With the availability of abridged prospectus, the requirement to prepare an offer document summary may be dispensed with in consultation with the Central Government.

3.3 These amendments are expected to streamline the requirements with respect to fund raising and enhance ease of doing business. Further, the rationalisation of information in abridged prospectus and also making it available with the DRHP is expected to enhance investor comprehension, improve information accessibility and thereby increasing the engagement and participation of retail investors in the IPO process.

3.4 The aforementioned proposals were deliberated in the Primary Markets Advisory Committee and have factored in the feedback received on the public consultation undertaken in November, 2025.

4. Permitting debt issuers to offer incentives in public issues to certain category of investors

4.1 With a view to enhance participation of retail investors in corporate debt market and also to encourage public issuances in the debt market, the Board considered and approved a proposal for amending SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (“NCS Regulations”) to permit debt issuers to offer incentives to certain categories of investors.

4.2 Currently, issuers of debt securities are not able to offer incentive to any persons for making an application in the issue, except for fees or commission for services rendered in relation to the issue.

Pursuant to this amendment, issuers of debt securities will be able offer incentives in the form of additional interest or a discount to the issue price to certain categories of allottees, viz. senior citizens, women, armed forces personnel namely, serving and retired defense personnel and widows and widowers of such personnel, retail individual investors or any other category of investors as may be specified by the Board from time to time. Such incentive shall be available to the initial allottee only and shall not be available in case the debt securities are transferred/ transmitted post allotment. This is expected to increase participation of retail investors and thereby encourage public issuance of debt securities.

4.3 This proposal was made after public consultation undertaken vide consultation paper issued on October 27, 2025 and based on the recommendations of the Corporate Bonds and Securitization Advisory Committee of SEBI.

5. Amendment to Regulation 39 and 40 of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015

5.1 The Board approved the proposal for amendments to Regulations 39 and 40 of the Securities and Exchange Board of India (Listing Obligations and

Disclosure Requirements) Regulations, 2015 (‘LODR Regulations’).

5.2 Details of these proposals are as under:

(i) Amendment to regulation 39 of LODR Regulations for dispensing with Letter of Confirmation (‘LOC’)- Pursuant to processing of investor service requests such as issuance of duplicate securities certificate, transmission, transposition, claim from unclaimed suspense account and corporate actions currently RTAs/listed companies issue LOC to investors. LOC acts as a confirmation of the service request and gives the investor the right to approach Depository Participant (‘DP’) to get credit of securities to his demat account. Accordingly, LOC is submitted by the investor to the DP to get credit of securities to his demat account. This entire process generally takes approximately 150 days from the date of submission of service request.

In order to simplify this process, the Board has approved the proposal to do away with requirement of issuance of LOC by RTAs/listed companies to investors and to effect direct credit of securities in demat account of the investor after due diligence, pursuant to investor service requests as mentioned above.

The proposed changes will streamline the process of credit of securities to investor’s demat account and also reduce timeline of credit of securities to investor’s demat account from existing approximately 150 days to 30 days. It will also reduce the risk of loss and pilferage of LOC and thus will enhance investor convenience.

(ii) Amendment to Regulation 40 of LODR Regulations for facilitating

Transfer of Physical Securities- Transfer of securities held in physical mode was discontinued with effect from April 01, 2019. Subsequently, it was clarified that transfer deeds lodged prior to above deadline and rejected / returned due to deficiency in the documents may be re-lodged with requisite documents till March 31, 2021.

Based on representation from investors and market participants, it was learnt that many investors had missed the above deadlines and could not get the securities transferred in their name. In order to facilitate such investors, as a first step, a special window was opened from July 07, 2025 to January 06, 2026 to allow re-lodgement of transfer deeds which were executed and lodged prior to the above deadline of April 01, 2019.

However, it is learnt that there are still many investors who had purchased physical securities before the deadline of April 01, 2019, but could not get the securities registered in their name, as they had not lodged the transfer deeds within the prescribed timelines.

In this regard, the Board approved the proposal to allow the investors holding original physical security certificates along with the transfer deed through which securities were purchased before April 01, 2019, to lodge such transfer deeds along with original share security certificates. Such lodgement shall be permitted during a specified window and shall be subject to such condition as may be specified by the Board. This would also be subject to necessary due diligence by RTAs/listed companies. Cases involving disputes/frauds will be excluded from the above window. For clarity with regard to applicability of this proposal, below matrix may be referred to:

| Execution Date of Transfer Deed |

Lodged before 01-04-2019? | Original Share Certificate Available? |

Allowed in the proposed window? |

| Before 01-04-2019 | No (it is fresh lodgement) | Yes | ✔ |

| Before 01-04-2019 | Yes

(it was rejected/ returned earlier) |

Yes | ✔ |

| Before 01-04-2019 | Yes | No | ✘ |

| Before 01-04-2019 | No | No | ✘ |

The proposed changes are expected to ensure ease of investing and restitute right to property of investors.

The amendments are based on the recommendations of a SEBI-constituted Panel of Experts and deliberations in the Industry Standards Forum of RTAs. Public consultation was undertaken in October 2025 and the approved changes incorporate stakeholder feedback.

6. Aligning the timeline for transfer of unclaimed amount by an entity having listed non-convertible securities with Companies Act

6.1 With a view to facilitating ease of doing business, the Board approved the proposal for amending the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (LODR Regulations), on aligning the timeline for transfer of unclaimed interest/ dividend/ redemption payment entities having listed non-convertible securities to the Investor Education and Protection Fund (IEPF)/ Investor Protection and Education Fund (IPEF), as the case may be with Companies Act provisions.

6.2 Presently unclaimed amounts are transferred to IEPF/ IPEF after 7 years of remaining unclaimed. To enable ease of doing business, issuers of non-convertible securities will now need to transfer the unclaimed amounts only once after completion of 7 years from the date of maturity of the security instead of multiple transfers when interest/ dividend/ redemption payment becomes due. This will also be beneficial for investors as they would have a longer time frame for claiming unclaimed amounts from the issuer.

6.3 The proposal was made after public consultation was undertaken vide consultation paper issued on October 24, 2025 and based on the recommendations of the Corporate Bonds and Securitization Advisory Committee (CoBoSAC) of SEBI.

7. Measures for regulation of activities of Credit Rating Agency

7.1 With a view to enable ease of doing business, the Board considered and approved the proposal of amending SEBI (Credit Rating Agencies) Regulations, 1999 to enable CRAs to carry out rating of financial instruments falling under the purview of other financial sector regulator (FSR) even in the absence of any rating guidelines by respective FSR.

7.2 Presently, CRAs rate bank loans under RBI guidelines but are constrained from rating unlisted debt securities/instruments due to lack of explicit rating guidelines. Enabling these ratings would ensure availability of ratings for wider set of financial instruments and would be beneficial for the development of overall debt market.

7.3 In order to provide appropriate safeguards for rating of financial instruments falling under the purview of other FSR, the Board approved the following safeguards:

a. Clear segregation and labelling of SEBI regulated instruments and instruments regulated by other FSR in rating reports and press releases.

b. Separation of disclosures on website and advertising/marketing material.

c. Clear upfront disclosures to new clients and written intimation to existing clients with regard to activities under the purview of other FSR

d. Clear disclosures that the SEBI investor protection mechanisms will not be available for activities falling under the purview of other FSR.

e. Net worth stipulations, if any, by other FSR shall be over and above the net worth mandated by SEBI.

f. Separation of Email IDs for handling grievances of activities falling under regulatory purview of different FSRs

7.4 The proposal to the Board was made after public consultation undertaken vide consultation paper issued on July 30, 2025, and based on the recommendations of the Corporate Bonds and Securitization Advisory Committee of SEBI.

8Relaxation in the threshold for identification of High Value Debt Listed Entities (HVDLEs) and measures facilitating ease of doing business for HVDLE including provisions relating to Related Party Transactions

8.1 Presently, HVDLEs are identified as having outstanding non-convertible debt of Rs.1000 crore or more. With a view to facilitate ease of doing business, the Board approved a proposal to relax the threshold for identification of HVDLEs to companies having outstanding non-convertible debt of Rs.5000 crore. This will make it easier for regulated entities like NBFCs, HFCs, ARCs, insurance companies and REITS to raise funds through corporate bond issuance.

8.2The Board also approved proposals to align Corporate Governance (CG) norms applicable for HVDLEs with recent amendments to CG norms applicable to equity listed entities, by way of amending SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 with a view to facilitate ease of doing business. Key amendments are highlighted as under:

8.2.1 Change in financial terminology used for defining Material Subsidiary Thresholds: The term ‘income’ has been substituted by the term ‘turnover’ in Regulation 62L(1).

8.2.2 Board of Directors and Committees:

i. For continuation of directorship of Non-executive director beyond the age of 75 years, prior approval of shareholders by way of special resolution would be required before the director crosses the age of 75 years.

ii. Time taken for regulatory, statutory or government approvals will be excluded from the timeline specified for obtaining shareholder approval for appointment or reappointment of director of a HVDLE.

iii. There will be exemption from obtaining shareholder approval for nominee directors of financial sector regulators or Debenture Trustee or those appointed by Court or Tribunal.

iv. A timeline of 3 months has been provided to fill up vacancies in Board Committees.

v. Recommendations of the Board to the shareholders should specifically include rationale of the board of directors.

8.2.2.1 Subsidiary related compliance requirements: Exemption has been given from the requirement of approval of shareholders for sale of assets of a material subsidiary to another subsidiary, as long as the assets are within the group.

8.2.2.2 Relaxations from compliance requirements due to IBC framework: Additional time has been provided by permitting three months for filling up the vacancy of KMPs subject to having at least one full-time KMP for companies coming out of corporate insolvency resolution process (CIRP) to ensure compliance with LODR.

8.2.2.3 Secretarial Audit and Secretarial Compliance Report: Provisions have been introduced relating to appointment, reappointment, removal and disqualifications for Secretarial Auditor of HVDLE.

8.2.2.4 Related Party Transactions (RPTs): The provisions related to RPTs have been harmonized with equity listed companies by cross referencing of provisions of Regulation 23 in Regulation 62K of LODR while retaining the requirements of obtaining NOC of Debenture trustee and the debenture holders.

8.3 The above proposals to the Board were made after public consultation undertaken vide consultation paper issued on October 27, 2025 and based on the recommendations of the Corporate Bonds and Securitization Advisory Committee (CoBoSAC) of SEBI.

9. Report of the High-Level Committee on conflict of interest, disclosures and related matters in respect of Members and Officials of SEBI

9.1 The Board at its meeting held on March 24, 2025 had approved constitution of a High-Level Committee to undertake a comprehensive review of the provisions relating to conflict of interest, disclosures and related matters in respect of Members and Officials of SEBI.

9.2 Accordingly, a High-Level Committee (“HLC” or “Committee”) was set up by SEBI in April 2025 under the Chairmanship of Shri Pratyush Sinha, former Chief Vigilance Commissioner. The Committee submitted its report to the SEBI Chairman on November 10, 2025.

9.3 The Report of HLC and its recommendations were placed before the Board for its consideration. The Board acknowledged the comprehensive review carried out by HLC.

9.4 The Board expressed the need to have detailed discussion on the recommendations in the ensuing meeting keeping in view the public and media comments, certain concerns expressed by employees, operational modalities and the way forward.

Mumbai

December 17, 2025