♦ Introduction:

We are witnessing massive amount of foreign funds coming into India especially through investments into Start-ups. The government is also encouraging foreign investment through different incentives like liberalising FDI limit in various sectors.

However, due to lack of awareness, often start-ups fail to comply with FEMA and RBI regulations with respect to Foreign investments and as a result, they end up paying late fees and penalties for delayed filing and contraventions.

One of such important compliance to be adhered to while receiving foreign funding in the form of Equity Instruments is filing of Form FC-GPR (Foreign Currency- Gross Provisional Return) with RBI

In this article, we shall explain about the process of filing FCGPR, timelines to be adhered, common mistakes made while filing FC-GPR and consequences of late filing and other contraventions.

♦ When is FC-GPR required to be filed and its due date?

An Indian company issuing equity instruments to a person resident outside India and where such issue is reckoned as Foreign Direct Investment, defined under the rules, shall report such issue in Form FC-GPR within 30 days from the date of issue of equity instruments

♦ Procedure for Filing:

- Create the Entity user id and update entity master (Complete FAQ’S for the same are available on the https://firms.rbi.org.in/firms/ portal)

- Register for Business user from FIRMS portal

- Log into FIRMS à Navigate to SMF tab (Single Master Form) à Choose Form FCGPR

- Fill the required details and submit the form

♦ List of documents required while filing FC-GPR:

- FIRC- to be obtained from the bank where the funding is received

- KYC- to be obtained from the bank where the fund is received

- Memorandum of Association (MOA)- signed by the authorised director

- Board Resolution- filed with ROC for allotment of shares

- List of allottees – filed with ROC for allotment of shares

- Valuation certificate- by SEBI registered valuer/ Chartered Accountant/ Cost Accountant

- CS certificate- in format as specified in notification no. FEMA/20(R)/ 2017-RB

- CA/ CS Declaration- on terms of Equity instruments issued

- Declaration by the Authorized Representative (Director)

♦ Points to remember:

- Amount mentioned in FIRC shall match with the total consideration against which the shares are allotted, any excess amount received shall be refunded

- Date of KYC should be after the date of remittance

- Nature of issue shall be correctly mentioned in the FIRC

- The nature of allotment (e.g. private placement) shall be specified in the board resolution and CS certificate

- The post-transaction foreign share holding pattern shall match with the actual shareholding pattern

- Issue price shall be equal to or above value per share determined as per valuation report

♦ Other Compliances to be adhered to:

- Foreign Liabilities and Assets Annual Return (FLA Return) is required to be submitted by all the India resident companies which have received FDI and/ or made overseas investment in any of the previous year. The same has to be filed before 15th July of the next financial year

- Statement of Specified Financial Transactions (SFT) is a required to be filed by companies receiving amount of more than Rs.10 lakhs against issue of shares. The statement needs to be furnished within 31st May of next year for the financial year in which the transaction occurs

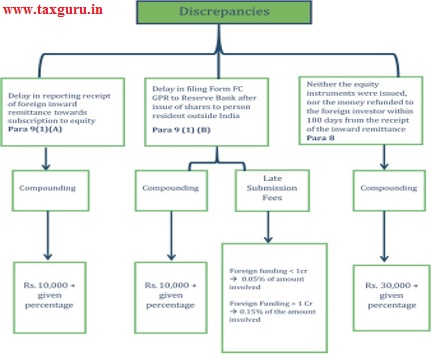

♦ Discrepancies while filing Form FCGPR:

Authors:

CA Shreyans Dedhia |Partner| Email: shreyans.dedhia@masd.co.in

Anuj Pai | Associate Consultant |Email: anuj.pai@masd.co.in

Sutishna Dhanuki | Associate Consultant|Email: sutishna.dhanuki@masd.co.in

Author Bio

In this Article on Forms to be filed when Foreign equity funds are received, under other compliances to be adhered to, it’s mentioned that statement of SFT to be filed. Form 61A demands PAN # of the investing company. When the investing Foreign company does not have a PAN in India, what’s the alternative? Form 60 is applicable only to an individual (non company or firm).

Hi Sir,

You are correct, Form 60 is applicable only to individuals.

Thus, as a practice, we file Form 61 directly in case of corporates not having PAN and categorise them under “Entities exempt under Rule 114b” in the dropdown list.

Hi Sir, You are correct, Form 60 is applicable only to individuals.

Thus, as a practice, we file Form 61 directly in case of corporates not having PAN and categorise them under “Entities exempt under Rule 114b” in the dropdown list.