The RBI had clarified via its circular no. DBR.No.BP.BC.34/21.04.132/2016-17 dated 10 November. 2016, “Schemes for Stressed Assets-Revisions”, that the standstill clause only applies to asset clarification and banks shall not recognize income on accrual basis if the interest is not serviced within 90 days from the due date. However, ‘stand still’ account classification benefit remains at 18 months from the reference date for SDR scheme and 180 days for S4A scheme. This will have adverse impact on the financial statement of the Bank if earlier they are recognizing the income by considering asset clarification norms.

Let us have a brief understanding on S4A and SDR Advances:

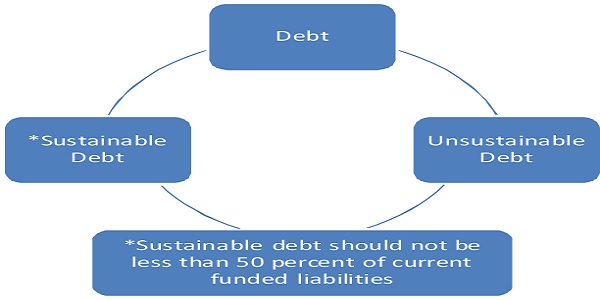

WHAT IS S4A (Scheme for Sustainable Structuring of Stressed Assets)

Under this scheme, large ticket loans are restructured by separating a sustainable loan from an unsustainable loan. The lenders are required to make this classification.

Sustainable level of debt is one which the banks think the stressed borrower can service with its current cash flows.

Banks can convert the unsustainable debt into equity or equity related instruments, which are expected to provide upside to the lenders in case the borrower cannot regain the glory and rework the financial structure.

Eligible criteria for Scheme for Sustainable Structuring of Stressed Assets

As per the PARA 4 of RBI Circular DBR.No.BP.BC.103/21.04.132/2015-16 dated June 13, 2016, the project must be operating and already generating cash. The aggregate exposure (including accrued interest) of all institutional lenders in the account is more than Rs.500 crores (including Rupee loans, Foreign Currency loans/External Commercial Borrowings,)

As per the PARA 5 of RBI Circular DBR.No.BP.BC.103/21.04.132/2015-16 A debt level will be deemed sustainable if the Joint Lenders Forum (JLF)/Consortium of lenders/bank conclude through independent techno-economic viability (TEV) that debt of that principal value amongst the current funded/non-funded liabilities owed to institutional lenders can be serviced over the same tenor as that of the existing facilities even if the future cash flows remain at their current level. For this scheme to apply, sustainable debt should not be less than 50 percent of current funded liabilities

What is SDR

The SDR scheme which was introduced by the RBI in June 2015 thus helps banks recover their loans by taking control of the distressed listed companies.

he SDR an initiative can be taken by the group of banks or JLF that have given loans to the particular defaulted entity. The Joint Lender Forum (JLF) is a committee comprised of the entire bankers who have given loans to a potentially stressed or stressed borrower.

CONDITIONS

- At the time of initial restructuring, the JLF must incorporate an option in the loan agreement to convert the entire or part of the loan including the unpaid interest into equity shares if the company fails to achieve the milestones and critical conditions stipulated in the restructuring package.

- This option must be corroborated with a special resolution since the debt-equity swap will result in dilution of existing shareholders.

- Such a mandate will result in the lenders acquiring a majority (51%) ownership.

- “If the company fails to achieve the milestones stipulated in the restructuring package, the decision of invoking the SDR must be taken by the JLF within thirty (30) days of the review of the account during the restructuring.

- The JLF must approve the debt to equity conversion under the Scheme within ninety (90) days of deciding to invoke the SDR.

- The JLF will get a further ninety (90) days to actually convert the loan into shares.

(Author can be contacted @Deepakrathore.8888@gmail.com)

Author Bio