The Concept of Donating to Political Party is an incentive to encourage transparency in Political Funding and to participate in the Political Process. Simultaneously eligible assessee may claim a tax deduction for such donations u/s 80GGC and 80GGB respectively. However, there are lot of nitty gritty regarding Donations. Let’s delve deeper into this deduction:

KEY POINTS OF 80GGB AND 80GGC

Eligible Assessee:- Indian Companies u/s 80GGB( subject to section 182 of companies act 2013) and any person other than Indian companies, local authority and artificial juridical person wholly or partly funded by the government u/s 80GGC.

Deductible amount: Assessee can Contribute in more than one Political Party in a Financial Year and claim 100% of the total amount donated to political parties as a deduction.

Meaning of Contribution u/s 80GGB- The explanation to section 80GGB provides that the word contribution shall have the meaning assigned to it u/s 182 of the companies act, 2013.

[The Companies Act, 2013, restricts political donations by companies to a maximum of 7.5% of the average net profit of the preceding three years. However 80GGB is not applicable for Govt. Companies and Companies are in existence for less than 3 Years]

Graphite India Ltd. vs. Dalpat Rai Mehta: Final Judgment _ Case Summary[Can a company legally donate to a political party?]

Parties: Graphite India Ltd. (Company) vs. Dalpat Rai Mehta (Shareholder)

Court: Calcutta High Court

Year: 1978

Case Number: [1978] 48 Comp. Cas. 683 (Cal.)

Issue: The primary issue in this case was whether a company could legally donate to a political party. The shareholder, Dalpat Rai Mehta, objected to Graphite India Ltd.’s expenditure on advertisements in All India Congress Committee Souvenirs, arguing that it constituted a political contribution, violating Section 293A of the Companies Act, 1956.

Court’s Ruling: The Calcutta High Court ruled in favor of the company, holding that a company can indeed make donations to political parties under certain conditions:

Shareholder Approval: The decision to donate must be approved by the shareholders at a general meeting.

Bona Fide Business Purpose: The donation should be made for a genuine business purpose, such as promoting the company’s interests or enhancing its public image.

Reasonable Amount: The amount donated should be reasonable and not excessive.

The court emphasized that the primary purpose of the donation should be to benefit the company, not to support a political party. If the donation is primarily for political purposes, it would be considered a violation of Section 293A.

Significance: The Graphite India case established important guidelines for companies seeking to engage in political activities. It clarified that while companies can donate to political parties, they must do so within the bounds of the law and for legitimate business reasons. The case has been cited as a precedent in subsequent cases involving corporate political donations.

In conclusion, the court’s final judgment in Graphite India Ltd. vs. Dalpat Rai Mehta allowed companies to make political donations under specific conditions, ensuring that such donations are made for genuine business purposes and with the approval of shareholders. This ruling has had a significant impact on corporate political activities in India.

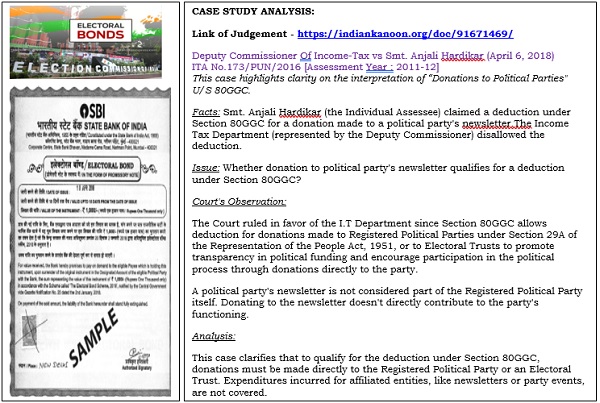

Meaning of Contribution u/s 80GGC-Unlike section 80GGB, section 80GGC doesn’t define the word contribution, therefore the word “Contribution” has to be understood in its ordinary sense. In other words a contribution is an aid or payment without any consideration [Graphite India ltd vs Dalpat rai Mehta[1978] 48 comp. Cas 683(cal.)]

Overall limit: There’s no specific limit on the deduction amount under 80GGC and 80GGB. However, the total deduction cannot be more than total taxable income.

Compliance with Companies Act only for Corporate Assessee/Donor: Section 182 of the Companies Act, 2013, makes various restrictions on political donations made by companies.

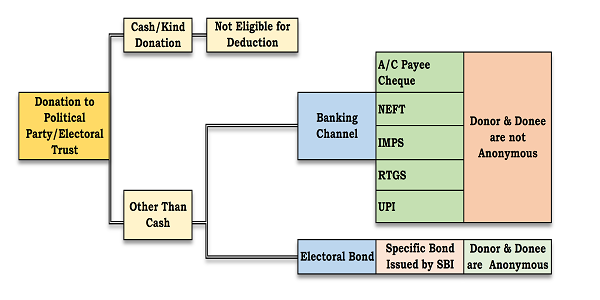

Method of donation: Cash donations are not eligible for this deduction. Donations must be made through other modes like cheque, demand draft, online transfer or electoral trust.

Eligible Donee: Donations only qualify for deduction if made to political parties registered under Section 29A of the Representation of the People Act, 1951, or to electoral trusts.

Donation Receipt: To claim the deduction, Assessee must possess a valid receipt for the donation having details like the name and address of Donor and Donee, PAN, TAN, along with the donation amount , mode of payment and the political party/electoral trust registration number.

METHOD OF DONATION

CONCEPT OF ELECTORAL BONDS

Electoral bonds were introduced in India in 2018 as a way to supposedly clean up political funding. They are essentially bearer instruments, similar to cash, that can be purchased by individuals or entities and donated to eligible political parties. Let’s delve into their structure and the tax implications for both donors and political parties.

How Electoral Bonds Work:

Purchase: Bonds are issued on non refundable basis by designated banks [ SBI Only] for a few days during specific periods and anyone (Indian citizens and companies) can buy.

Who is eligible to receive electoral bonds: Only registered Political parties who have secured not less than 1 % of the votes polled in the last general election to the house of the people or the legislative assembly, as the case may be, shall be eligible to receive bonds.

Validity of Bonds : The bonds shall be valid for fifteen days from the date of issue and no payment shall be made to an payee political party if the bond is deposited after expiry of the validity period, the amount of bonds not encashed within the validity period of fifteen days shall be deposited by the authorized bank to the PM relief fund.

Encashment: Political parties encash the bonds through their verified bank accounts.

Impact of the Supreme Court Judgement in the case Association For Democratic Reforms vs Election Commission Of India

The recent judgment has significantly altered the taxation landscape for electoral bonds. Previously, Political Parties didn’t have to maintain detailed records of donations below Rs. 20,000 received via electoral bonds to claim tax exemption under Section 13A. However, a recent Supreme Court judgement deemed this provision unconstitutional. Now, parties need to maintain complete records for all bond-based donations to claim tax exemption. If Political Parties cannot provide proper records, they might lose tax exemption on those donations, increasing their tax burden.

CRITICISMS OF ELECTORAL BONDS

Despite the intended benefits of transparency, Electoral Bonds have faced criticism due to:

Anonymity: Donor identities remain anonymous, raising concerns about potential influence of undisclosed sources.

Black Money Concerns: The system might not effectively eliminate black money from political funding.

Electoral bonds were introduced with the aim of reforming political funding. While they brought some transparency by using official banking channels, the anonymity clause and the recent judgement on record-keeping raise concerns. The future of electoral bonds and their role in Indian politics remains to be seen.

Example:

FAKE POLITICAL DONATIONS? INCOME TAX DEPARTMENT MAY COME KNOCKING

The Income Tax Department is issuing notices to address situations where taxpayers claim deductions for fake political donations.

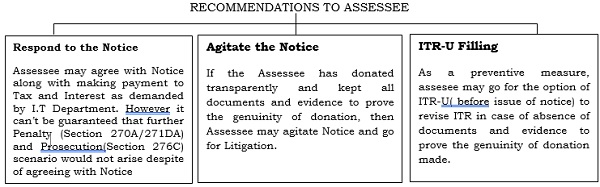

RECOMMENDATIONS TO ASSESSEE

BEWARE OF FAKE POLITICAL DONATIONS: LESSONS FROM THE RUPP [Registered Unrecognized Political Parties] CASE : AHMEDABAD

BEWARE OF FAKE POLITICAL DONATIONS: LESSONS FROM THE RUPP [Registered Unrecognized Political Parties] CASE : AHMEDABAD

This practice of fake political donations came to light when the Income Tax Department conducted searches on Registered Unrecognized Political Parties (RUPPs). The RUPP Ahmedabad case, uncovered in September 2022, involved a major racket concerning bogus donations to Registered Unrecognized Political Parties (RUPPs). This case has significant implications for those considering donating to political parties in India.

Registered Unrecognized Political Parties (RUPPs)

Either newly Registered Parties or those which have not secured enough Percentage of Votes in the Assembly or General Elections to become a National /State Party or those which have never contested Elections since being Registered are considered Unrecognized Political Parties.

Key Points:

Fake Donations: The investigation revealed that a group of 23 RUPPs in Ahmedabad were issuing fake donation receipts to individuals and companies. These receipts were then used by donors to claim tax deductions on their income tax filings.

Income Tax Scrutiny: The Income Tax Department has been issuing notices to individuals and companies who made donations to these RUPPs. This can lead to reassessment of taxes, penalties, and potential legal issues.

Unregistered Political Party: It’s crucial to distinguish between Registered and Unregistered Political Parties. Donations to unregistered parties are not eligible for tax deductions, further as per section 182 of the companies act, contribution to unregistered political party is a punishable offence.

Implications for Donors:

Careful Verification: Before donating, thoroughly verify the legitimacy of the political party. Check the Election Commission of India (ECI) website to ensure the party is registered and has a valid registration number as on the date of donation.

Reputable Parties: Consider donating to a national/state political parties.

Documentation: Maintain proper records of all donations, including receipts and party registration details.

CURRENT SITUATION:

ECI Action: Following the RUPP Ahmedabad case, the ECI has taken stricter measures to identify and remove non-existent RUPPs from its registry.

Tax Department Scrutiny: The Income Tax Department continues to scrutinize donations made to RUPPs.

Additional Considerations:

The RUPP Ahmedabad case highlights the importance of ethical political funding.

Donors should ensure whether party is filing donation reports with ECI and filing ITR’s and fielding candidates in elections.

Overall, Section 80GGB and 80GGC incentivize Corporate and Individual participation in the political process by offering significant tax benefits. However, Assessee must be mindful of the potential transparency concerns. Claiming deductions for fake Political Donations is a way to reduce taxable income, ultimately evading taxes. The Income Tax Notice warns of potential reassessment of income, leading to additional tax liabilities and possible penalties. Political Donations are always susceptive Money Laundering to Income Tax Department. Hence the assessee should stay away from Political Donations just for claiming Tax Deduction to avoid the risk of prosecution under relevant sections of the Income Tax Act, which may lead to imprisonment and fines unless and until the Donation is being made transparently.

…………

Author: CA Himanshu Dubey

Author Bio