INTRODUCTION

Section 44AB was introduced in the Income-tax Act, 1961, by the Finance Act, 1984. This section provides for audit of accounts of assesses having total sales, turnover or gross receipts exceeding the specified limits of Rs. 40 lakhs for business and Rs. 10 lakhs for profession. New Rule 6G, inserted in the Income-tax Rules, prescribes the Forms of Audit report for the above purpose. The requirements for the above audit will apply to accounts relating to previous year relevant to assessment year 1985-86 and subsequent years.

Audit of accounts in the corporate sector has been made compulsory by legislation over a period of years. Realising the importance of audit, this requirement is being extended to non-corporate sector also.

The Income-tax Act already provides for audit of accounts of Public Charitable Trusts and non-corporate assessee establishing new industrial undertakings. Section 142(2A) gave wide powers to the tax authorities to get the accounts in certain specified circumstances audited by a chartered accountant. The new provision introduced by section 44AB has considerably widened the scope of audit.

WHAT IS TAX AUDIT?

The dictionary meaning of the term “audit” is check, review, inspection, etc. There are various types of audits prescribed under different laws like company law requires a company audit, cost accounting law requires a cost audit, etc. The Income-tax Law requires the taxpayer to get the audit of the accounts of his business/profession from the view point of Income-tax Law.

Section 44AB gives the provisions relating to the class of taxpayers who are required to get their accounts audited from a chartered accountant. The audit under section 44AB aims to ascertain the compliance of various provisions of the Income-tax Law and the fulfillment of other requirements of the Income-tax Law. The audit conducted by the chartered accountant of the accounts of the taxpayer in pursuance of the requirement of section 44AB is called tax audit.

The chartered accountant conducting the tax audit is required to give his findings, observation, etc., in the form of audit report. The report of tax audit is to be given by the chartered accountant in Form Nos. 3CA/3CB and 3CD.

WHAT IS THE OBJECTIVE OF TAX AUDIT?

One of the objectives of tax audit is to ascertain/derive/report the requirements of Form Nos. 3CA/3CB and 3CD.

Apart from reporting requirements of Form Nos. 3CA/3CB and 3CD, a proper audit for tax purposes would ensure that the books of account and other records are properly maintained, that they truly reflect the income of the taxpayer and claims for deduction are correctly made by him.

Such audit would also help in checking fraudulent practices.

It can also facilitate the administration of tax laws by a proper presentation of accounts before the tax authorities and considerably save the time of Assessing Officers in carrying out routine verifications, like checking correctness of totals and verifying whether purchases and sales are properly vouched for or not.

APPLICABILITY OF TAX AUDIT

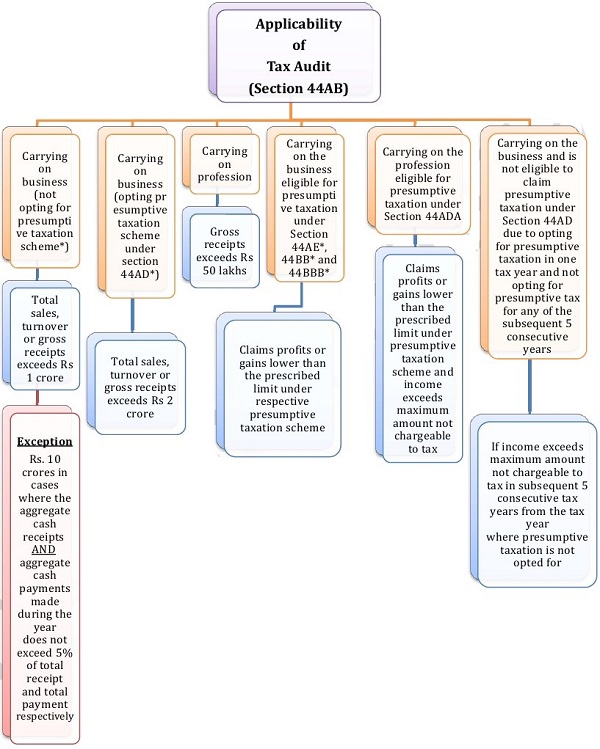

Following categories of taxpayers are required to get tax audit done:

| Category of person | Threshold |

| Carrying on business (not opting for presumptive taxation scheme*) | Total sales, turnover or gross receipts exceeds

Rs 1 crore ( Provided further that for the purpose of this clause, the payment or receipt, as the case may be, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be the payment or receipt, as the case may be, in cash. [Proviso inserted by Finance Act, 2021] |

| Carrying on business (opting presumptive taxation scheme under section 44AD*) | Total sales, turnover or gross receipts exceeds Rs 2 crore |

| Carrying on profession | Gross receipts exceeds Rs 50 lakhs |

| Carrying on the business eligible for presumptive taxation under Section 44AE*, 44BB* and 44BBB* | Claims profits or gains lower than the prescribed limit under respective presumptive taxation scheme |

| Carrying on the profession eligible for presumptive taxation under Section 44ADA* | Claims profits or gains lower than the prescribed limit under presumptive taxation scheme and income exceeds maximum amount not chargeable to tax |

| Carrying on the business and is not eligible to claim presumptive taxation under Section 44AD due to opting for presumptive taxation in one tax year and not opting for presumptive tax for any of the subsequent 5 consecutive years | If income exceeds maximum amount not chargeable to tax in subsequent 5 consecutive tax years from the tax year where presumptive taxation is not opted for |

WHAT IS TAX AUDIT REPORT?

Section 44AB requires the tax auditor to submit the audit report in the prescribed form and setting forth the prescribed particulars.

Sub-rule (1) of Rule 6G provides that the report of audit of accounts of a person required to be furnished under section 44AB shall –

a) in the case of a person who carries on business or profession and who is required by or under any other law to get his accounts audited, be in Form No. 3CA;

b) in the case of a person who carries on business or profession, but not being a person referred to in clause (a), in Form No. 3CB.

Sub-rule (2) of Rule 6G further provides that the particulars which are required to be furnished under section 44AB shall be in Form No. 3CD.

| When is Form 3CA to be used? | When is Form 3CB to be used? |

| Form 3CA is to be used when the financial statements of the entity are audited under any other law. For example:

– a Company audited under Companies Act 2013. – A Limited Liability Partnership (LLP) audited under Limited Liability Partnership Act, 2008 if its turnover exceeds Rs. 40 Lakhs. |

Form 3CB is to be used in all other cases i.e., when financials statements of the entity are not audited under any other law. |

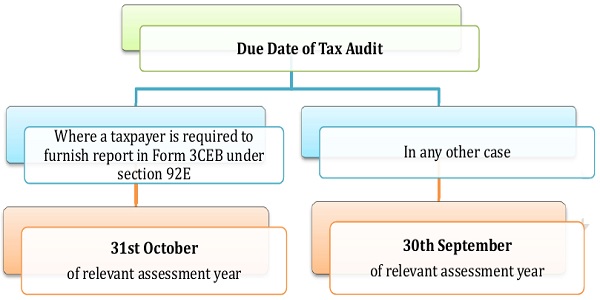

WHAT IS THE DUE DATE BY WHICH A TAXPAYER SHOULD GET HIS ACCOUNTS AUDITED?

A person covered by section 44AB should get his accounts audited and should obtain the audit report on or before the due date of filing of the return of income, i.e., on or before 30th September of the relevant assessment year, e.g., Tax audit report for the financial year 201021 corresponding to the assessment year 2021-22 should be obtained on or before 30th September, 2021.

In case of a taxpayer who is required to furnish a report in Form No. 3CEB under section 92 in respect of any international transaction or specified domestic transaction, the due date of filing the return of income is 31st October of the relevant assessment year. (as amended by Finance Act, 2020)

The tax audit report is to be electronically filed by the chartered accountant to the Income-tax Department. After filing of report by the chartered accountant, the taxpayer has to approve the report from his e-fling account with Income-tax Department.

WHAT IS THE PENALTY FOR NOT GETTING THE ACCOUNTS AUDITED AS REQUIRED BY SECTION 44AB?

According to section 271B, if any person who is required to comply with section 44AB fails to get his accounts audited in respect of any year or years as required under section 44AB or furnish such report as required under section 44AB, the Assessing Officer may impose a penalty. The penalty shall be lower of the following amounts:

a) 0. 5% of the total sales, turnover or gross receipts, as the case may be, in business, or of the gross receipts in profession, in such year or years.

b) Rs. 1,50,000.

However, according to section 271B, no penalty shall be imposed if reasonable cause for such failure is proved.

GENERAL PRINCIPLES TO BE KEPT IN MIND WHILE PREPARING THE STATEMENT OF PARTICULARS FOR FORM 3CD

⇒ Assessee can rely upon the judicial pronouncements while taking any particular view about inclusion or exclusion of any items in the particulars to be furnished under any of the clauses specified in Form No. 3CD.

⇒ If there is a conflict of judicial opinion on any particular issue, assessee may refer to the view which has been followed while giving the particulars under any specified clause.

⇒ The AS, Guidance Notes, SA issued by the Institute from time to time should be followed.

IMPORTANT POINTS TO BE CONSIDERED BY THE TAX AUDITOR WHILE FURNISHING THE PARTICULARS IN FORM NO. 3CD

⇒ The information in Form No. 3CD should be based on the books of account, records, documents, information and explanations made available to the tax auditor for his examination.

⇒ If a particular item of income/expenditure is covered in more than one of the specified clauses in the statement of particulars, a suitable cross reference to such items at the appropriate places.

⇒ If there is any difference in the opinion of the tax auditor and that of the assessee in respect of any information furnished in Form No. 3CD, the tax auditor should state both the view points and also the relevant information in order to enable the tax authority to take a decision in the matter.

⇒ If any particular clause in Form No. 3CD is not applicable, he should state that the same is not applicable.

⇒ In computing the allowance/disallowance, the law applicable in the relevant year should keep in view, even though the form of audit report may not have been amended to bring it inconformity with the amended law.

⇒ In case the auditor relies on a judicial pronouncement, mention the fact as his observations in clause(3) of Form No. 3Ca or clause(5) provided in Form No. 3CB, as the case may be.

The tax auditor may qualify his report on matters in respect of which information is not furnished to him and state in his report that the relevant information has not been furnished by the assessee.

SECTION 44AB – COMPULSORY AUDIT OF ACCOUNTS OF CERTAIN PERSONS CARRYING ON BUSINESS OR PROFESSION Every person,—

a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed one crore rupees in any previous year;

[Provided that in the case of a person whose—

a. aggregate of all amounts received including amount received for sales, turnover or gross receipts during the previous year, in cash, does not exceed five per cent of the said amount; and

b. aggregate of all payments made including amount incurred for expenditure, in cash, during the previous year does not exceed five per cent of the said payment,

this clause shall have effect as if for the words “one crore rupees”, the words “five crore rupees” had been substituted; or]

Provided further that for the purpose of this clause, the payment or receipt, as the case may be, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be the payment or receipt, as the case may be, in cash. [Proviso inserted by Finance Act, 2021]

b) carrying on profession shall, if his gross receipts in profession exceed fifty lakh rupees in any previous year; or

c) carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section 44AE or section 44BB or section 44BBB, as the case may be, AND he has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, in any previous year; or

d) carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits and gains of such person under section 44ADA AND he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his profession AND his income exceeds the maximum amount which is not chargeable to income-tax in any previous year; or

e) carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case AND his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

get his accounts of such previous year audited by an accountant before the specified date and furnish by that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed. (Refer Chapter 5 for better understanding)

Provided that this section shall not apply to the person, who declares profits and gains for the previous year in accordance with the provisions of sub-section (1) of section 44AD AND his total sales, turnover or gross receipts, as the case may be, in business does not exceed two crore rupees in such previous year. (Refer Chapter 5 for better understanding)

Provided further that this section shall not apply to the person, who derives income of the nature referred to in section 44B or section 44BBA, on and from the 1st day of April, 1985 OR, as the case may be, the date on which the relevant section came into force, whichever is later.

Provided also that in a case where such person is required by or under any other law to get his accounts audited, it shall be sufficient compliance with the provisions of this section if such person gets the accounts of such business or profession audited under such law before the specified date and furnishes by that date the report of the audit as required under such other law AND a further report by an accountant in the form prescribed under this section.

Let us understand the first proviso of Section 44AB(1) with the help of an Example:

Mr. Prem, engaged in the business of trading of readymade garments, has turnover of less than Rs. 10 crores during the financial year 2020-21. He made the following transactions during the relevant year:

| Particulars | Mode of transaction Cash (Rs. in lakhs) | Bank (Rs. in lakhs) |

| Receipts | ||

| – Sales | 30 | 580 |

| – Advance from customers | 10 | 20 |

| – Unsecured loan | 10 | 100 |

| Total receipts Payments | 50 | 700 |

| – Purchase | 15 | 400 |

| – Rent | Nil | 50 |

| – Loan repayment | 5 | 50 |

| Total Payments | 20 | 500 |

The turnover of Mr. Prem during the financial year 2020-21 is up to Rs. 10 crores. He shall not be liable for tax audit if his cash receipt and payment during the year does not exceed 5% of total receipt or payment, as the case may be.

Computation of percentage of cash receipts & payments:

| Particulars | Total (A) | Cash (B) | % in cash (B/A*100) |

| Receipts | 750 | 50 | 6.66% |

| Payments | 520 | 20 | 3.85% |

Though the payment made in cash during the year does not exceed 5% of total payments, the percentage of cash receipts exceeds the limit of 5%. Thus, Mr. Prem isn’t entitled to the benefit of the increased threshold limit of Rs. 10 crores for the tax audit.

Explanation: For the purposes of this section:

⇒ “specified date”, in relation to the accounts of the assessee of the previous year relevant to an assessment year, means the due date for furnishing the return of income under sub-section (1) of section 139.

⇒ “accountant” shall have the same meaning as in the Explanation below sub-section (2) of section 288;

MEANING OF ACCOUNTANT [SECTION 288(2)]:

In this section, “accountant” means a chartered accountant as defined in clause (b) of subsection (1) of section 2 of the Chartered Accountants Act, 1949 (38 of 1949) who holds a valid certificate of practice under sub-section (1) of section 6 of that Act, but does not include [except for the purposes of representing the assessee under sub-section (1)]—

a. in case of an assessee, being a company, the person who is not eligible for appointment as an auditor of the said company in accordance with the provisions of sub-section (3) of section 141 of the Companies Act, 2013 (18 of 2013); or

b. in any other case,—

i. the assessee himself or in case of the assessee, being a firm or association of persons or Hindu undivided family, any partner of the firm, or member of the association or the family;

ii. in case of the assessee, being a trust or institution, any person referred to in clauses (a), (b), (c) and (cc) of sub-section (3) of section 13;

iii. in case of any person other than persons referred to in sub-clauses (i) and (ii), the person who is competent to verify the return under section 139 in accordance with the provisions of section 140;

iv. any relative of any of the persons referred to in sub-clauses (i), (ii) and (iii);

v. an officer or employee of the assessee;

vii. an individual who is a partner, or who is in the employment, of an officer or employee of the assessee;

vii. an individual who, or his relative or partner—

I. is holding any security of, or interest in, the assessee:

Provided that the relative may hold security or interest in the assessee of the face value not exceeding one hundred thousand rupees;

II. is indebted to the assessee:

Provided that the relative may be indebted to the assessee for an amount not exceeding one hundred thousand rupees;

III. has given a guarantee or provided any security in connection with the indebtedness of any third person to the assessee:

Provided that the relative may give guarantee or provide any security in connection with the indebtedness of any third person to the assessee for an amount not exceeding one hundred thousand rupees;

viii. a person who, whether directly or indirectly, has business relationship with the assessee of such nature as may be prescribed;

ix. a person who has been convicted by a court of an offence involving fraud and a period of ten years has not elapsed from the date of such conviction.

| APPLICABILITY OF TAX AUDIT | |||||

| Carrying on Business | Carrying on Profession | ||||

| If Total Sales, Turnover or Gross Receipts

> Rs.1 Crore* *Exception: Rs.10 Crore, if Total Receipts ≤ 5% & Total Expenditure ≤ 5% in CASH Provided further that for the purpose of this clause, the payment or receipt, as the case may be, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be the payment or receipt, as the case may be, in cash. [Proviso inserted by Finance Act, 2021] |

If claimed profit u/s 44AE, 44AB, 44BBB

< the profit so deemed u/s 44AE, 44AB, 44BBB |

If claimed profit u/s 44AD

< 8% or 6% AND Total Sales, Turnover or Gross Receipts > Rs. 2 Crore |

If claimed profit u/s 44AD

< 8% or 6% AND declares profit for any of the 5 A.Y. succeeding such P.Y. < 8% or 6% AND Income > the maximum amount which is not chargeable to Income Tax |

If Gross Receipts

> Rs. 50 Lakhs

|

If claimed profit u/s 44ADA

< 50% AND Income > the maximum amount which is not chargeable to Income Tax |

IMPORTANT POINTS TO BE CONSIDERED:

WHAT IF ASSESSEE IS HAVING BUSINESS AS WELL AS PROFESSIONAL INCOME?

- A question may arise in the case of an assessee carrying on business and at the same time engaged in a profession as to what are the limits applicable to him under section 44AB for getting the accounts audited.

- In such a case if his professional receipts are, say, Rs. 51,00,000/- but his total sales, turnover or gross receipts in business are, say, Rs. 48,00,000, it will be necessary for him to get his accounts of the profession and also the accounts of the business audited because the gross receipts from the profession exceed the limit of Rs. 50,00,000/-

- If however, the professional receipts are, say, Rs. 48,00,000/- and total sales turnover or gross receipts from business are, say, Rs. 51,00,000/- it will not be necessary for him to get his accounts audited under the above section, because his gross receipts from the profession as well as total sales, turnover or gross receipts from the business are below the prescribed limits.

WHAT IF ASSESSEE IS HAVING MORE THAN ONE BUSINESS?

- It may, however, be noted that in cases where the assessee carries on more than one business activity, the results of all business activities should be clubbed together.

- In other words, the aggregate sales, turnover and/or gross receipts of all businesses carried on by an assessee would be taken into consideration in determining whether the prescribed limit as laid down in section 44AB has been exceeded or not.

- However, where the business is covered by section 44B or 44BBA turnover of such business shall be excluded.

- Similarly, where the business is covered by section 44AD or 44AE and the assessee opts to be assessed under the respective sections on presumptive basis, the turnover thereof shall be excluded.

- So far as a partnership firm is concerned, each firm is an independent assessee for purposes of Income-tax Act.

- Therefore, the figures of sales of each firm will have to be considered separately for purposes of determining whether or not the accounts of such firm are required to be audited for purposes of section 44AB.

PRESCRIBED LIMIT SHALL BE CHECKED EVERY YEAR

- It must also be understood that the issue whether the turnover exceeds the prescribed limit in the case of business or the gross receipts exceed the prescribed limit in the case of profession is to be determined in each year independent of the results obtained in the

preceding year or years. - Further, this section applies only if the turnover exceeds the prescribed limit according to the accounts maintained by the assessee.

- If the Assessing Officer wants the assessee to get his accounts audited in cases where the figures of turnover as appearing in the books of account of the assessee do not exceed the prescribed limits, he has no option but to pass an order under section 142(2A) directing the assessee to get his accounts audited from a chartered accountant as may be nominated by the Commissioner of Income-tax or the Chief Commissioner of Income-tax.

TAX ADUIT IS NOT AN INVESTIGATION.

- In Sahara India (Firm) v CIT (2008) 169 Taxman 328, the supreme Court held pointed out that the tax audit u/s 44AB of the Income Tax Act, 1961, is not an investigation unlike audit u/s 142(2A) of the Act.

MR. Y, A CHATERED ACCOUNTANT IN PRACTICE HOLDS APPOINTMENTS AS A STATUTORY AUDITOR OF 21 COMPANIES.

- Since Mr. Y holds appointment as a statutory auditor of more than 20 companies, he cannot sign and upload any report/ certificate pertainting to a company. Hence Mr. Y is not competent to sign and upload tax audit report until he vacates the office of the statutory auditor of on of the companies.

- However, there is no such limitation for report/certificate pertaining to a person other than a company. Hence, Mr. Y can sign tax audit report of a person othan than a company.

COMPANY CANNOT CARRY PROFESSION

- In ITO v Ashalok Nursing Home Pvt Ltd (2006) 156 Taxman 86 (Mag), the Tribunal held that a company cannot be said to carry on a profession. For a person to be engaged in a profession personal skill is necessary. A company, being an artifical person, cannot be said to possess any personal skills. A company does not have a mind and body and therefore cannot be engaged in profession. It can neither have any intellectual skill nor any manual skill.

APPLICABILITY OF SECTION 44AB TO NONRESIDENT

- Where the non-resident assessee did not carry any business in India nor maintained any permanent establishment in India, the provisions of section 44AB are not applicable to him [ITO v Voest Alpine Industrieanlagenbau GMBH, Austria (1968) 67 ITD 219 (Cal)]. The non-resident is taxable only in respect of income accruing or arising or received in India. Accordingly, the audit would be confined only to the non-resident’s Indian operations.

WHETHER TAX AUDIT APPLICABLE WHERE INCOME IS EXEMPT U/S 10?

- As per the ruling of Hon’ble ITAT in the case of ACIT v. India Magnum Fund [2002] 81 ITD 295 (Mum), if entire income of the assessee is exempt u/s 10, he will not be liable to tax audit u/s 44AB despite his turnover or gross receipts exceed the prescribed or threshold limit, since the heading of chapter III dealt with ‘Incomes which do not form part of total income’ and as such provisions of Section 44AB cannot and do not have any application in relation to incomes which are enumerated under chapter III and are expressly excluded from total income”

APPLICABILITY OF TAX AUDIT ON AGRICULTURIST

- Agriculturist with no income under the head “Profits and Gains from Business or Profession” is not required to get his accounts audited, even though his sale of agricultural products exceeds prescribed or threshold limit.

CLARIFICATION BY CBDT ON APPLICABILITY OF PROVISIONS OF SECTION 44AB TO POLITICAL PARTIES

- The CBDT vide notifiation no. 1988 dated 19th October, 2000 clarified that the provisions of Section 44AB shall not apply to political parties.

- the Board are of the view that the income of the political parties are governed by the special provisions i.e. section 13A of the Income-tax Act, 1961, and accordingly the provisions of Chapter IVD which are applicable for profits and gains of business or profession cannot be applied in the cases of political parties. Income of political parties from voluntary contributions cannot be said to be income from profession so as to attract section 44AB or 271B of the Income-tax Act.

- However, the political parties will have to fulfill the requirement of maintaining the accounts and getting them audited by an accountant, as provided in section 13A of the Act to claim the benefit of exemption”.

APPLICABILITY OF TAX AUDIT ON COMMISSION AGENTS, ARAHTIAS ETC.

- In the case of agents whose position is similar to that of kachha arahtia, the turnover is only the commission and does not include the sales on behalf of the principals. In the case of agents of the type of pacca arahtia, on the other hand, the total sales/turnover of the business should be taken into consideration for determining the applicability of the provisions of section 44AB. (Circular: No. 452 [F. No. 201/3/85-IT(A-II)], dated 17-3-1986.)

*****

Disclaimer: This update is not an advertisement or any form of solicitation. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we Endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in future. Readers should obtain appropriate professional advice.

Author Bio

I have below query for AY 2021-22

I have 5 lakh salary income as my main source of income.

Short Term and Long Term Capital Loss around 1 lakh from Mutual Funds and Listed Stocks

Brought Forward Long Term Capital Loss from Previous Year

Rs 500 Intraday Turnover which is also Rs 500 Intraday Loss

Is ITR 3 or ITR 4 Applicable in this case

Intraday Loss of Rs 500 should be shown under Business Income or Presumptive Income and under which section it falls and which ITR it is to be filed.

Is Tax Audit applicable for this small amount of Intraday turnover.

Another query, I downloaded Zerodha Tax P&L and also the new AIS Annual Income Statment from incometax website. There is a small difference in sale value and purchase price for all the Equity trades. Not sure which one is correct.

Also, which expenses are allowed to be deducted from the equity sale/ purchase transactions while filing Tax Return.

Thank you for your help.

I am unable to upload tax audit report for AY 2021-22 can you Guide.

Is it possible to file Return of assessee and then file Tax audit report

As per the ICAI guidance note on tax audit, even if the income of assessee is exempt under income tax act he still needs to get the tax audit done