Modification of residency provisions

In order to bring prevent tax abuse the Finance Act, 2020 modified the Residency Provision.

According to the un-amended Section 6, an individual is said to be resident in India in any previous year, if he—

(a) is in India in that year for a period or periods amounting in all to 182 days or more ; or

(b) having within the 4 years preceding that year been in India for a period or periods amounting in all to 365 days or more, is in India for a period or periods amounting in all to 60 or more in that year.

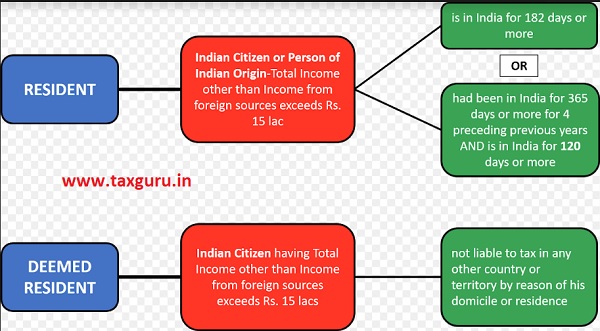

According to Explanation 1 an Indian citizen or a person of Indian origin shall be Indian resident if he is in India for 182 days instead of 60 days in that year. This provision provides relaxation to an Indian citizen or a person of Indian origin allowing them to visit India for longer duration without becoming resident of India.

Many Indian citizen or person of Indian origin visiting India were misusing this provision, where period of 182 days was specified for them. Individuals, who are actually carrying out substantial economic activities from India, manage their period of stay in India, so as to remain a non-resident in perpetuity and not be required to declare their global income in India.

Resident

The Finance Act 2020 applicable for AY 21-22 has altered the Provision for Indian Citizens and Persons of Indian Origin.

Accordingly the period of 182 days specified in the Explanation for Indian citizen and person of Indian origin with total income other than income from foreign sources more than Rs. 15 lacs, has been reduced to 120 days.

The Finance Act 2020 also introduced the concept of Deemed Resident.

Thus according to the new Provision introduced, those Indian citizen having total Income other than Income from foreign sources exceeds Rs. 15 lacs, who don’t have a domicile or residence in any other country, will be Deemed to be Resident of India.

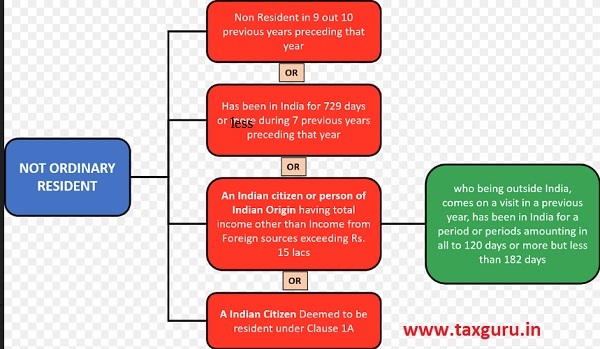

Not Ordinary Resident

According to Income Tax Act, a Resident but not ordinary resident’s Foreign Income is taxable in India if it is controlled from India. Also an ordinary Resident’s Foreign Income is taxable in India along with his foreign Income controlled from India.

“Not ordinarily resident” in a previous year means if the person is an individual who has been non-resident in 9 out of the 10 previous years preceding that year, or has during the 7 previous years preceding that year been in India for an overall period of 729 days or less. Clause (b) thereof contains similar provision for the HUF.

The Finance Act 2020 added two more conditions to become Not Ordinary Resident which are:

> a citizen of India, or a person of Indian origin, having total income, other than the income from foreign sources, exceeding fifteen lakh rupees during the previous year, as referred to in who, being outside India, comes on a visit to India in any previous year, for a period or periods amounting in all to 120 days or more but less than 182 days

> a citizen of India who is deemed to be resident in India under clause (1A).

*income from foreign sources means income which accrues or arises outside India (except income derived from a business controlled in or a profession set up in India)

Plausible Effects

> The issue of stateless persons has been bothering India since quite some time. Though the provisions introduced aim to reduce tax abuse, especially those by High Net worth Individuals, they may have opposite effects.

> The people aimed to catch, may instead give up their citizenship altogether, to avoid coming under this provision of law. Moreover, those people of Indian origin who are now Deemed citizens due to the number of days spent in India, might reduce their total stay in a year starting FY 20-21, to less than 120 days. This will not only reduce foreign remittances in India, if the covered people decide to shift their families to outside India, but also reduce their expenses in India.

> Though it’s a great step to tax those people who avoid getting taxed by living in Non taxable countries, but this step might not be beneficial all in all because a reduction in foreign Income of India might be more than the gain from taxing them.

> This step might also make Indian citizens and persons of Indian origin emotionally distant from their home country, while those who were actually aimed to be covered under the new amendment,might just give up their nationality all together.

The concept of Resident and Not Ordinary Resident under Section 6 for Indian citizens and Persons of Indian origin, is explained with the following illustration

Disclaimer: The Article is based on the Relevant Provisions and as per the information existing at the time of the preparation. In no event the author will be liable for any direct and indirect result from this Article. This is only a knowledge sharing initiative.

The Author can be reached at aayushi.ajmani@gmail.com or +918826071696

Kindly note that there is a mistake in not ordinarily resident diagram.

It is mentioned 729 days or more instead of 729days or less

This article is incomplete in as much as the status Non-resident status is missing.

In a final essence it should also state about Non-resident-in real terms and their no of days stay outside india.

no comments