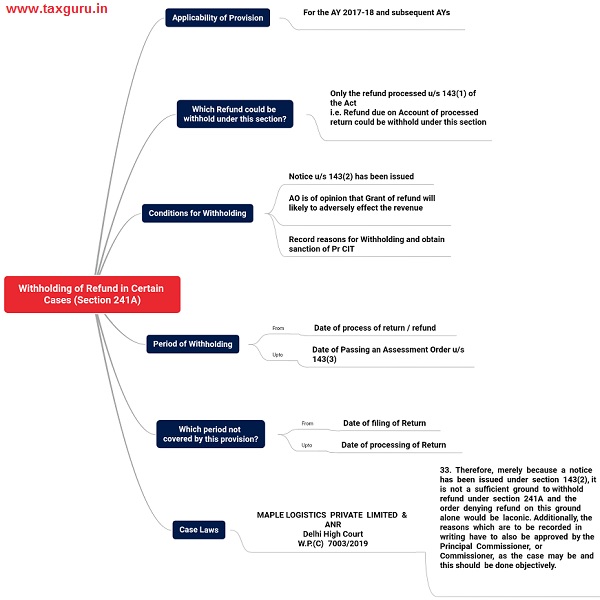

Overview:

Finance Act, 2017 inserted the section 241A to enable the AO to withhold the refund arise after processing of the Income Tax Return. The provision has been analyzed as under.

Provision of Income Tax Act

Withholding of refund in certain cases.

241A. For every assessment year commencing on or after the 1st day of April, 2017, where refund of any amount becomes due to the assessee under the provisions of sub-section (1) of section 143 and the Assessing Officer is of the opinion, having regard to the fact that a notice has been issued under sub-section (2) of section 143 in respect of such return, that the grant of the refund is likely to adversely affect the revenue, he may, for reasons to be recorded in writing and with the previous approval of the Principal Commissioner or Commissioner, as the case may be, withhold the refund up to the date on which the assessment is made.

Position before Insertion of Section 241A

Earlier, the provision of section 143(1D) specify that the processing of a return shall not be necessary, where a notice has been issued to the assessee under section 143(2) of the Act.

Then section 143(1D) was amended by the Finance Act, 2016 and it was provided that with effect from assessment year 2017-18, processing under section 143(1) of the Income-tax Act is to be done before passing of assessment order.

Therefore, earlier, the refund was no paid to the assessee until passing of assessment order. This becomes trigger point for unnecessary litigations before the various High Courts. This further leads to increase in the cost of interest u/s 244A for the Department.

Therefore, in order to address the grievance of delay in issuance of refund in genuine cases, a proviso has been inserted in section 143(1D) of the Income-tax Act specifying that the provisions of the said sub-section shall cease to apply in respect of returns furnished for assessment year 2017-18 and onwards.

Applicability of Provision

This section applies for the assessment year 2017-18 and thereafter.

Which Refund Covered

The language of the section is clear and provides that the only the refund due to the assessee u/s 143(1) i.e. refund as per intimation u/s 143(1) could be withheld under this section (subject to fulfilment of other conditions discussed hereinafter).

Therefore, withholding of the refund due to the assessee on account of other reasons such as refund due after rectification u/s 154, refund on account of appeal effect etc. would not be governed by the provisions of this section. Under such circumstances, the Assessing Officer is bound to issue a refund as per time prescribed under Citizen Charter or the AO can make adjustment u/s 245 of the Act.

Conditions for Withholding

The processed refund could be withhold subject to fulfilment of following conditions and procedure;

– Notice u/s 143(2) for the said return has been issued

– Assessing Officer is of the opinion that the grant of the refund is likely to adversely affect the revenue

– Reasons to be recorded in writing and with the previous approval of the Pr. CIT

Now, question arise, whether, the assessee is empowered to know the reason for withholding of processed refund? The answer is yes. However, section does not provide regarding communication of said reasons with assessee but according to principal of natural justice, the assessee empowered to know the reason for such withholding.

Period of Withholding

The refund could be withhold for the period beginning from the date of processing of refund u/s 143(1) till the date of passing an assessment order u/s 143(3) or 144 as case may be.

Which Period not Covered

The refund is claimed by filing of Return of Income. In the Act, there is no time limit provided for processing of the Return. Therefore, the period from date of filing of return till the date of processing of the return is not covered by the provision of this section.

Important Case Laws

Huawei Telecommunications (India) Company Private Limited V. Union Of India (CWP No. 2698 of 2020)

The Hon’ble Punjab and Haryana High Court held that It is evident that procedure for refund and withholding of refund is often being used as delaying tactics for various reasons including window dressing of collection of revenue. The method adopted is a short sighted vision. Apart from harassment to the assessee, it results in paying interest on the delayed amount of refund putting further burden on the exchequer. It cannot be lost sight of that trade and commerce is a life blood of the system, if the excess amount deposited as tax is not refunded to the entrepreneur/assessee, it has effect on the liquidity and business. There cannot be second opinion that the revenue collection and securing the interest of the revenue is of great importance, at the same time the revenue is to be collected like an apiarist extracts honey from beehive without destroying it. Considering the facts that in spite of there being no justifiable reason as per provisions of the statute, yet the refund was withheld for which the petitioner would be entitled to statutory interest.

The Hon’ble Delhi High Court held that

32. The power of the AO has been outlined and defined in terms of the Section 241A and he must proceed giving due regard to the fact that the refund has been determined. The fact that notice under section 143(2) has been issued, would obviously be a relevant factor, but that cannot be used to ritualistically deny refunds. The AO is required to apply its mind and evaluate all the relevant factors before deciding the request for refund of tax. Such an exercise cannot be treated to be an empty formality and requires the AO to take into consideration all the relevant factors. The relevant factors, to state a few would be the prima facie view on the grounds for the issuance of notice under section 143(2); the amount of tax liability that the scrutiny assessment may eventually result in vis-a-vis the amount of tax refund due to the assessee; the creditworthiness or financial standing of the assessee, and all factors which address the doubt of recovery of revenue in doubtful cases.

33. Therefore, merely because a notice has been issued under section 143(2), it is not a sufficient ground to withhold refund under section 241A and the order denying refund on this ground alone would be laconic. Additionally, the reasons which are to be recorded in writing have to also be approved by the Principal Commissioner, or Commissioner, as the case may be and this should be done objectively.

Summary

The above provisions are summarized in following chart:

Author Bio

F.Y.2021-22 return submitted but not yet received refund and compliance certificate. one grievance lodged but not yet received reply or any guidance received from I.T. Department. please advised me.

Very good analysis