Case Law Details

Marche Retail Pvt. Ltd. Vs ACIT (ITAT Delhi)

In the case of Marche Retail Pvt. Ltd., the ITAT Delhi deleted the addition of ₹35,22,000 made u/s 68 r.w.s. 115BBE relating to demonetisation-period cash deposits. The AO treated certain December-2016 deposits as unexplained mainly because they were not deposited immediately after the announcement of demonetisation, while CIT(A) dismissed the appeal ex-parte.

The Tribunal observed that the assessee was engaged in FMCG retail with multiple outlets and had already furnished detailed cash deposit statements, VAT returns, bank records & audited books before the AO. Cash balance as on demonetisation date was ₹1.48 crore, and subsequent cash sales during November & December 2016 were sufficient to explain the deposits. The AO made the addition merely on timing of deposits without rejecting books or bringing contrary evidence.

ITAT held that once books are audited and cash sales are recorded & reconciled, deposits cannot be treated as unexplained merely due to staggered deposits across outlets. Since adequate source of cash existed and no adverse material was found, the addition was deleted and the assessee’s appeal allowed on merits.

FULL TEXT OF THE ORDER OF ITAT DELHI

1. This appeal is filed by the Assessee against the order of Ld. Commissioner of Income Tax (Appeals)/National Faceless Appeal Centre (NFAC), Delhi (hereinafter referred to ‘ld. CIT(A)’) dated 16.07.2025 for AY 2017-18.

2. Brief facts of the case are, assessee filed its return of income for the AY 2017-18 on 27.10.2017 declaring total income of Rs.59,94,400/-. The case was selected for complete scrutiny under CASS, accordingly, notices u/s 143(2) and 142(1) along with questionnaire were issued and served on the assessee through e-portal. In response AR of the assessee attended and submitted the relevant information through e-portal.

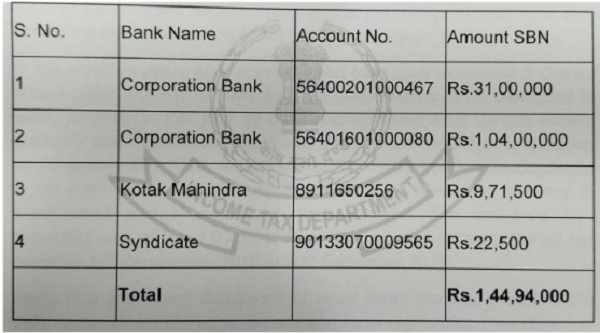

3. Assessee is engaged in the business of wholesale in a variety of goods. During the assessment proceedings, the Assessing Officer observed that the assessee had deposited cash of Rs.1,44,94,000/- in old currency in its bank account during demonetization period as under:-

4. The assessee was asked to explain the source of the same, and further asked to submit the relevant information on the basis of month wise cash sales and cash in hand for the FY 2015-16 and 2016-17. The assessee filed the relevant information. Further assessee submitted the following submissions, for the sake of brevity it is reproduced below:-

“The assessee had 6 outlets spread within the distance of 50kms and all being individually run by the team of professionals without any interference of the owners/ Directors of the company. All the cash sales and proceeds are independently responsibility of the respective Shop Managers. In such a case every outlet is maintaining cash in hand for daily requirements including coins, cash small notes and cash required for petty expenses and also a cushion of cash required for any eventually as not less than one Hundred staff is working at each outlet. Every shop deposits the cash collected or withdraws from bank for needs irrespective of any excess cash lying at any other outlet. No movement of cash takes place from one shop to another unless the management by themselves carry the amount handing over the receipt of such cash and depositing the same at Head Office of the company.

In the previous years also assessee had total cash exceeding 2 Crores at one given moment of time but eventually every cash is deposited in Bank, similarly in this year all cash was collected from various outlets gradually and deposited in Bank after the declaration of Demonetization on November 8th, 2016. An amount of Rs. 1,40,28,500-/ was deposited in old currency of Rs. 500 and Rs. 1000 notes remaining currency of small notes and change bags were retained. The assessee also deposited sum of Rs. 1,03,38,334/- in cash of new currency during the period of 10th November, 2016 to 30th December, 2016.

Being in a line where thousands of small items are sold including the daily consumables like eggs, breads and fresh vegetables, maintaining of cash balances become mandatory. Assessee has been very regularly depositing the cash in banks however sometimes accumulation takes place because of seasonability and paucity of vehicle to carry such large cash. Festival season and high October Sales resulted in high cash on the date of Demonetization. Still considering the volume and sales of the Assessee cash deposited in just 6 days of sales of the assessee. Total sales including taxes were beyond Rs. 84 Crores and only Rs. 1.40 Crores was cash in hand.”

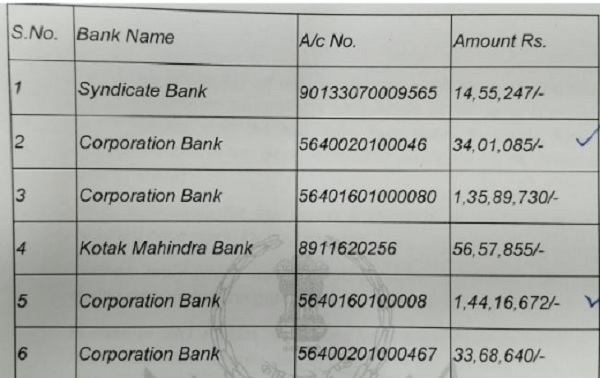

5. After considering the above submissions Assessing Officer rejected the same and further issued a show cause notice to explain why cash deposit of Rs.3,85,20,589/- be not treated as unexplained and added to the total income of the assessee. In the notice issued to the assessee, assessee was asked to file the bank statement of all bank accounts for the period 01.11.2016 to 31.12.2016, bank account details and date wise cash deposits during the demonetization period relating to old and new currencies, further evidences in support of claim and deposit in new currency. In response assessee submitted that assessee has actually deposited Rs.2,43,67,834/- only and accordingly assessee has filed the details of cash deposit in various banks maintained by the assessee. However, Assessing Officer forwarded the following chart to the assessee and asked the assessee to substantiate the sources for such deposits:-

6. By referring to the above chart, assessee submitted that the serial No.2 and serial No.5 of the account mentioned by the Assessing Officer are not belongs to the assessee, and assessee has submitted that in three bank account mentioned by the Assessing Officer in which assessee has deposited in SBN of Rs.1,40,29,500/- along with certificate of deposit of old currencies were also submitted before the Assessing Officer. Assessee submitted bank statements from 01.11.2016 to 31.12.2016 along with the cash deposit report. Further assessee has submitted copy of VAT return, and submitted that only for third quarter relating the return filed Delhi VAT were revised for some small changes.

7. After considering the above submissions, the Assessing Officer rejected the same and observed that nature of assessee’s business and fact of different outlets maintained by the assessee are considered but trend of cash deposit show that cash was deposited in 2016. When demonetization was declared all the cash in hand should have been deposited. He observed that there is no logic of depositing cash in various instances. Due to different stores at different locations time span of deposits may be spread over the number of days. But cash deposited after long period is not justified and shows that amount to this extent was not available with the assessee on 08.11.2016. On the basis of certificates issued by the banks and submitted by the assessee at the last stage of assessment proceedings, for the cash deposit SBNs at Rs.1,44,94,000/-, the Assessing Officer treated the cash deposit made by the assessee during the December period are not genuine and accordingly he proceeded to make the following additions to the total income of the assessee u/s 68 of the Act, and the relevant proposed additions are as under:-

8. Aggrieved with the above order assessee preferred an appeal before NFAC, Delhi and filed the grounds of appeal. However, Ld. CIT(A) has given several notices for hearings and the relevant details are reproduced at page 3 of the appellate order. Since no response from the assessee Ld. CIT(A) found that the additions proposed by the Assessing Officer is justified and accordingly he dismissed the appeal preferred by the assessee.

9. Aggrieved with the above order assessee is in appeal before us raising following grounds of appeal;-

1. Ld. CIT (Appeals) erred in law and on facts in confirming the addition of Rs. 35,22,000/- made u/s 68 on ex-parte basis in a summary manner by deeming non-participation in the appellate proceedings by the appellant as disinterest on its part to pursue the appeal, but ignoring that all facts and explanations of the appellant along with the supporting evidences were already available on AO’s record, which were not even called for examination. Thus, the appellate order made mechanically by simply confirming the assessment order without applying his mind and thereby violating the mandatory requirement of Section 250(6) of the Act which requires a reasoned and speaking order, must be quashed.

2. Ld. CIT (Appeals) erred in law and on facts in confirming the addition of Rs. 35,22,000/- made by the AO u/s 68 r.w.s. 115BBE by treating cash deposits made in bank accounts during the demonetization period in December-2016 only as unexplained by ignoring the fact that the addition had been made arbitrarily, whimsically and simply on conjectures and surmises by the AO: and without bringing any evidence on record to the contrary. Thus, the addition so made must be deleted.

3. Ld. CIT (Appeals) erred in law and on facts in confirming the addition of Rs. 35,22,000/- made by the AO u/s 68 r.w.s. 115BBE on ex-parte basis for cash deposits made during the demonetization period as unexplained without rejecting the books of account by ignoring that books of account were audited; and also ignoring the fact that the appellant is engaged in FMCG retail business; sufficient cash balance was available in the books for deposits; which arose from cash sales and which were duly recorded in the books and stood reconciled with the VAT Returns. Thus, the addition so made must be deleted.

4. The appellant craves leave to add, substitute, modify, delete or amend all or any ground of appeal either before or at the time of hearing.

10. At the time of hearing Ld. AR of the assessee submitted that no doubt, the ld. CIT(A) has dismissed the appeal without giving proper opportunity to explain the case of the assessee and further submitted that all the relevant information relating to the facts are already filed before the Assessing Officer. Ld. CIT(A) has ignored the above facts on record. On merit Ld. AR of the assessee submitted that the Assessing Officer has made the addition of Rs.35,22,000/- u/s 68 r.w.s. 115BBE with regard to cash deposits made during demonetization period as unexplained without rejecting the books of accounts and Assessing Officer ignored the fact that the books of account are already audited. Further he submitted that assessee is engaged in FMCG Retail Business and it had sufficient cash balance in its books of account and the source of the same are cash sales which were recorded in the books of account and reconciled with the VAT return. He prayed that all the relevant informations are already available on record and prayed that the issue may be decided on merits.

11. On the other hand, Ld. DR insisted that the first appellate order is ex parte due to non-prosecution from the assessee side. He relied on the findings of the lower authorities.

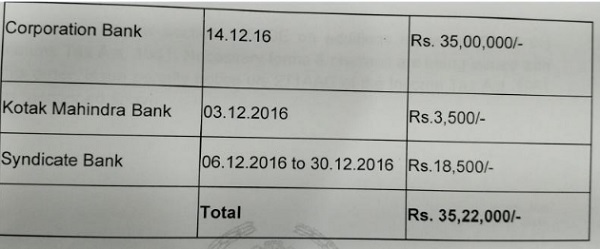

12. Considered the rival submissions and material placed on record, we observed that assessee has made detailed submissions before the Assessing Officer during assessment proceedings however, in first appellate proceedings assessee failed to attend the hearings on several occasions. We can remit this issue back to the file of CIT(A) however, we observed that all the relevant informations are already available on record. This being factual issue, we proceeded to adjudicate. We observed that assessee is engaged in the business of FMCG and have stores on various places. Assessee has also filed detailed cash deposits made by the assessee during demonetization period before the Assessing Officer and Assessing Officer noticed that assessee has submitted the details of cash deposits in SBN to the extent of Rs.1,44,94,000/- and he observed that assessee has not deposited the SBN once the demonetization is announced and should have deposited one go, at the same time, he observed that there is no logic of depositing cash in various instances. He acknowledged the fact that assessee is having different stores at different locations time span of deposits may be spread over the number of days, the cash deposited after long period is not justified and accordingly, he proceeded to make the addition of Rs.35,00,000/- deposited on 14.12.2016 and Rs.3,500 on 03.12.2016 in Kotak Mahindra Bank and Rs.18,500 on 06.12.2016 to 30.12.2016 in Syndicate Bank. We observed that the assessee has made the total cash deposits of SBN currencies of Rs.1,44,94,000/- which was also confirmed by the Assessing Officer. From the details of cash deposit submitted by the assessee before the Assessing Officer are as under:-

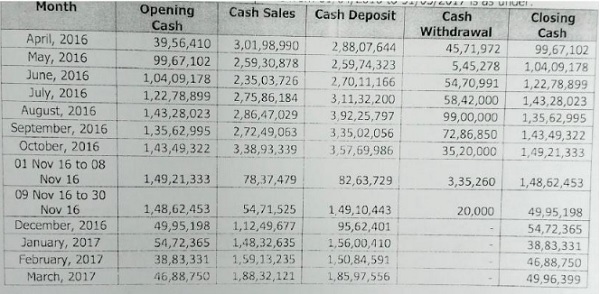

13. From the above chart it is clear that on the date of announcing the demonetization assessee had closing cash balance of Rs.1,48,62,453/- and assessee had recorded sales of Rs.54,71,525/- in November 2016 post demonetization period and deposited cash of Rs.1,49,10,443/-. During December 2016 assessee had declared cash sales of Rs.1,12,49,677/- and made cash deposit of Rs.95,62,401/-. The above details clearly shows that assessee has enough cash sales to make the deposits during the post demonetization period particularly, November and December. We observed that the Assessing Officer as merely proceeded to make the addition on the basis that assessee had deposited cash on 14.12.2016 in Corporation Bank of Rs.35,00,000/- and another Rs.22,000/- in Kotak Mahindra Bank and Syndicate Bank on various dates. He has not brought on record whether the above said cash are SBN or new notes. He has proceeded to make some addition without their being any proper justification for making the above addition. We noticed that assessee has enough source of cash to make the above deposits in its banks. Bank account maintained in Corporation Bank and Kotak Mahindra Bank. Therefore, we are inclined to allow the Ground No.3 raised by the assessee on merit.

14. At this stage we are not inclined to adjudicate on other grounds raised by the assessee.

15. In the result, appeal filed by the assessee is allowed.

Order pronounced in the open court on this day of 12th February 2026

Author Bio