Finance Act, 2020 had introduced provisions relating to TCS on sale of goods u/s 206(1H). Finance Act, 2021 introduced provisions relating to TDS on purchase of goods u/s 194Q to cover those transactions which were left uncovered by section 206C(1H).

These amendments have increased the compliance burden for the taxpayer as it impacts the most basic transactions of purchase and sale of goods.

An interplay of the above sections has added to the practical difficulties faced by the taxpayers entering into above transactions, especially with possibilities of overlap between the TDS and TCS provisions.

Therefore, it becomes important to understand the basic provisions and application of both these sections.

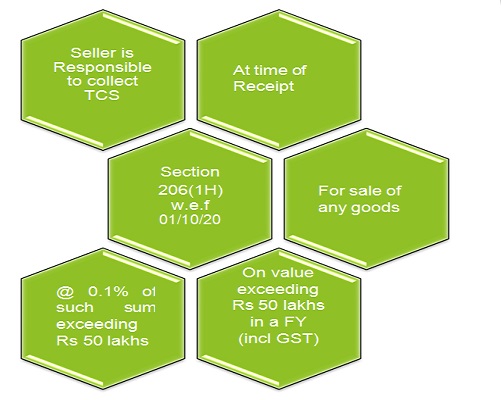

Section 206(1H) – TCS on sale of goods

Notes:

- Seller means a person whose total sales/gross receipts/ turnover from business carried on by him exceed Rs 10 Crores in immediately preceding previous year (excluding GST). Hence not applicable in first year of

- No TCS applicable in the following cases:

- Buyer is Central/State Government, local authority, Embassy, High Commission, legation, Consulate of foreign state

- If TDS is deducted under any other provision on the said transaction.

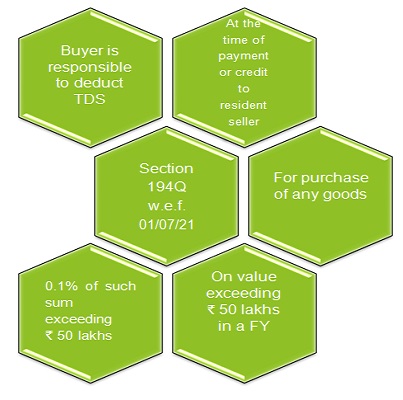

Section 194Q – TDS on purchase of goods

Notes:

- Buyer means a person whose total sales/gross receipts/turnover from business carried on by him exceed Rs 10 crores in immediately preceding FY (excluding GST). Hence not applicable in first year of

- The period from April to June, 2021 to be considered for computing threshold limit of Rs 50 lakhs for each seller (including GST). No TDS to be paid on

- If amount is credited in books of accounts by whatever name called the provisions of section 194Q will apply

Important Points:

- No liability under section 194Q in following scenarios:

- TDS is deducted under any other provisions or TCS is collectible except u/s 206C(1H). There is still reporting requirement under Form 26Q

- In relation to transactions involving purchase of immovable property

- If seller is Central/State Government, Reserve Bank of India, corporations established by Central Act which are exempt from Income Tax and Mutual Funds covered under section 10(23D)

- Any other person as Government may notify

- If there is purchase/sales return then TDS/TCS must have been deducted/collected as per provisions, hence such TDS/TCS will have to claimed at the time of filing income tax

- TDS Credit shall be allowed in the financial year in which income corresponding to such TDS is

- The fixed assets and capital assets will also be covered u/s 194Q as the provisions of this section apply to all types of goods.

- In case of potential overlap on a transaction, section 194Q will prevail. However, if buyer defaults then obligation shifts on seller

Summary of section 194Q and 206C(1H)

| Particulars | 194Q | 206C(1H) |

| Who is responsible? | Buyer | Seller |

| Applicable from? | 01/07/2021 | 01/10/2020 |

| When to be deducted or collected? | Payment or credit,

whichever is earlier |

At the time of

receipt |

| Rate of TDS/TCS | 0.1% | 0.1% |

| Penal Rate of TDS/TCS if PAN not available | 5%

(if provides PAN/Aadhar but has not filed income tax return for last two financial years of which the due date to file return has expired and amount of TDS or TCS is Rs 50,000/- or more in each of those two years) |

1% |

| When is TDS/TCS to be deducted? | Purchase of goods of aggregate value exceeding Rs 50 lakhs in a year (incl GST) | Sale consideration received exceeds Rs 50 lakhs in a year (incl GST) |

| Quarterly statement to be filed | 26Q | 27EQ |

| Certificate to be issued | Form 16A | Form 27D |

Consequences of default

1. For failure to deduct TDS

-

- Interest @ 1% p.m or part of the month

- Deemed to be an assessee in default

- 30% of purchase value will be disallowed u/s 40(a)(ia)

- For failure to pay TDS after deduction

- Interest @ 1.5% p.m or part of the month

- Deemed to be an assessee in default

- 30% of purchase value will be disallowed u/s 40(a)(ia)

- For Late filing/Non filing of TDS/TCS Return

- Rs 200/- per day from due date

- Minimum – Rs 10,000/-, Maximum –Rs 1,00,000/-

is 194Q and 206C(1H) both provision applicable on different transaction