Background

As per Section 5 of the Income Tax Act, Income which is accrued or deemed to accrue and received or deemed to receive in India is only taxable in the hand of non -resident. Therefore, any income of non -resident which is accruing outside India is not taxable until that is deemed to accrue in India. Section 9 of Income tax act creates such deeming fiction.

A per section 9, all income accruing or arising, whether directly or indirectly, through or from any business connection in India, or through or from any property in India, or through or from any asset or source of income in India, or through the transfer of a capital asset situate in India shall be deemed to accrue or arise in India.

Now the question arises whether transfer of any asset outside India can lead to transfer of capital asset in India. In General transfer of any asset by non -resident situated outside India was not taxable under the India Tax Laws. As per landmark ruling of the Hon’ble Supreme Court in Vodafone International Holdings BV v. Union of India (the “Vodafone case”) (2012) in which the Court held that

- Transfer of shares of a Cayman Islands company would not be subject to capital gains tax in India since the shares of the Cayman Islands company were not located in India.

- Controlling interest is embedded in the shares and not is a separate asset.

- Legal form cannot be disregarded unless the transaction is sham or tax avoidant.

In this case the ownership of Indian company has been transferred by transferring the shares of its holding company outside India.

Indian Tax authority believed that such types of transferred outside India is already covered under the deeming fiction created by section 9. Following is the text from memorandum of Finance Bill 2012-

“Section 9 of the Income Tax provides cases of income, which are deemed to accrue or arise in India. This is a legal fiction created to tax income, which may or may not arise in India and would not have been taxable but for the deeming provision created by this section. Sub-section (1)(i) provides a set of circumstances in which income accruing or arising, directly or indirectly, is taxable in India. One of the limbs of clause (i) is income accruing or arising directly or indirectly through the transfer of a capital asset situate in India”. The legislative intent of this clause is to widen the application as it covers incomes, which are accruing or arising directly or indirectly. The section codifies source rule of taxation wherein the state where the actual economic nexus of income is situated has a right to tax the income irrespective of the place of residence of the entity deriving the income.”

Therefore, Finance Act 2012 inserted explanation 4 and 5 in section 9 of the income tax, and amended section 2(14) to include in the definition of “property” the right in or in relation to India company, including right of management, section 2(47) to include in the definition of “transfer” disposing of or parting with an asset/ interest or creating any interest in any manner, section 195 to cast responsibility to deduct tax on non -resident by quoting in memorandum “Certain judicial pronouncements have created doubts about the scope and purpose of sections 9 and 195. Further, there are certain issues in respect of income deemed to accrue or arise where there are conflicting decisions of various judicial authorities. Therefore, there is a need to provide clarificatory retrospective amendment to restate the legislative intent in respect of scope and applicability of section 9 and 195 and also to make other clarificatory amendments for providing certainty in law.”

Further explanation 6 and 7 included in finance Act 2016 to decide what constitute substantial value and on what explanation 5 does not apply, respectively.

All these amendments have been made by inserting explanation in the respective sections and made applicable with retrospective effect (1-4-1962).

Provision under the Income Tax Act1

Now in case of transfer of any assets being share or interest in company situated outside by non-resident can lead to capital gain in India if the underlying assets driving its substantial value from the assets situated in India.

9.(1) The following incomes shall be deemed to accrue or arise in India: –

(i) all income accruing or arising, whether directly or indirectly, through or from any business connection in India, or through or from any property in India, or through or from any asset or source of income in India, or through the transfer of a capital asset situate in India

Explanation 4—For the removal of doubts, it is hereby clarified that the expression “through” shall mean and include and shall be deemed to have always meant and included “by means of”, “in consequence of” or “by reason of”

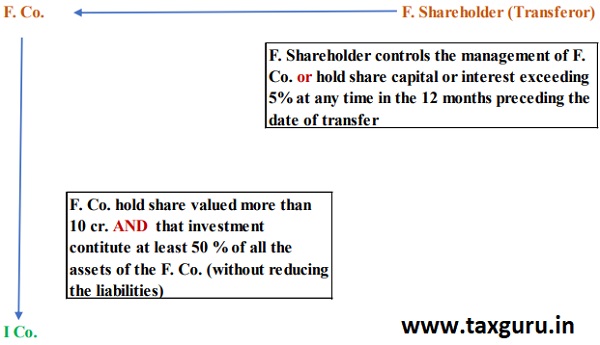

Explanation 5—Any asset being any share or interest in a company or entity registered or incorporated outside India shall be deemed to be situated in India, if the share or interest derives, directly or indirectly, its value substantially from the assets located in India:

Explanation 6— The share or interest, shall be deemed to derive its value substantially from the assets located in India, if, on the specified date (i.e., last date of accounting period preceding the date of transfer or the date of transfer if book value of assets exceeds by 15% from last date of accounting period), the value of such assets

(i) Exceeds 10 Cr. (FMV as per rule 11UB) and

(ii) represents at least fifty per cent of the value of all the assets (FMV as per rule 11UB) of the assets without reducing liabilities) owned by the company or entity.

Explanation 7— no income shall be deemed to accrue or arise to a non-resident from transfer as referred to in the Explanation 5

If the transferor, at any time in the twelve months preceding the date of transfer, neither holds the right of management or control in relation to such company or entity, nor holds voting power or share capital or interest exceeding five per cent of the total voting power or total share capital or total interest, as the case may be, of such company or entity.

Explanation 7 is for exempting small shareholders of foreign entity from indirect transfer provision.

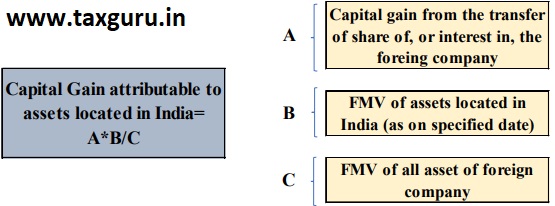

Attribution of Income

In a case where all the assets owned by a company referred to in the Explanation 5, are not located in India, the income of the non-resident transferor, from transfer outside India of a share of, or interest in, such company or entity, deemed to accrue or arise in India under this clause, shall be only such part of the income as is reasonably attributable to assets located in India and determined as prescribed in rules 11UC.

Illustration: Indirect transfer will be applicable only if all the conditions as depicted in the chart are fulfilled

Tax implication of Indirect Transfer under DTAA

As per Section 90(2) of the Act, where the Government of India has entered into an agreement with the Government of another country for avoidance of double taxation, the provisions of the Treaty shall apply to the extent that they are more beneficial to the tax- payer. Therefore, a non-resident has the option to be taxed as per the provisions of the Act or under the tax Treaty between India and the country of which such person is resident, whichever is more beneficial subject to the fulfilling the condition mentioned u/s 90(4).

Generally, DTAA allow to tax the gain on transfer of share in company in the country of which such company or transferor is resident. Below is the exact clause from article 13 of India Singapore DTAA (Just to illustrate).

“4A. Gains from the alienation of shares acquired before 1 April 2017 in a company which is a resident of a Contracting State shall be taxable only in the Contracting State in which the alienator is a resident.

4B. Gains from the alienation of shares acquired on or after 1 April 2017 in a company which is a resident of a Contracting State may be taxed in that State.”

According to the clauses supra gain from share is taxable either in the country in which transferor is a resident or in the country in which the company of which shares are being transferred is resident.

In case of indirect transfer, transferor, and company of which shares are being transferred will usually belong to country other than India therefore this transaction would be out of tax due to beneficial provision in the DTAA. Although, one may investigate the respective DTAAs for the same. Like India – USA treaty does not provide any relief with respect to the capital gains and allow each contracting State to tax capital gain in accordance with the provisions of its domestic law.

Additionally, it may be noted that the benefit under Article 13 of the Treaty is available subject to the fulfilment of the conditions laid down under Article 24A (Limitation of benefits) of the India Singapore Treaty.

Further Impact of article 7 of the MLI with respect of principal purpose test provision need to be analysed to take the benefit under DTAA.

Other Points to consider

> Nothing contained in Explanation 5 shall apply to an asset or capital asset, which is held by a non-resident by way of investment, directly or indirectly, in Category-I or Category-II foreign portfolio investor under the Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations, 2014 or in Category-I foreign portfolio investor under the Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations, 2019.

> If such transfer is deemed to be taxable in India, the calculation of capital gain will be done as per section 48 of the income tax act.

> If shares are transferred within 24 months from the date of acquisition, it will be short term capital gain taxable @ 40% plus applicable surcharge and cess in the hand of nonresident.

> If shares are transferred after 24 months from the date of acquisition, it will be long term capital gain taxable @ 10% plus applicable surcharge and cess in the hand of nonresident.

> As per section 50CA sales consideration of share transferred shall be higher of actual consideration or valuation of share transferred as per method prescribed in rule 11UA, however person referred in rule 11UAD are not required to take valuation report.

> Further the transferee needs to take care of provision of section 56(2)(x).

> Transferee will withhold the tax u/s 195, file the TDS return and file form 15CA/CB in India.

> Non-resident (transferor) will file ITR along with form 3CT.

> Indian company will file form 49D along with ITR.

> Entities covered under treaty benefit are supposed to file a Return of Income. Generally, such transaction involves huge amount, therefore it is suggested to file ROI and claim the benefit of DTAA therein.