How to file Income Tax return when window to file the tax return is closed by Income Tax portal.

31st March, 2021 has gone and the assessee who have failed to file their respective ITR for AY 2020-21 tend to lose their claim of income tax refund what they are eligible for. Section 139 of Income Tax Act allow the assessee to file its ITR on or before the specified due date which is 31st October or 31st July of relevant Assessment year as the case may be. However, assessee can file a belated return also before the end of the relevant assessment year, however beyond that ITR cannot be filed. Most of the people miss this deadline. The reason in most of the cases is that the individual assessee generally is not aware of it . It actually happens largely in NRIs cases where they have income taxable in India and TDS has also been deducted but have failed to file ITR. It results in loss of TDS refund which could have been claimed by filing the ITR.

However, there is another option to file ITR even if the last date of filing has been missed. Section 119 (2)(b) provides that CBDT can authorize income tax authority to admit an application or claim of any refund after the expiry of period specified by the Act. To operationalize this provision, CBDT issued a circular (No. 9/2015) dated 09.06.2015 vide F.No. 312/22/2015 which contains the comprehensive guidelines on the conditions for condonation and the procedure to be followed for deciding such matters.

For those who find difficulties in filing delayed return and whose TDS refund has been stuck due to anomalies of the law, below mentioned is the detailed procedure which can be followed for filing delayed ITR

Stepwise procedure

Step-1: File a manual application to the jurisdictional chief commissioner/principal chief commissioner of the income tax. You can check your jurisdiction in ‘My Profile’ under the tab ‘PAN details’. The application shall be properly addressed to the commissioner and shall contain all the material fact. There must be a valid reason for non-filing the ITR within the due date along with supporting documents. Also, attach a draft computation and mention the amount of refund along with supporting e.g. Form 26AS or Form 16/16A or tax payment challan etc.

Step-2: After submitting an application as above, the jurisdictional commissioner or chief commissioner as the case may be, shall ask for the information regarding your claim. A notice will be issued by the department which can be accessed through ‘e-proceeding portal’ and a reply to the notice may also be submitted online.

Step-3: After due verification of all the information provided by the assessee, the commissioner or principal commissioner as the case may be, shall decide upon merit in accordance with law and shall pass an order under section 119(2)(b). The order will be available under ‘e-proceeding’ tab only and shall also be emailed on the registered email id of the assessee.

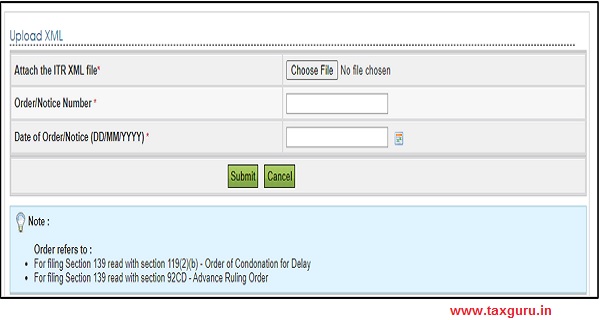

Step-4: After receiving such order, assessee may proceed with filling return as depicted in following images.

Select assessment year and ITR Form and under filing type select ‘u/s 119(2)(b). Thereafter, below screen will appear,

Attach the ITR XML and mention the order number and date of order and submit. The ITR will be filed. The ITR shall thereafter will be processed normally as if the return is filed u/s 139.

Following further points shall also be applicable under section 119(2)(b),

- If the amount of refund claim is less than Rs. 10 lakhs then Principal Commissioner/Commissioner shall be vested with the power of acceptance or rejection of application filed u/s 119(2)(b)

- If the refund claimed is more than Rs. 10 lakhs but less than Rs. 50 lakhs then Principal Chief Commissioner/Chief Commissioner shall have the power to accept or reject the application filed u/s 119(2)(b)

- If the refund claimed is more than Rs. 50 lakhs, then CBDT shall consider such application.

- The application cannot be filed after six years from the end of the assessment year for which such application is made. The application shall be disposed by the competent authority within 6 months as far as possible.

- An application may also be filed for additional amount of refund after completion of assessment for the same, provided all the conditions are fulfilled subject to following further conditions,

- The income of the assessee is not assessable in the hands of other person

- Interest shall not be given on such refund

- The refund should be arisen due to excess TDS/TCS or excess advance tax or access self-assessment tax

About the Author

Author is Amit Jindal, ACA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.

sir i have forget to file a tax bill of july. so is there any way to file that bill now ?

Sir i missed to file itr for fy 20-21 and i have tax liability of approx 1,20,000 can i file condonation of delay u/s 119(2b).

Yes you can file.

sir, i have missed the return of income tax for AY 2020-21 but filed the return for AY 2021-22 is there any way to file the missed return now ? it requred for bank loan ( i have no tax liability or refund )

You can file after obtaining condonation of delay from the Commissioner.

How can i upload Approval copy of condonation of delay u/s 119 (2) (b) along with XML file. plz guide me

As and when you select the section under which you are filing return, it will ask for the order number and attachment of order copy.

Sir please guide me how to file ITR 4 in the new portal for the Asst year 2020-21 after getting condonation of order from I Tax commissioner. we have already received condonation of order to file income tax return for the Asst year 2020-21

You can proceed to normal filing. Just select the section 119(2)(b) and upload the order copy.

Whether the DGIT(Inv) is empowered to condone the delay in filing return of income?

No, the jurisdictional CIT or CCIT can condone.

Whether the DGIT(Inv) is empowered to condone the delay in filing return of income u/s.119(2)b)?

Dear Sir,

Sec 119(2)(b) states “In case where refund claim has arisen consequent to a Court Order, the period for which any such proceedings were pending before any Court of Law shall be ignored while calculating the said period of six years, provided such Condonation application is filed within six months from the end of the month in which such Court Order was issued or the end of financial year, whichever is later.”

In my case the legal case was filed in Court in Mar 2017. The court gave verdict in Mar 2020. However due to pandemic the order was not officially given till Oct 20. Thereafter the implementation of the decision by the Govt authorities took another 9 months to issue instructions for payment.

Now can I file for condonation to CIT as under

1. FY 17-18, 18-19, 19-20 -period the Case was pending before the court of Law

2. FY 11-12 to FY 16-17 – Six previous years as per sec 119(2)(b)

3. OR it will be only six previous years from FY 14-15 to FY 19-20.

Also can I take benefit of Order dated 27th April, 2021 passed by the Hon’ble Supreme Court of India in Misc. Application No. 665/2021 in Suo Motu

Writ Petition (Civil) No. 3/2020 directed that the period of limitation in filing petitions/applications/ Suits/appeals/ all other proceedings, irrespective of the period of limitation under the general or special laws, shall stand extended with effect from 15thMarch, 2020 till further orders. Delay has occured due to pandemic and no fault of mine in not being able to file for condonation application within six months from the end of the month in which such Court Order was issued or the end of financial year, whichever is later.

Please Clarify. Thanks

Nand

Dear Sir

In case of the Assessment years for which court has given its verdict, the date of issuing the order shall be considered as Oct, 2020. So, you could file condonation of delay last till April, 21 (Being 6 months from the end of the month in which said order is issued).

Even if we consider the Supreme Court ruling, the period from 15.03.2020 till 14.03.2021 shall be excluded. In your case it is immaterial because you still had time to file the condonation in April, 21.

For other financial years, rule of 6 years shall be followed.

सर बताएं की ay 2020 -21 की ITR फाइल हो जायेगी 250000/- की

कौन से सेक्शन में अपलोड करू Section 119 of Income Tax Act

कृपा करके बताये बड़ी परेशानी में है लेट होने पे कौन सा सेक्शन चूज करें

आपके आर्टिकल में रिटर्न अपलोड करते समय नोटिस न और डेट का ऑप्शन आ रहा है

आर्डर न नोटिस न कहा से मिलेगा

आपकी बड़ी अपार कृपा होगी

Sir

You can file your ITR u/s 119 but an approval from the Commissioner will be required. Post that you can file your ITR u/s 119 by uploading the approval order.

Sir, I have to file ITR for FY 2019-20 now since I was some urgent issues at home. There is no refund involved, just that I want to file my return. How do I do since e-filing is not an option now?

Yes, you can file. For more details you can contact us through our website.

Can I file Online request to CIT due to Lockdown ? Details If any.

Is 234A & 234F levied in 119(2)b returns?

Yes

Sir maine ITR F.Y.2015-16 ki file kiya tha but wo defective ho gyi thi bt mai notice ka reply nhi de paya tha and F.Y. 2016-16 ki ITR file kiya tha to refund aa gyi bt F.Y. 15-16 ITR invalid ho gyi hai and refund 36550 jo ki abhi tak nhi aayi hai ..to sir condonation of delay ki application file krni hogi..or else koi aur process hai.

F.Y 15-16 ko chhor sare year ki refund and ITR process ho gyi hai.help sir invalid return ko valid me convert condonation of delay application file kr k krna hoga

Yes, you have to file condonation request

Form 67 not filed before the filling of return income 143(1)issued without considering the exemption under DTAA claimed on foreign income under section 90 Can we file application u/s 119(2) (B) seeking condonation of delay in filling Form 67 and to file revised return to claim exemption under section 90

2. my profile jurisdiction is Rajasthan whereas we are filling return of income in karnataka where the business running. whether we have to file application u/s 119(2)(B) in Rajasthan or Karnataka.

Yes, you can file for condonation request for Form 67 as well as revised return. The application shall be filed with Rajasthan jurisdiction first. In Case, you are assessable in Karnataka, then Rajasthan jurisdiction will transfer your file to Karnataka jurisdiction. Or else you have to first file for migration of PAN from Rajasthan to Karnataka.”

Hi D Krishna, did you apply for condonation and was it accepted? I am in the same boat.

Hi did you applied for condonation for foreign 67 , my client have faced the same issue. I am confused whether to follow by applying form 119(2)(b) condonation or through appeal route?

Sir,

My salary income is within exemption limit. No TDS in my account. Can I file my ITR of 2019-20 after 31-Mar-2021 ?

Since there is no claim or tax payable , chances of getting approval are less unless there is strong reason to file the return .

There is a doubt. Kindly clarify whether a person who was posted in Siachen from May of an year till December next year who could not come file ITR by due date or even extended date can file ITR after the portal has closed? He has no refund; in fact he has to pay about excess 12,000/- after all deduction from his pay & TDS on Deposits

You can apply for order u/s 119 post which you can file the tax return.

Hello Sir,

For FY 2008-2009 and 2009-2010, my tax was deducted from monthly salary by MNC. But they submitted it to govt. last year in mid Nov. 2020 after updating PAN in records.

Meanwhile, the demand was raised for my filed return for FY 2018-2019 and 2019-2020.

Now, the tax is also submitted and demand amount is recovered as well from IT return adjustment.

3 times even when I rejected the demand.

How can I get the demand money back which was forcefully adjusted from the IT return?

Please file online rectification u/s 154 .

Hi Taxguru,

I filed my ITR through cleartax on 31st March 2021 and amount of rupees 21269 has also been charged as interest and fees. Is there anyway this can be refunded or waived off?

Can be checked after seeing the tax computation and return filed.

A very informative article

Thanks

Sir

Please advice on what to do if on filed ITR , IT Dept notice of missing 26AS under other source , asked to correct and revice return before 31st mar’ 2021, was missed deadline. Notice came very late and system was very slow on 31st

You can file rectification application u/s 154.

Thank you for writing this article CA Neeraj.

Thanks Mr. Desai.

Thank you for the article. I have a question on Step-1. When you say “a manual application”, should this be submitted as a letter or is this something that can be submitted online? Thanks!

As of now it can be filed manually . But hopefully , CBDT will allow it to be filed online.

Good presentation sir on the subject.

Whether a tax audit case or tax payable case can be filed, after the deadline, for AY 2020-21 or earlier years. In this COVID situation some of assessee have missed the opportunity. Shall we need to wait till the response from CIT is received. Are there any chances of opening the window for some more time U/s139(4), based on representation made by some tax bar associations.

Yes , you can file the same for approval.

In case the return is filed. Can additional claim be admitted under this provision?

Eg. Interest deduction u/s 24(b) not claimed in ITR filed. Can it be claimed u/s 119(2)(b) ?

Yes you can file the application for approval with additional claim .

whether Normal belated Indl.(otherthan NRI) can file return after 31 March with interest ?

You have to file application with jurisdiction AO asking for approval to file . Once you have an approval , then you can file.