E-ASSESSMENT SCHEME, 2019

NOTIFICATION NO. 61, DATED 12.9.2019

NOTIFICATION NO. 62/2019, DATED 12.9.2019

(Directions for giving effect to Income Tax E-assessment Scheme, 2019 by sub-section (3B) of section 143 of the Income-tax Act, 1961)

In exercise of the powers conferred by sub-section (3A) of section 143 of the Income-tax Act, 1961 Govt.

INTRODUCED a scheme of faceless e-assessment. The scheme seeks to eliminate the human interface between the taxpayer and the income tax department.

Que.- 1 OBJECTIVE OF E- ASSESSMENT SCHEME 2019:-

- This he scheme seeks to eliminate the human interface between the taxpayer and the income tax department.

- For carry out a faceless assessment through electronic mode.

- To reduce the scope for corruption and potential overreach by tax officials.

- To minimization time of Tax litigation which is 10 to 15 year at present

- To increase the Tax Revenue

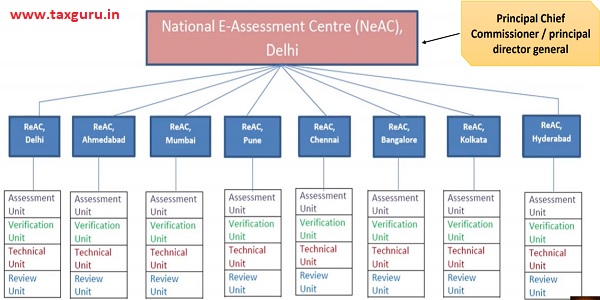

Scope Of This Scheme – CBDT Will Set Up Assessment Centers

IMPORTANT DEFINITIONS FOR EXAMS

“Assessment” means assessment of total income or loss of the assessee under sub-section (3) of section 143 (Regular & Scrutiny Assessment) of the Act

Automated allocation system” means an algorithm/ System/ Process for randomised allocation of cases, by using suitable technological tools, including artificial intelligence and machine learning, with a view to optimise the use of resources

Automated examination tool” means an algorithm for standardised examination of draft orders, by using suitable technological tools, including artificial intelligence and machine learning, with a view to reduce the scope of discretion.

E-Assessment” means the assessment proceedings conducted electronically in ‘e-Proceeding’ facility through assessee’s registered account in designated portal ( Portal –www.Incometaxindiaefilling.gov.in )

Registered mobile number” of the assessee means the mobile number of the assessee, or his authorised representative, appearing in the USER PROFILE of the electronic filing account registered by the assessee in designated portal

“Video telephony” means the technological solutions for the reception and transmission of audio-video signals by users at different locations, for communication between people in real-time.

Mobile app” shall mean the APPLICATION SOFTWARE OF THE INCOME-TAX DEPARTMENT DEVELOPED FOR MOBILE DEVICES which is downloaded and installed on the registered mobile number of the assessee

Registered e-mail address” means the e-mail address at which an electronic communication may be delivered or transmitted to the addressee, including-

1. The email address available in the electronic filing account of the addressee registered in designated portal; or

2. The e-mail address available in the last income-tax return furnished by the addressee; or

3. The e-mail address available in the Permanent Account Number database relating to the addressee; or

4. In the case of addressee being an individual who possesses the Aadhaar number, the e-mail address of addressee available in the database of Unique Identification Authority of India ;or

5. In the case of addressee being a company, the e-mail address of the company as available on the official website of Ministry of Corporate Affairs; or

6. Any e-mail address made available by the addressee to the income-tax authority or any person authorised by such authority.

Appellate Proceedings.– An appeal against an assessment made by the National e- assessment Centre under this Scheme shall lie before the Commissioner (Appeals) having jurisdiction over the jurisdictional Assessing Officer and any reference to the Commissioner (Appeals) in any communication from the National e-assessment Centre shall mean such jurisdictional Commissioner(Appeals).

Authentication of electronic record:- An electronic record shall be authenticated by the originator by affixing his digital signature in accordance with the provisions of sub-section (2) of section 3 of the Information Technology Act, 2000 (21 of 2000):

1. E-assessment Centres – (1) For the purposes of this Scheme, the Board may set up-

(i) A National e-assessment Centre to facilitate the conduct of e-assessment proceedings in a centralised manner, which shall be vested with the jurisdiction to make assessment in accordance with the provisions of this Scheme;

(ii) Regional e-assessment Centres as it may deem necessary to facilitate the conduct of e-assessment proceedings in the cadre (small group) controlling region of a Principal Chief Commissioner, which shall be vested with the jurisdiction to make assessment in accordance with the provisions of thisScheme;

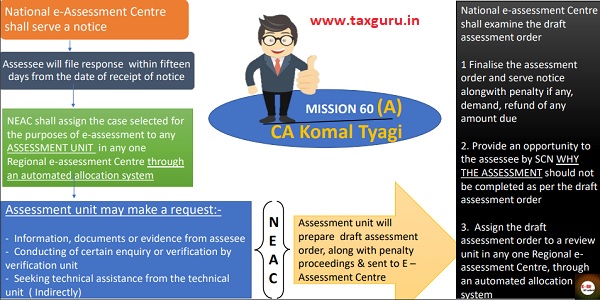

(iii) Assessment units, as it may deem necessary to facilitate the conduct of e- assessment, to perform the function of making assessment, which includes identification of points or issues material for the determination of any liability (including refund) under the Act, seeking information or clarification on points or issues so identified, analysis of the material furnished by the assessee or any other person, and such other functions as may be required for the purposes of making assessment;

(iv) Verification units, as it may deem necessary to facilitate the conduct of e- assessment, to perform the function of verification, which includes enquiry, cross verification, examination of books of accounts, examination of witnesses and recording of statements, and such other functions as may be required for the purposes of verification.

(v) Technical units, as it may deem necessary to facilitate the conduct of e-assessment, to perform the function of providing technical assistance which includes any assistance or advice on legal, accounting, forensic, information technology, valuation, transfer pricing, data analytics, management or any other technical matter.

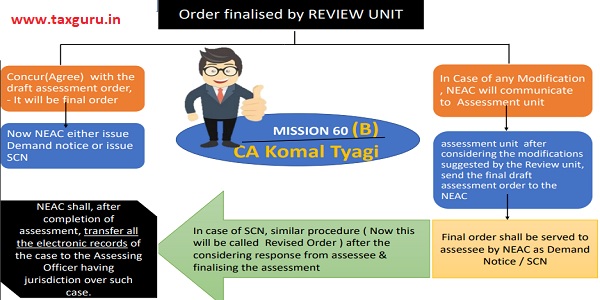

(vi) Review units, review of the draft assessment order, checking relevant and material evidence, Consideration of issues on which addition or disallowance should be made in the draft order, judicial decisions have been considered and dealt with in the draft order, checking for arithmetical correctness of modifications and such other functions as may be

Procedure For Assessement under This Scheme

–

Powers of Jurisdictional Assessing Officer:

- Imposition of penalty;

- collection and recovery of demand;

- rectification of mistake;

- giving effect to appellate orders;

- submission of remand report, or any other report to be furnished, or any representation to be made, or any record to be produced before the Commissioner (Appeals), Appellate Tribunal or Courts, as the case may be; proposal seeking sanction for launch of prosecution and filing of complaint before the Court;

- However, the National e-assessment Centre may at any stage of the assessment, if considered necessary, transfer the case to the Assessing Officer having jurisdiction over such case

POINTS TO BE REMEMBER:-

1. Penalty proceedings can be initiated by the assessment unit through National E-assessment center in case of non-compliance of any notice, direction or order.

2. All the above communication shall take place through electronic communication which will be served either in the electronic portal or e-mail id or mobile app and a real time alert.

3. No personal appearance in the process, but an assessee can request for personal hearing of the same through Video conference facilities.

4. E-assessment is not a special type of assessment. All the current assessments can be carried out in an electronic manner

Questions

1. What is the Objective of this scheme

2. How many National centre in India

3. How many Regional centre in India

4. Selection process (sequence, sampling , Random) A, b, c,

5. Assessee reply timing (10 Days, 15 Days, 30 Days) A, b, c,

6. Who is the incharge of NEAC ( AO, CI, CCI, PCCI) A, b, c, d

7. Can at any stage National e-assessment Centre may transfer the case to the Assessing Officer having jurisdiction over such case? Yes or No

8. Can Assessment Units / Centres directly ask for technical support from Technical units Yes or No

9. Under this scheme all communication shall take place through electronic communication except documents management / documents delivery Yes or No

Author Bio

Excellent presentation and recently i had gone through this whole process its very transparent and techno save people with accurate knowledge of Law and legal terminology can only do that, so its not everybody cup of tea. Now there will be no vested interest of Officers or any authorities and totally scrutiny cases will be done on Merit basis. Must say its an Bold move by CBDT

are kuch samaj nahi aa raha