Due to persisting COVID-19 pandemic and challenges faced by taxpayers, Government has further extended dates for various direct tax compliances. These are notified at regular intervals from time to time. Article compilesExtended due dates of filing TDS / TCS Returns : Quarterly, Extended due date of furnishing Form 16 / Form 16A: Quarterly & Annually, Extended due of Filing Income Tax Returns: Annually, Extended due dates of filing Annual Income Tax Forms, Extended due dates of Income Tax Assessment & Appeals and Extended due dates of Various Payments under Income Tax Act, 1961.

“Extended due dates– Returns”

Page Contents

- Extended due dates of filing TDS / TCS Returns :Quarterly

- Extended due date of furnishing Form 16 / Form 16A: Quarterly & Annually

- Extended due of Filing Income Tax Returns: Annually

- Extended due dates of filing Annual Income Tax Forms

- Extended due dates of Income Tax Assessment & Appeals:

- Extended due dates –Payments under Income Tax Act, 1961

Extended due dates of filing TDS / TCS Returns :Quarterly

Note:

- As per currently stated, the due date for the quarter ended 31st December, 2020 (October 2020 to December 2020) will continue to be 31st January, 2020 until further stated.

- These due dates stated above are for regular TDS/TCS returns.

- For returns covered by section 194IA/IB /M the due date for the month of February 2020 or March 2020 will be 31.07.2020 instead of current due date of 30.06.2020.

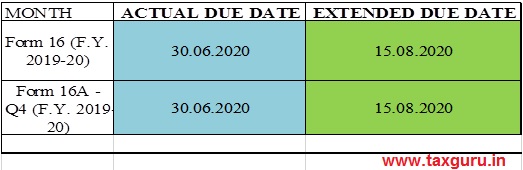

Extended due date of furnishing Form 16 / Form 16A: Quarterly & Annually

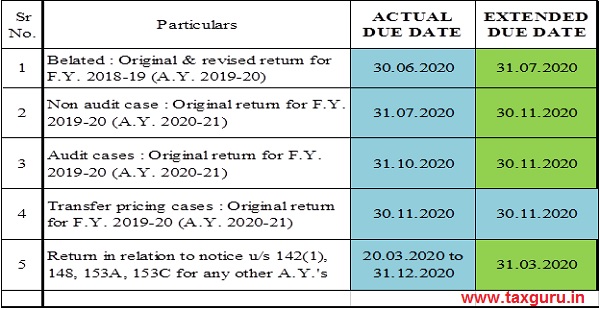

Extended due of Filing Income Tax Returns: Annually

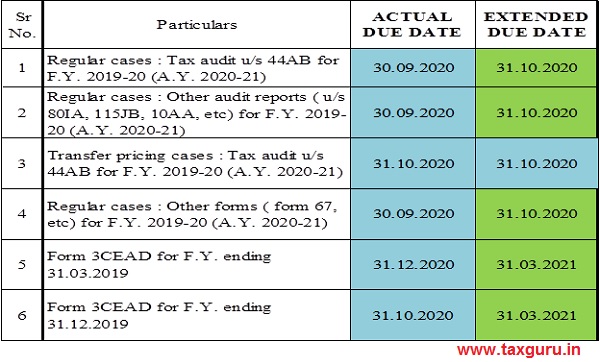

Extended due dates of filing Annual Income Tax Forms

Direct tax forms: Annually

Extended due dates of of Other Income Tax Compliance: Annually / One time

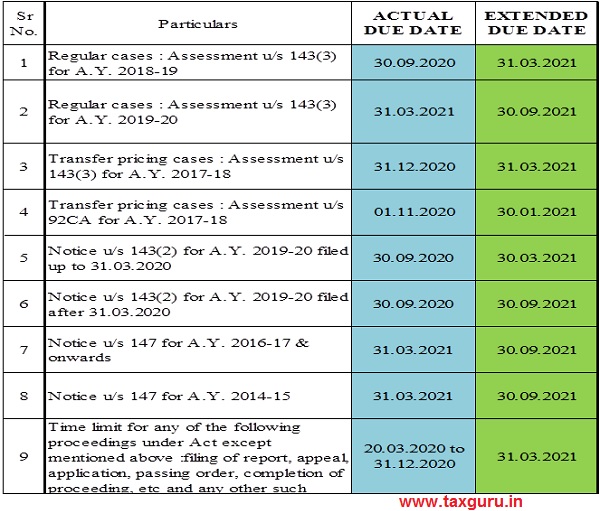

Extended due dates of Income Tax Assessment & Appeals:

Note:

The scrutiny assessment u/s 143(3) for A.Y. 2017-18 is already time barred on 31.12.2019 and there is no further extension for the same.

Extended due dates –Payments under Income Tax Act, 1961

Direct tax Compliance:

TDS/ TCS payment:

- There has been no extension in the original due dates of TDS payments. However, there has been reduction in the tax rates for about 25% from the original tax deduction rates. Also, there has been relief in the interest rate in delayed payment of taxes under TDS/ TCS (including for F.Y. 2018-19 (A.Y. 2019-20))

- The normal rate of interest would be levied as per applicable provisions for payment of taxes made after 30.06.2020.

- The reduced rates are applicable only to the mentioned sections on press release dated 12.05.2020.

- There shall be no reduction in rates in case of deduction in case of non-furnishing of PAN/ Aadhaar.

Advance Tax payment:

- The liability of advance tax may increase due to change in TDS/TCS rates and accordingly the differential tax needs to be paid after recalculating.

- There is no revision in the dates of payment of Advance Tax.

Interest on Tax payment:

- Interest u/s 234A would be levied only after the due dates mentioned above.

- Interest u/s 234A would not be levied if net tax payable after allowing credit of TDS, MAT, etc. is Rs 1 lakhs or less paid till 30.11.2020.

- There has been reduction in the rate of interest levied in case of delayed payment of taxes. Reduced rate of 9% is applicable. The normal rate of interest would be levied as per applicable provisions for payment of taxes made after 30.06.2020. The reduced rate is applicable for interest on delayed payments of advance tax, self-assessment tax, etc. including for F.Y. 2018-19 (A.Y. 2019-20).

“Extended due dates –Other”

Other:

- The board has deferred the implementation of new procedure for registrations u/s 12AB & 80G from 01.06.2020 to 01.10.2020. Therefore, the old procedure will apply till 30.09.2020.

For further details and discussions, kindly reach out to us: E-mail: info@mdbassociates.in

Disclaimer: The content of this article are for information purposes only and does not constitute advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer to relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc. before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author Bio