The union budget 2020 has introduced new income tax slabs for individual and HUF taxpayers and it came into effect from April 1, 2020. This gives the option to either continue with the existing tax regime or opt for the new tax regime sans 70 tax exemptions and deductions.

Salaried employees, having no business income, will have to choose between the existing and new tax regime every financial year, as per their convenience.

However, who have business income should carefully evaluate whether they want to continue with the existing tax regime or opt for the new tax regime. This is because once they opt for the new tax regime, then they can switch back to the existing tax regime only once in a lifetime.

We will discuss about the following topics in this article:

1. What’s there in the new tax regime?

2. What are the conditions to avail it and who can opt it?

1. What’s the new tax regime?

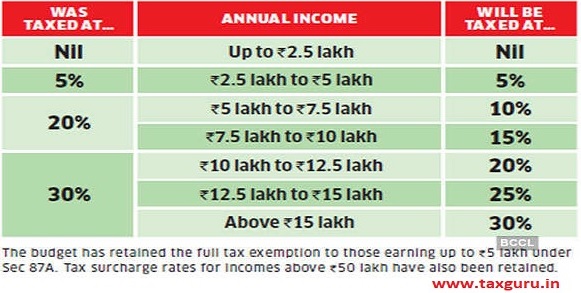

The new personal income tax regime comes up with a new income tax slab for individuals which is attached below:

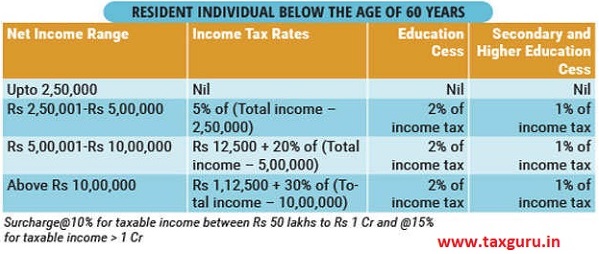

While previously we had the below income tax slabs prevalent:

So, it’s pretty evident that while the old regime had different tax slabs for different age groups,new tax regime does not provide the varied tax slabs on basis the age groups.

2. What are the conditions to avail the new regime and who can opt it?

- Any individual can opt the new tax regime, meaning to say that the new regime is an optional regime and individual taxpayers can choose between the old and new tax regime.

- Further, where the taxpayer earning income from business has opted for the new regime for any year and withdraws it in any subsequent year, cannot opt for the new regime again and has to follow the old tax slabs only. However, other individual taxpayers can choose between the regimes every year.

- CBDT circular issued on April 13, 2020 has directed all the employers to obtain a declaration from employees, if they wish to opt for the new tax regime. However, employees will still continue to have the right to choose between the tax regimes at the time of filling the return.

- Individuals opting for the new regime has to forego certain exemptions and deductions which were available with the old regime.

Here’s a list of the main exemptions and deductions that tax payers will have to forgo if they opt for the new regime.

– Leave travel allowance exemption which is currently available to salaried employees twice in a block of four years.

-House rent allowance normally paid to salaried individuals as part of salary.

– Standard deduction of Rs. 50000/- currently available to salaried tax payers.

– Deduction available under 80TTA/80TTB will not be available to the taxpayers.

– Deduction for entertainment allowance ( for government employees) and employment/ professional tax as contained in section 16.

– Tax benefit u/s 24 on interest paid on housing loan taken for a self-occupied or vacant house property.

– Deduction of Rs. 15,000/- allowed for family pension.

– The most commonly claimed deductions under section 80C will have to forgone.

However, deduction under sub-section (2) of section 80CCD and 80JJAA can still be claimed.

– Deduction claimed for medical insurance premium under section 80D will also not be claimable.

– Tax benefits for disability under section 80DD and 80DDB will not be claimable.

– Tax on interest paid for education loan under 80E will not be claimable.

– Tax break on donations to charitable institutions available under section 80G will not be available.

So to conclude it, individuals will have to work out their tax liability under the old and new tax regime before deciding which one is more beneficial.