Gift is usually used to convert black money into white money. To stop practice of converting black money into white money a section 56(2)(Vii) introduced by Finance Act , 2009 and amended by Finance act , 2010. This section deals with law of taxation of gift.

The term “Gift” implies – any sum of money or property received by an individual or a HUF without consideration or a property acquired for inadequate consideration.

From the taxation point of view, the Taxability of Gifts received by an Individual / HUF can be classified as follows:

1. Any sum of money received without consideration, it can be termed as ‘monetary gift’.

2. Specified movable properties received without consideration, it can be termed as ‘gift of movable property’.

3. Specified movable properties received at a reduced price (i.e. for inadequate consideration), it can be termed as ‘movable property received for less than its fair market value’.

4. Immovable properties received without consideration, it can be termed as ‘gift of immovable property’.

5. Immovable properties acquired at a reduced price (i.e. for inadequate consideration), it can be termed as ‘immovable property received for less than its stamp duty value’.

The meaning of Property is defined as under :-

- Immovable Property being land or Building or both

- Shares and Securities

- Jewellery

- Archaeological Collections

- Drawings

- Paintings

- Sculptures

- Any other work of Art.

If a person receives gifts (either in cash or in kind) from any person, gift tax would be levied and to be paid by the person receiving the gifts. Such income would be taxable in the year in which the gift is received and taxable under the head “Income from Other Sources” .

After adding this to total income, the gross total income would be computed and the tax would be levied on the gross total income as per the Income Tax slab rates.

Page Contents

- Exemption from Levy of Income Tax on Gifts under different scenarios :

- 1. Gifts received from Relatives :

- 2. Gifts received From Non-Relatives :

- 3. ON THE OCCASION OF MARRIAGE OF THE INDIVIDUAL :

- 4. Tax treatment of immovable / movable property received as gift by an individual:

- 5. GIFTS RECEIVED UNDER A WILL OR BY WAY OF INHERITANCE OR IN CONTEMPLATION OF DEATH OF THE PAYER :

- 6. Gifts received from any Local Authority as defined in Section 10(20) :

- 7. Gifts received under Section 12AA :

Exemption from Levy of Income Tax on Gifts under different scenarios :

1. Gifts received from Relatives :

As per the Income tax act, the Gifts received from any of the relatives, whether Resident or Non – Resident (NRI) are fully exempt from tax. Whether it is in the form of Cash, Cheque or any goods. The receiver would not be liable to pay the tax for these gifts. In case of HUF, Money received by a HUF from its members, is exempted from taxes.

Here is the term “relatives” as defined by the Income Tax act as follows:

- Spouse of the individual

- Brother or sister of the individual

- Brother or sister of the spouse of the individual

- Brother or sister of either of the parents of the individual

- Any lineal ascendant or descendant of the individual

- Any lineal ascendant or descendant of the spouse of the individual, Spouse of the person mentioned above.

2. Gifts received From Non-Relatives :

Here non-relatives mean anyone who doesn’t come under the above mentioned list of relatives. If the aggregate value of gifts (whether in cash or in kind) received from a person or persons (except relatives as specified above) in any financial year does not exceed Rs. 50,000/-, then such gifts are not liable to Gift Tax. However, if the value of gifts received exceeds Rs. 50,000/-, then the entire gift so received is taxable as Income from other sources. In case of HUF, value of gifts (whether in cash or in kind) received by a HUF from non- members, shall not be liable to tax, if the same is below Rs. 50,000/-, but shall be taxed if the value of the gifts exceeds Rs.50,000/-.

3. ON THE OCCASION OF MARRIAGE OF THE INDIVIDUAL :

One very happy feature of the provision of taxation of gifts is that ANY gift received from any person on the occasion of the marriage of the receiver of the gift, would not be liable to income tax. There is no monetary limit attached to this exemption. It should be noted that, if anyone receives any gifts (from non-relatives) at the time of engagement or the marriage anniversary, then such gifts (above Rs.50,000) shall be liable to tax. It has also been clarified that the gifts received by a person on his own marriage are exempted and not on the marriage of their son/daughter/brother/sister.

4. Tax treatment of immovable / movable property received as gift by an individual:

Gift Tax on Property (as described above) received in kind would be levied in the following manner:-

- In case the property is received without any consideration being paid by the receiver of the gift, the stamp duty value/fair market value of the property would be taxable (provided the stamp duty value exceeds Rs. 50,000).

- In case inadequate consideration is being paid by the receiver of the gift, and the difference between the part payment made and the stamp duty value/fair market value is more than Rs. 50,000/-, such difference would be taxable.

Note : In case of Immovable Properties, the stamp duty value would be considered and in case of Movable Properties, the fair market value would be considered.

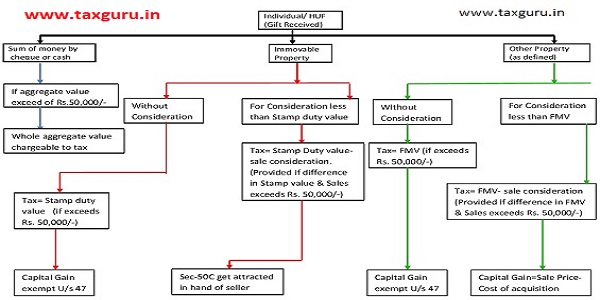

Analysis of Section- 56(2)(Vii) Read with section of Capital Gain Section 50C, Sec-47.

I. Any transfer of capital assets under gift, will or an irrevocable trust is not taxable under head Capital Gain. It is not regarded as transfer U/s 47.

II. Any distribution of capital assets on the partial or total partition of a Hindu Undivided Family is not taxable under head Capital Gain. Because it is not regarded as transfer U/s 47.

III. As per Sec-50C, where the consideration received or accruing as a result of the transfer by an assessee of a capital asset, being land or building or both, is less than the value adopted or assessed or assessable by any authority of State Government for the purpose of payment of stamp duty, such value deemed as full consideration.

Graphical representation of above provisions.

Example of above discussed provisions :-

1. Akshay has a property, which he has purchased on 01-04-2018 of Rs. 10,00,000/-. Later on he gifted the property to Aarti (Donee) on 31-03-2019. On date of gift Stamp duty/Fair market value of said property was Rs. 25,00,000/-.What is tax implication in the hands of Akshay (Donor) and Aarti (Donee).?

Solution-

In the hands of Akshay (Donor)

There is no capital gain tax in the hands of Akshay because gift transfer is exempted U/s 47 of the income tax act and other reason is that there is no sale price exist.

In the hands of Aarti (Donee)

Gift is taxable in the hands of Aarti under the head “Income from other sources” under section 56(2)(Vii). Because stamp duty value/ Fair market value of the property is in excess of Rs. 50,000/-. Hence whole stamp duty value/ Fair market value is taxable in the hand of Aarti .i.e 25,00,000/- is taxable.

2. In above example if Akshay sold property to Aarti at Rs. 20,00,000/-. Other things remains same then what tax implication in the hands of Akshay and Aarti.?

Solution-

In the hands of Akshay

If property sold is an immovable property then Section 50C would be applicable, hence Capital Gain = 25 lakh-10 lakh= 15 lakh is taxable.( Subject to indexation)

If property is other than immovable property then section 50C does not apply, hence Capital gain = 20 lakh- 10 lakh .i.e 10 lakh is taxable.

In the hands of Aarti-

Stamp Duty value or fair market value of the property is excess of Rs. 50,000/-. Consideration paid is less than stamp duty value/ fair market value and difference between stamp duty value/ fair market value is in excess of Rs. 50,000/-. Hence it is taxable in the hands of Aarti.

Taxable amount = 25 lakh – 20 lakh = 5 lakh is taxable under the head “Income from other Sources”

In following cases, gift of property will NOT be charged to tax :

- Property received from relatives (Relatives – as described above)

- Property received on the occasion of the marriage of the individual.

- Property received under will/ by way of inheritance.

- Property received in contemplation of death of the donor.

- Property received from a local authority [as defined in Explanation to section 10(20) of the Income-tax Act, 1961].

- Property received from any fund, foundation, university, other educational institution, hospital or other medical institution, any trust or institution referred to in section 10(23C).

- Property received from a trust or institution registered under section 12AA.

Tax on Property received as Gift would only be levied in case of the above mentioned properties. Thus, in case any property is not listed above, tax on those properties received as gift would not be levied. Examples of such properties on which gift tax would not be levied are Cars, Laptops, and Mobiles etc.

5. GIFTS RECEIVED UNDER A WILL OR BY WAY OF INHERITANCE OR IN CONTEMPLATION OF DEATH OF THE PAYER :

Any amount received under a will or by way of inheritance or in contemplation of death of the payer is fully exempted in the hands of the person receiving the gift. There is no maximum limit in this case and the whole gift received is considered as tax free.

6. Gifts received from any Local Authority as defined in Section 10(20) :

Gifts received from any Local Authority as defined in Section 10(20) are exempted from taxes.

7. Gifts received under Section 12AA :

Gifts received from any fund or foundation or university or other education institution or hospital or other medical institution or any other trust or institution referred to in Section 10(23C) or Gifts received from any fund or Institution registered under Section 12AA are exempted from taxes.

Capital Gains on Property received/transferred as Gifts

In the hands of the person giving the gift :

If a person gives gift to another person, then such gift would not be regarded as transfer and therefore no capital gains would arise in the hands of the transferor i.e. the person who is giving the gift. And therefore, at the time of giving the gift, no tax would be required to be paid by the person giving the gift.

In the hands of the person receiving the gift :

- The Cost of acquisition in the hands of the person receiving the gift – would be the same as the cost of acquisition in the hands of the person who gave the gift.

- For the computation of period of holding in the hands of the receiver would be determined – from the period of holding / date of buying of the gift by the gift giver to the date of selling of the said gift by the receiver.

Therefore, the above provisions of Gift Tax, under the Income Tax Act, 1961 shall get attracted if an Individual / HUF receives gifts or sales the property, received as gifts by them.

CONCLUSION:-

Whenever you receive anything without consideration or for inadequate consideration, just check from whom it is received and when it is received and the value of such gift.

SOURCE:- Income tax Act, Section 56(2)(vii)

Author is a Practicing Chartered Accountant in kolkata in own proprietorship S. Meharia & Associates and can be reached on mail casonalmeharia@gmail.com.