Working capital is a common measure of a company’s liquidity, efficiency, and overall health. It is the cash available for day-to-day operations of an organization. There are some apprehensions that in GST regime, the working capital requirements will increase. Let us check the truth with some practical transactions like stock transfer, import under Advance Authorization, Advance payments, supplies to Government & its agencies – TDS, Samples on Approval basis – Returnable / Non- Returnable, Inverted Duty Structure etc.

Page Contents

- Ø Impact of Working Capital on Stock Transfers:

- Ø Opportunity to Re-Design Supply Chain Network:

- Ø Impact of Working Capital on import under Advance Authorization:

- > Impact of Working Capital on Advance Payment :

- > Impact of Working Capital on TDS:

- Ø Impact of Working Capital on Samples on Approval basis

- Ø Impact of Working Capital due to Inverted Duty Structure :

- Ø Conclusion

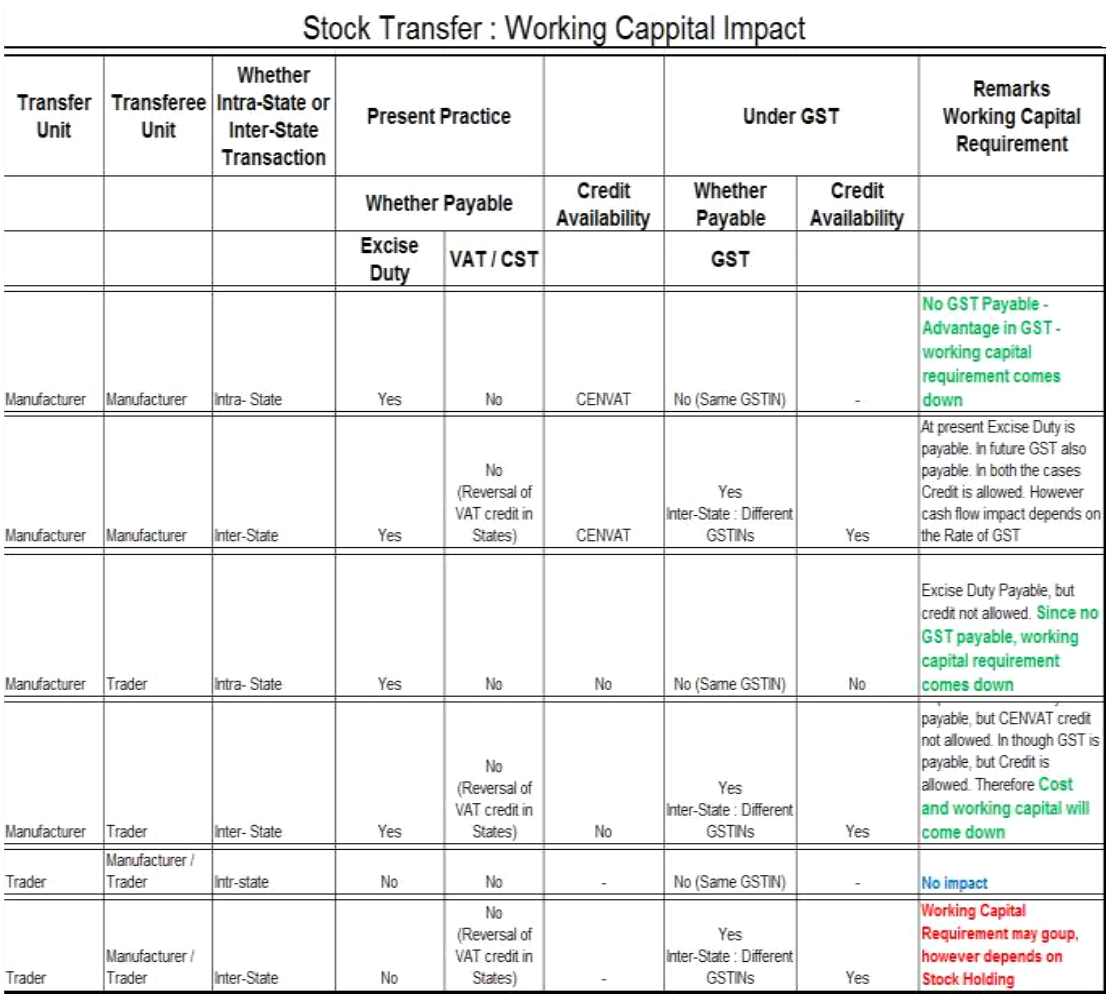

Ø Impact of Working Capital on Stock Transfers:

Stock transfer refers to moving of goods from one part of the distribution chain to another of same legal entity. An internal purchase order is created for stock transfer between branches and warehouses. Since stock transfer happens between units of the same legal entity, there shall not be any sale.

Present Practice:

At present under Central Excise, a registered manufacturer making a stock transfer of excisable goods, should pay excise duty on 100% +10% of cost of production. If the transferring units are only trading units and not manufacturing, then no excise duty payable.

Such transfers against Form F, doesn’t attract VAT / CST as there is no sales involved. However, input VAT on purchase of goods should be reversed at certain percentage which differs from state to state.

In GST Regime:

In GST regime, payment of tax on stock transfer depends on whether the supplying and receiving units are in the same state or not. In case both the units are in the same state and have same GSTIN, then no GST is payable. On the other hand if the units are situated in different states, then each unit to register separately in the respective states and therefore GST payable on such supplies.

Working Capital impact depends on whether the transaction is intra-state or inter-state, type of supplier & recipient, number of day’s stock holding, GST rate etc. For hypothetical consideration, various options are charted down as below and their impact on working capital is analyzed.

Stock Transfer : Working Capital Impact

It is observed that generalization and media circulation that working capital requirement in case of stock transfer in GST regime will increase is not true. In fact working capital requirement may even reduce in case transactions are within the state (Intra-State) with same GSTIN. One of the finer features of the proposed Goods and Service Tax Law (GST) is admissibility of seamless input credit across entire value chain.

Therefore even in inter-state transactions if the inventory turnover is high (means less stock holding days) resulting faster utilization of credit, the working capital requirement minimizes.

Overall, in most of the cases, for stock transfer, the working capital requirement in GST regime may come down considering reversal of VAT credit applicable in some states.

Ø Opportunity to Re-Design Supply Chain Network:

Supply chain network design is a powerful modeling approach proven to deliver significant reduction in supply chain costs and improvements in service levels by better aligning supply chain strategies. A variety of factors—ranging from cost structures, tax laws, skills and material availability, new market entry and others—have driven companies to redesign and reconfigure their supply chains continually.

Present Practice :

At present supply chain in India is mostly driven by factor of tax efficiency. Simply to save CST on inter-state sales, warehouses are being created in almost every state. Goods are stock transferred to these locations where no CST is applicable, however, trading off logistics & warehousing costs. This is to enable the business to do billing with local VAT which allows buyer in the respective state to get the credit.

In GST Regime:

With the seamless flow of input tax credit across state borders in GST, the need for businesses to open multiple branches or warehouses across states is no longer required. They may have to re-design supply chain network only from the perspective of logistic and business operational convenience and efficiency and not from tax point of view. The effective planning and redesign of warehousing may scale down the number and scale up in size (consolidation), and subsequently cut down the stock transfer operations drastically. As a consequence of which working capital requirement surely comes down.

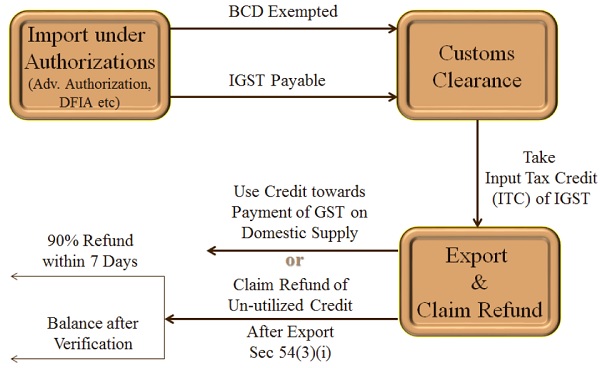

Ø Impact of Working Capital on import under Advance Authorization:

The objective of the schemes is to enable duty free import of inputs for export production. Advance Authorization is issued as per guidelines of Chapter 4 of the Foreign Trade Policy.

Present Practice:

All the Customs Duties are exempted as per para 4.14 of Foreign Trade Policy including CVD (levied under Sec 3(1) of Customs Tariff Act 1975) & SAD (levied under Sec 3(5) of Customs Tariff Act 1975). Therefore there is no cash outflow when imported under Advance Authorization. (Notification No. 18/ 2015 –Customs; Notification No. 20/ 2015 — Customs — Annual requirement; Notification No. 21/ 2015 — Customs, 1st April, 2015 — Deemed Exports)

In GST Regime:

These two duties (CVD (levied under Sec 3(1) of Customs Tariff Act 1975) & SAD (levied under Sec 3(5) of Customs Tariff Act 1975) are subsumed in GST. However import under Advance Authorization is exempted from Basic Customs Duty (BCD) only. IGST is payable. However, the same can be taken credit and may be utilized for supplies in domestic market or can be claimed refund. See the Exhibit below. (However corresponding amendments in FTP & Customs Notifications are still expected). Since importers under the scheme have to pay first IGST, then after even though allowed credit, it may increase working capital requirement.

Imports under Advance Authorization

Impact Increased requirement and blockage of working capital & Cost.

This is an appropriate and right measure to streamline misuse of Export Benefits by most of the unscrupulous exporters. Taking advantage of para 4.22 of FTP, which stipulates Export Obligation period of 18 months, exporters are importing required inputs as per SION (raw materials, Consumables, packing materials) in advance under the scheme and diverting the materials for domestic supply and casually discharging export obligation. Though Actual User Condition as per para 4.16 is attached the authorization, and procedures for Maintenance of Proper Accounts (para 4.51 of HB) and Monitoring of Export Obligation (4.44 of HB) are prescribed in Hand Book of Procedures (Vol -1), no DGFT authorities or Customs officials are bothered to verify giving exporters sheltered wrong doings and this may surely overshoot scams of scams if probed. Therefore exporters are most worried lot for GST roll out.

Work Capital Analysis:

Let us now analyze whether import under Advanced Authorization on payment of IGST is really impact the working capital.

Exports & Domestic Supply – Impact of Working Capital:

In case importer under the scheme has both Exports and Domestic supply, then he can utilize the IGST credit (accrued from payment of IGST on Import under Advance Authorization). If the Domestic supplies are significant value (say above 55%), then total credit of above IGST can be utilized towards output tax. So that the working capital impact is minimal.

Adverse working capital impact however can be seen only when exports are overshoot the domestic supply. However, provisions are made in the GST law to provide refund of 90% of the value within 7 days (Sec 54(3)(i))

> Impact of Working Capital on Advance Payment :

Present Practice:

By virtue of the provisions in Section 65 (105) and 67 of the Finance Act, 1994, the Government has levied service tax on “advances” received towards rendering of taxable services and the said liability has to be discharged, as soon as the advances are received, even before the actual rendering of the service.

The provision of Tax on advance is applicable only in case of services and not for goods, therefore excise and VAT / CST need not be paid on advances received.

In GST Regime:

As per Sec 31(3)(d) of CGST Act, the recipient of advance issues a receipt voucher evidencing receipt of such payment and make payment of tax to that extent. Unlike in the present (applicable only to services), GST on advance receipts is payable irrespective of goods or services. That means cash outflow on account of tax on advance payment received and the same is allowed to be adjusted only at the time of issue of invoice against supplies. Impact – Increased requirement and blockage of working capital & Cost.

However no input tax credit is allowed to recipient of supplier till he is received supplies and in possession of invoice.

Impact : Increased requirement and blockage of working capital & Cost.

> Impact of Working Capital on TDS:

Present Practice:

There is no such provision to deduct tax at source by government authorities for supplies to them.

In GST Regime:

Tax Deduction at source (TDS) provisions are incorporated in GST law as per Sec 51 of CGST Act. Accordingly Central Government or State Government; or local authority; or Governmental agencies deduct tax at the rate of one per cent from the payment made or credited to the supplier. Though the supplier can claim credit after he receives the TDS certificate, money is blocked to that extent. However TDS provisions are applicable only in case of Intra-state supplies and no TDS on inter – state supplies.

Tax Deduction at Source (TDS) by Govt. Dept or Local Authority

Sec 51 of CGST

Provided that no deduction shall be made if the location of the supplier and the place of supply is in a State or Union territory which is different from the State or as the case may be, Union territory of registration of the recipient (Inter-state). For the purpose of deduction of tax specified above, the value of supply shall be taken as the amount excluding the central tax, State tax, Union territory tax, integrated tax and cess indicated in the invoice.

Ø Impact of Working Capital on Samples on Approval basis

Present Practice:

At present excise duty is applicable even on samples removed from factory premises, however no VAT / CST payable as there is no sales.

In GST Regime:

Under GST provisions supply of samples (irrespective of whether – returnable / non-returnable) also considered as supply and therefore attracted tax and to that extent working capital impact may be seen. Mostly pharmaceutical industry and garments industry is impacted due to this.

Ø Impact of Working Capital due to Inverted Duty Structure :

Inverted duty structure refers to taxation of inputs at higher rates than finished products that results in build-up of credits and cascading costs. Example excise duty on commercial vehicles is 8%, the inputs used in their manufacture are taxed at 12.5% resulting in accumulation of CENVAT credit.

Present Practice:

At present, Central Laws do not provide for any refund of credit accumulation on account of differential tax rates, particularly when the rate of tax on inputs is more than rate of tax on output.

In GST Regime:

Industry has been demanding for over a long time that government should remove the anomalies with regard to taxation arising inverted tax. To relief the industry from such situations, special provisions are made to get refund of un-utilized credit under Sec 54(3)(ii). This provision not only reduces the cost, but greatly reliefs working capital blockage.

Ø Conclusion

As see from the analysis above, it only a myth that with the roll out of GST working capital requirements will go up. With better planning and re-design of supply chain network, the need for stock transfers will come down, resulting in reduction in working capital. GST also enables better planning, budgeting and cost management to bring down stocks held in godowns.

Though working capital requirement in case of import under Advance Authorization, advance payments, Tax Deduction at Source (TDS) may go up, the objective is to bring in certain discipline, curb mis-use and track the transactions. Refund provisions made for Inverted Duty Structure is a welcome measure. Another noteworthy aspect of GST is provision to release the payment to supplier within 180 Days, otherwise tax liability will arise by way of reversal of credit taken. Though critics criticizing terming it as government intrusion into private agreements, it is right measure specially safeguarding interests of MSME suppliers.

Author Bio

Do you not think that the exporters working capital needs will be increased as he will be out of pocket for 20% advance payments of GST which will be refunded over 60+ days. This is not factored in his working capital bank limits. Even if banks grant these loans, there will be an added interest burden. Please advise.

Thanks for the article, bang on when you said that working capital required might decrease under GST. At our initial discussion with clients, we were under the impression that working capital needs will rise under GST, but having done a few impact analysis, the results have been quite the opposite.

Sir, Very informative article

kashok999@gmail.com

dear sir

is it GST applicable on advance payment recd from exporter.( agt export)

2. is it also applicable advance payment against goods supplied local against the letter of credit / FLC/ or any other mode of amount recd in advance from buyer.

Very well explained.. Thanks