One of the practiced business model in trade is that of ‘Bill-to-Ship-to’ model, which raises eyebrows in the Indirect tax world.

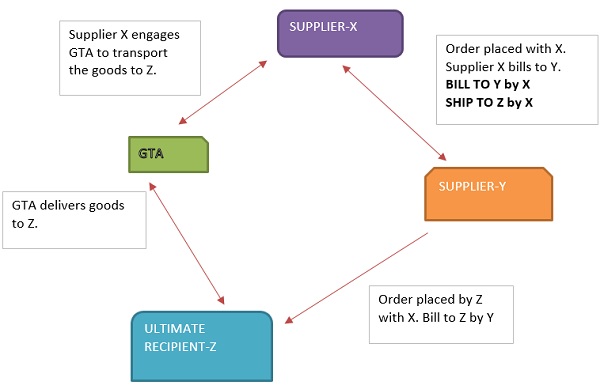

The bill-to ship-to transaction typically involves two supplies-

1. The supply between the one who supplies the goods and the one who pays for it and

2. The supply between the one who receives the goods and the one who paid the supply in the first leg.

In 2(93) of the CGST Act, 2017, the recipient of supply of goods is defined as the person who pays the consideration. In cases where there is no consideration, the recipient is the one to whom the goods are delivered.

In the above representation of Bill-to Ship-to transaction, there are two suppliers involved:

1. Supplier X-The main supplier, based on the purchase order of Y, supplies the goods.-SUPPLY 1.

2. Supplier Y-The second-level supplier, who makes an order with Y and also contracts to sell the goods to Z.-SUPPLY 2.

We shall assume that the consideration is paid by Y to X and by Z to Y for their respective inward supplies (for obtaining clarity over recipient of supply).

Hence the recipient for the supply of goods in Supply 1 is Y and Supply 2 is Z.

Now let us analyse the various facets of GST under “Bill to Ship to” concept:

Page Contents

1. Place of Supply:

Section 10 of the IGST Act deals with place of supply of goods other than imports and exports.

Section 10(1)(b) reads as follows:

The place of supply of goods, other than supply of goods imported into, or exported from India, shall be as under

where the goods are delivered by the supplier to a recipient or any other person on the direction of a third person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to the goods or otherwise, it shall be deemed that the said third person has received the goods and the place of supply of such goods shall be the principal place of business of such person;

Mere reading of the section would lead to confusion, when it comes to the interpretation of the word “recipient” and “third person”. The reader has to interpret the words without applying the definition of the word recipient as given in 2(93).

In other words, for the limited purpose of Sec.10 (1) (b):

Recipient would mean the person who receives the goods (Z in our example) and

Third person would mean the one who instructs delivery ;( In our example, it will be Y who instructs delivery to X and the one who pays consideration to X);

The PoS will be the location of the principal place of business of the “third person”-Y.

Hence even if the movement involves two different states, it is very well possible to have an Intra-state supply. On the contrary, even if the movement is within a state, it is possible to have an inter-state supply.

As far as Supply-2 is concerned, the provisions of Section 10(1)(a) would apply and not 10(1)(b).

Sec. 10(1)(a) states as follows:

The place of supply of goods, other than supply of goods imported into, or exported from India, shall be as under, ––

(a) where the supply involves movement of goods, whether by the supplier or the recipient or by any other person, the place of supply of such goods shall be the location of the goods at the time at which the movement of goods terminates for delivery to the recipient

Hence the PoS for the second supply between Y and Z will be based on the location where the movement terminates. With specific reference with our example, for Supply-2, the place of supply will be the principal place of business of Z.

Let us understand this by an example:

Place of Supply for “Supply-1”

| Scenario | Location of Supplier – X | Place of delivery of goods – Office of Z | Principal place of business of Y who instructed delivery to Z | Place of supply

for X |

Type of tax payable by X |

| 1 | Nashik | Nashik | Chennai | Chennai | IGST at Maharashtra |

| 2 | Nashik | Chennai | Chennai | Chennai | IGST at Maharashtra |

| 3 | Nashik | Kolkata | Bhbuaneshwar | Bhubaneshwar | IGST at Maharashtra |

| 4 | Nashik | Chennai | Nashik | Nashik | CGST + Gujarat GST at Maharashtra |

Place of Supply for “Supply-2”

| Scenario | Location of Supplier – X | Place of delivery of goods – Office of Z | Principal place of business of Y who instructed delivery to Z | Place of supply

for Y |

Type of tax payable by Y |

| 1 | Nashik | Nashik | Chennai | Nashik | IGST at Tamil Nadu |

| 2 | Nashik | Chennai | Chennai | Chennai | CGST+SGST at Tamil Nadu |

| 3 | Nashik | Kolkata | Bhbuaneshwar | Kolkata | IGST at West Bengal |

| 4 | Nashik | Chennai | Nashik | Chennai | IGST at Maharashtra |

2. Imports/exports in Bill-to ship-to supplies:

Two important sections determine the taxability of Bill-to ship-to transactions in case of exports/imports.

Sec.11 determines the place of supply in case of goods for imports and exports. In case of import of goods, the place of supply shall be the location of the importer. In case of exportation of goods, the place of supply shall be the place where the goods are exported to.

Sec.16 deals with zero-rated supplies of goods or services-which means export of goods or services or supply of goods or services to SEZ/SEZ developer.

As stated bluntly in the section, it is the ultimate place where the goods reach-either the importer in India/recipient outside India, which would determine the taxation impact.

Further, it is important to discriminate between “Export/zero-rated supply” and “supply by way of export”. Export/zero-rated supply would involve taking the goods from India to a place outside India.

Assuming that goods are shipped to a destination outside India, with X and Y being in India, the second leg of transaction, i.e. Supply-2 shall constitute “Export/Zero-rated supply”. However, claiming zero-rated supply for Supply-1 shall be incorrect merely because Supply-2 is zero-rated. For Supply-1 to be zero-rated, the “bill-to” destination shall also remain outside India, and then this would qualify as “supply by way of export”, and X can call his supply as “zero-rated supply by effecting supplies by way of export outside India”

Let us look at different scenarios to understand the nuances.

Place of Supply in “Supply-1”

| Scenario | Location of Supplier – X | Place of delivery of goods – Place of Z | Principal place of business of Y who instructed delivery to Z | Place of supply

for X |

Type of tax payable |

| 1 | Nashik | Sydney | Sydney | Sydney | Zero-rated supply as it would satisfy the condition-“supply by way of export”. |

| 2 | Nashik | Chennai | Sydney | Sydney(Operation of 10(1)(b) as Sec.11 will not apply since goods have not left India) | IGST at Maharashtra-Application of Sec.7(5) |

| 3 | Nashik | Sydney | Chennai | Tamil Nadu | IGST at Maharashtra |

| 4 | Nashik | Sydney | Colombo | Sydney | Zero-rated supply as it would satisfy the condition-“supply by way of export”. |

Place of Supply in “Supply-2”

| Scenario | Location of Supplier – X | Place of delivery of goods – Place of Z | Principal place of business of Y who instructed delivery to Z | Place of supply

for Y |

Type of tax payable |

| 1 | Nashik | Sydney | Sydney | Sydney | Y will not be liable to any tax in India. |

| 2 | Nashik | Chennai | Sydney | Y will not be liable to any tax in India. | Y will not be liable to any tax in India. |

| 3 | Nashik | Sydney | Chennai | Tamil Nadu | Zero-rated supply |

| 4 | Nashik | Sydney | Colombo | Y will not be liable to any tax in India. | Y will not be liable to any tax in India. |

3. Input-tax credit

Section 16 of the CGST Act, lays down the conditions upon satisfaction, the ITC would be eligible to be taken. Amongst other conditions, receipt of the goods or services is one of the conditions for taking Input Tax credit.

To address the issue of Bill-to-ship to transactions, an explanation has been provided in Sec.16(2)(b) which reads as under:

For the purposes of this clause, it shall be deemed that the registered person has received the goods where the goods are delivered by the supplier to a recipient or any other person on the direction of such registered person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to goods or otherwise.

This would mean that in case of “Supply-1” type of transactions, Y would be eligible to take credit of the invoice raised by X, even-though the goods have not been “physically” delivered to Y. A deeming fiction has been imposed on such scenarios.

As far as Z is concerned, he will be eligible to take ITC of the invoice raised by Y, only if the goods have been received by him physically.

4. Supply when there is no consideration:

The underlying principle of any contract is consideration and when there is no consideration, there cannot be a supply and when there is no supply, it is out of the ambit of GST.

Hence, it is possible that either Supply-1 or Supply-2 can be without consideration.

If Supply-1 is without consideration, and neither X, nor Y are related to each other, supply-1 shall not even be regarded as supply if neither Z nor Y pays for the goods. This is irrespective of the fact that the recipient in case of Supply-1 is Z(being the receiver of the goods). If Z pays for the goods, the transaction would be between X and Z and this would lead to a third supply between Z and X.

However, if Y pays for the goods to X, but in turn does not receive any payment from Z, Supply-2 will not be regarded as supply as such with the same assumption that none of them are related.

Further, the above two scenarios would doubt the commercial substance of such transactions.

More practically, coming to a case where either X&Y are related persons or Y and Z are related persons, one would have to refer to Para 2 of Schedule I of the CGST Act, where supplies between related persons made in the course or furtherance of business shall be regarded as “Supply” even when consideration is absent

Accordingly, valuation rules would have to be applied as specified in Section 15 and Rule28/30/31 of the Valuation rules. However, there won’t be any change in place of supply interpretation.

One example of this kind would be placement of order by Head Office(Y) with X to deliver the goods to branch office (Z). X will bill the Head Office and send the goods to branch office. The transaction between branch and head office shall be valued in accordance with Valuation rules-28,30 or 31 of the CGST Rules,2017.

5. Requirement of E-way bill:

E-way bill requires along with the consignment note-either a bill of supply/tax invoice/delivery challan to move the goods.

The contract of the GTA is with X, being the supplier of “Supply 1”. The e-way bill in case of Bill to ship to transaction can be generated by “X” or “Y”. In other words, “Z” being the recipient cannot generate the way bill.

Further, one e-way bill is sufficient in cases of bill-to ship-to mode. There is no requirement to generate a second e-way bill between “Z” & “Y”

We have delivered goods to Indian party in SEZ as per order from overseas party. Billing is in the name of overseas party and ship to is Indian party. Since goods are shipped to SEZ, we have not paid any GST amount.

Now we want to receive payment from overseas customer but bank is not allowing us to receive payment.

What is way out? How to get this payment? Has anyone faced this problem? How to resolve it?

Pls help.

Sir what to be done in case of Processing or job work.Here goods will be ordered by A TO B and informed that such goods shoul be sent directly to C in same state or other State But details of Final recepient not known.Here common practice is they will keep goods in transport office and once Job work party is confirmed they will issue detailos of Third party or processer.But while movement of goods SHIP TO address is left blank and only place is mentioned.

sir i have a question. i received a order from singapore. the lelling me to to generate way bill to address of mumbai and the billing address will be the singapore. who its possible and if its possible the guide me it could be done

Order placed by indian vendor with INR ,whereas asking to indicate ship to party on GST Inv as overseas ,can you update if its possible in GST

Order placed by indian vendor with INR ,whereas asking to indicate ship to party on GST Inv as overseas ,can you update if its possible in GST .

It is for kind attention of author of article “Treatment of ‘Bill To-Ship-To’ Transactions In GST” published in taxguru dt. sep.11,2019 the following para needs correction in my opinion- “2. Supplier Y-The second-level supplier, who makes an order with Y and also contracts to sell the goods to Z.-SUPPLY 2. IT should ‘who makes an order WITH X’ instead of ‘who makes an order WITH Y’.

thanks

Thank you sir for your guidance. Sir I have a query. In my case Mr. A of Delhi received order from Mr. Y of Hong Kong to deliver goods at liaison office (unregistered) of Mr. Y in Delhi. From liaison office the goods are exported to Hong Kong. Consideration is received in convertible foreign exchange. In this case, what will be the POS, whether it is an export of goods and if GST is payable then whether it will be IGST or CGST/SCGT.

We have received an order from Foreign company for supplying material. Order is in USD and payment shall be received by us in USD .The material however shall be shipped in India to the project site of Foreign buyer and later it shall be taken out of India by the foreign buyer. How to treat this under GST/FEMA point of view. Can we raise invoice in USD with different billing and shipping address. Will it be treated as export from GST/FEMA point of view.

We have received order for supply of material from US based company in USD. However the goods shall be delivered in India for testing purpose by client of US based supplier and post testing the material shall be taken by US based company out of India. Here , the billing company is US based but shipping is in India on instruction of US based customer. Can we invoice on US based company in USD when the shipping is in India only. US based customer has agreed to pay in USD . Will this be treated as export ?. pls advise how to regularise this taxation/FEMA point of view.