The Biggest Indirect Tax Reform of India is about to take place on 1st July, 2017. A Summarized Format of Significant Differences under M-VAT Provisions & GST has been given below :-

| Sr.No. | Particulars | Provision under GST Regime | Provision under M-VAT Regime |

| 1 | Applicability | GST will be made Applicable on Manufacturers, Traders and Service Providers | M-VAT was liable to be paid by Traders (Buyers & Sellers of Taxable Goods) only. |

| 2 | Taxability of Intra-State and Inter-State Transactions | Refer Annexure-I | Refer Annexure-I |

| 3 | Credit of Capital Goods | Will be Fully Available except for following few items:

1. Motor Vehicles 2. Goods/Service for Personal Consumption 3. ITC For Exempted Supplies 4. Goods Lost/Stolen or distributed as free samples |

Available full for Certain Items and for Certain Items 3% was retained |

| 4 | Credit of Taxes paid on Services | Credit of CGST/SGST/IGST Paid on Services Received will be made Available | Credit of Service Tax Paid on Services Received was not admissible and therefore it was a cost for Traders |

| 5 | Taxability of Stock Transfers to Inter-State Branches | Taxable since different Registration for each state will be there but full ITC will be made Available to Transferee branch | Was not liable for CST and F Form was supposed to be submitted by Transferee which was later to be submitted in Department by Transferor |

| 6 | Returns & Payment Dates |

Periodicity: Monthly GSTR-1 – Details of outward supplies of taxable goods (10th of Subsequent Month) GSTR-2 – Details of inward supplies of taxable goods and/or services claiming input tax credit (15th of the subsequent month) GSTR-3 – Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the Payment of Tax (20th of the next month) GSTR-9 – Annual Return (31st December of next financial year) |

Periodicity: Quarterly Form 231/232/233/III-E: Quarterly VAT/CST Return along with Payment of Tax (21st of Month Succeeding Quarter) |

| 7 | Audit | Applicable: Dealers crossing Turnover of Rs. 1 crore

Due Date: 31st December of next Financial Year |

Applicable: Dealers crossing Turnover of Rs. 1 crore

Due Date: 15th January of next Financial Year |

| 8 | Conditions for Claiming Input Tax Credit | The two major shifts of claiming Input Tax Credit are:

1. Payment to Supplier must be made within 180 days 2. Every single Purchase Invoice must be matched with Invoice of Supplier while uploading return for the month and Supplier must make payment of Tax |

No such conditions were existed under M-VAT initially at time of Return Filing.

However, filing of Annexures J1 & J2 was to be made and mismatch in J1 & J2 in subsequent yearsled to payment of Credit Amount. |

| 9 | Payment of Tax Under RCM for Purchases from Unregistered Suppliers |

For Every Purchases made or Services received from Unregistered Suppliers for an amount exceeding Rs. 5,000 per day, GST has to be paid by Registered Recipient under Reverse Charge Mechanism and a Payment voucher should be issued to such supplier. |

No Such Provisions were present under M-VAT |

| 10 | Point of Taxation | GST will be charged at the Time of Raising Invoice or at the Time of Receiving Money from Recipient whichever is earlier (Advances from Customers will be liable for GST) | VAT has to be charged at the time of Raising Invoice |

| 11 | Threshold Limit for Non – Registration | Rs. 20 Lakhs | Rs. 10 Lakhs |

| 12 | Penalty for Late Filing of Returns | Rs. 100 for per day of Late Filing (Maximum Penalty – Rs. 5,000)

Penalty @ 0.25% of Annual Turnover will be levied for Late Filing of Annual Return |

Varied from Rs. 1,000 to Rs. 5,000 |

| 13 | Interest on Late Payment of Tax | 18% p.a. Interest on day wise basis will be levied | Interest @ 1.25% for 30 days of delay, Interest @ 1.5% for next 60 days of delay, Interest @ 2% for further delay was charged |

| 14 | Treatment of Discount | Discount initially reflected in invoice will not be subject to GST. Discounts allowed subsequently will also not amount to GST subject to the conditions for giving discount were pre-defined among Supplier & Recipient and a Credit is needed to be issued in this regard. | Similar Provisions existed under VAT Regime except that there was no condition for Pre-Defining Discount Terms |

| 15 | Invoicing Requirements | Few Important things which are must required to be mentioned in invoice are:

> Name, Address, GST TIN of Supplier > Name, address, GST TIN of Recipient (If recipient is registered Person under GST) > Product Details such as HSN Code, Rate of GST applicable on it, Quantity Sold, Rate and Amount > CGST/SGST/IGST must be reflected separately |

Similar things were required to be presented under VAT except for mentioning of HSN Code and Quantity of Goods Sold |

| 16 | Time Limit for Retention of Books of Accounts & Records | 60 Months (5 Years) from end of September of Next Financial Year i.e. 5 Years 6 Months from end of Financial Year | 5 Years from end of Financial Year |

| 17 | GST Compliance Rating | A Rating System will prevail under GST. Every Registered Dealer will be rewarded Rating by Department based on Compliance of GST Provisions.

Please Note that such Rating of every dealer will be made reflected on GST Portal. So, it is advisable to maintain your rating good to avoid loss of Business Reputation |

No such provisions were existed previously |

| 18 | Mandatory Receipt of Goods for Claiming Input Tax Credit | Input Tax Credit will be made available after Receipt of both Invoice and Goods | Only Receipt of Invoice was sufficient to Claim Input Tax Credit |

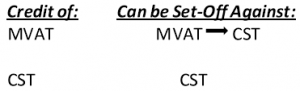

| 19 | Set-Off of Taxes |

Note: CGST & SGST Cannot be Set-Off |

|

| 20 | Treatment of Sales Return | Reversal of Tax on Goods Returned by Recipient will be allowed provided goods are received within 30th September of Subsequent Financial Year | Reversal of Tax on Goods Returned by Recipient was allowed provided goods were received within 6 months from Sale Date |

| 21 | Mode of Payment for Interest & Penalties | Interest and Penalty levied must be paid in Cash or through Banking means only i.e. it cannot be Set-Off against Input Credit Available | Earlier, dealers were able to Set-Off Interest and Penalty through balances in M-VAT & CST available also |

| 22 | Issue of Debit / Credit Notes | Revision of Sales & Purchases Details Uploaded is not possible under GST, so Dealers need to Issue Debit & Credit Notes in order to rectify there Uploaded Data | Revised Returns could have been uploaded before / after audit |

Other Important Aspects to be Taken Care of before Implementation of GST:

> Gear up to Issue Invoices with Important Details and Charge GST from 1st July, 2017 itself

> Get Ready with your Closing Stock Working as on 30th June, 2017 and Match it with Purchase your Invoices

> Claim of Excise will be made available @ 100% on closing stock where Excise paid is reflected in Invoice.

If Excise paid is not Reflected then 60%(where GST Rate is >= 18%) or 40% (Where GST Rate < 18%)

> Inform your GST Provisional ID & ARN to all Your Suppliers and also Collect it from your Customers

> Determine HSN Codes of Products you are dealing in and Tax Rate Applicable on it

> The Payment of GST can be made through RTGS/NEFT/Debit Card/Credit Card/Cash (Amount < Rs. 10,000)

Ann exure-I

Example 1: Supplier A of Maharashtra sold Goods to Buyer B of Maharashtra worth Rs. 100 (Applicable Tax Rate on Goods was 18%)

| Treatment in GST Regime | Treatment under VAT Regime | ||

| Sales | 100 | Sales | 100 |

| Add: CGST @ 9% | 9 | Add: VAT @ 18% | 18 |

| Add: SGST @ 9% | 9 | Total Invoice Value | 118 |

| Total Invoice Value | 118 | ||

In both cases the Buyer of Goods B will get set off of Rs. 18 Therefore, Cost of Purchase for B of Maharashtra will be Rs. 100

Example 2: Supplier A of Maharashtra sold Goods to Buyer B of Gujarat worth Rs. 100 (Applicable Tax Rate on Goods was 18%)

| Treatment in GST Regime | Treatment under VAT Regime | ||

| Scenario 1: If C-Form is Produced | |||

| Sales | 100 | Sales | 100 |

| Add: IGST @ 18% | 18 | Add: CST @ 2% | 2 |

| Total Invoice Value | 118 | Total Invoice Value | 102 |

| This is a Major Shift in GST Regime whereby B of Gujarat will get Set-Off of Rs. 18 IGST Paid and therefore the Cost of Manufacturing for him will be Rs. 100 only | |||

| Scenario 2: If C-Form is not Produced | |||

| Sales | 100 | ||

| Add: VAT @ 18% | 18 | ||

| Total Invoice Value | 118 | ||

| In both of the above scenarios under VAT Regime, B of Gujarat won’t get Set-Off of Rs.2/Rs.18 (as the case may be). Therefore Cost of Manufacturing for B of Gujarat will be Rs. 102/Rs. 118 (as the case may be) | |||

Note:

1. This article is not published for Commercial Purpose and is freely available over the Internet.

2. The above Information Provided is summarized and contains only Relevant Data for Traders of For Complete understanding of Law, other Books and Act may be referred

3. Substantial amount of Time and Efforts are devoted by Publisher in compiling this document and to avoid errors and omissions. In spite of that, errors may creep in. Any errors or omissions noted can be brought to notice of publisher at lsfedudocs@gmail.com. Any Feedback or Queries can also be sent on same E-Mail ID.

Author Bio

Very Article and very informative