“Explore the intricacies of tax audit and the interlink between sections 44AB, 44AD, and 44ADA of the Income Tax Act for the Assessment Year 2023-24. Understand the applicability conditions, thresholds, and amendments that impact businesses and professionals. A comprehensive flowchart is provided to help assess the necessity of a tax audit. Stay informed for informed financial decisions.”

Applicability of Tax Audit and Inter link between section 44AB vis-à-vis

section 44AD and 44ADA of the Income Tax Act

[Relevant for A.Y. 2023-24]

Over time, numerous amendments have been made regarding the applicability of Tax Audit provisions and the widely recognized deeming income provisions, namely Section 44AD and Section 44ADA of the Income Tax Act. This has resulted in significant confusion, and unfortunately, a crucial amendment effective from Assessment Year (A.Y.) 2017-18 has gone unnoticed by a majority of taxpayers and professionals.

The purpose of this article is to draw attention to this amendment and elucidate the provisions of Sections 44AB, 44AD, and 44ADA as applicable for A.Y. 2023-24.

Additionally, a flow chart is provided at the end of the article to assist readers in determining the final outcome regarding the applicability of audit.

APPLICABILITY OF TAX AUDIT

Sec 44AB – Audit of accounts of certain persons carrying on business or profession.

|

Clause |

Nature of Activity | Condition | Threshold | |

| (a) | Business | Total Sales, Turnover or Gross Receipts | Exceeds ₹1 crore | |

| Exception |

Cash Receipts in business ≤ 5% of total amount received And Cash Payments in business ≤ 5% of total amount paid |

Exceeds ₹10 crores | ||

| The threshold limit for applicability of Tax Audit is ₹1 crore. However, relaxations are provided to assessees who primarily conduct their business transactions through banking channels. If an assessee’s

i) cash receipts are lower than 5% of the total receipts and ii) cash payments are lower than 5% of the total payments, he will be liable for audit only if his sales, turnover, or gross receipts exceed ₹10 crores |

||||

| (b) | Profession | Gross Receipts | Exceeds ₹50 lakhs | |

| (c) | Business | Section 44AE, 44BB and 44BBB and wants to Declare profits Lower than Deemed profits as provided in respective sections | ||

| (d) | Profession | Is engaged in the specified professions as prescribed under Sec 44AA(1)* and wants to Declare income lower than deemed income u/s 44ADA | ||

| (e) | Business | If Sec 44AD(4) is applicable to the assessee Discussed in detail later |

||

* legal, medical, engineering or architectural profession or the profession of accountancy or technical consultancy or interior decoration or any other profession as is notified by the Board

Exception to Sec 44AB:

Turnover is upto ₹2.00 Crores AND Assessee declares Profits as per Sec 44AD(1)

Meaning: Assuming the cash transactions > 5% and the Turnover exceeds ₹1 Crore as specified in clause (a) above, the assessee can still be not liable to get his books of accounts audited by declaring income u/s 44AD(1) s.t. his Turnover is upto ₹2 Crores only.

POPULAR DEEMING PROVISIONS UNDER INCOME TAX ACT AND THEIR INTER-LINK WITH SECTION 44AB

Sec 44AD: Special provision for computing profits and gains of BUSINESS on presumptive basis

This section overrides all the PGBP provisions as stated under Sec 28 to 43C. It states that, in case of an eligible assessee engaged in an eligible business, a sum of 8% of the total turnover or gross receipts shall be deemed profits under the head “PGBP”

If receipts are through specified electronic modes (i.e. through banking channels), deemed profits are 6%.

The assessee may voluntarily declare profits at a higher percentage than specified above.

The BIGGEST benefit in case of a person engaged in a business and opting for the presumptive taxation scheme of section 44AD is that the provisions of section 44AA relating to maintenance of books of account will not apply. In other words, if a person adopts the provisions of section 44AD and declares income @ 8%/6% of the turnover, then he is not required to maintain the books of account as provided under section 44AA in respect of business covered under the presumptive taxation scheme of section 44AD.

WHO CANNOT OPT FOR SECTION 44AD?

1. A person carrying on profession as referred to in section 44AA(1)*

2. a person earning income in the nature of commission or brokerage

3. a person carrying on any agency business

| Eligible assessee:

Individual, HUF or a Partnership Firm (excl. LLP) |

Eligible business: Any business except the business of plying, hiring or leasing goods carriages referred to in Section 44AE and Whose Turnover or Gross Receipts does not exceed ₹2 Crores. |

44AD(4) – The Drastic Amendment in Section 44AD introduced w.e.f. A.Y. 2017-18

Before this amendment i.e. upto A.Y. 2016-17, in case of an eligible assessee engaged in eligible business, it was mandatory to declare profits at a specified % as stated above. If the Taxpayer wants to declare his income lower than the specified % and his income exceeds Basic Exemption Limit, he was mandatorily required to:

a) Maintain the books of accounts as per Section 44AA and

b) Get his Books of accounts Audited irrespective of his turnover

However, the provisions u/s 44AD were drastically amended w.e.f. A.Y. 2017-18.

The relevant clauses of old provisions of Section 44AD and Amended provisions of Section 44AD linked with relevant provisions of Sec 44AB are stated as under:

|

Pre – amendment |

Post – amendment | ||

| 44AD(5) | Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee who claims that his profits and gains from the eligible business are lower than the profits and gains specified in sub-section (1) and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB | 44AD(4) | Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1), he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which the profit has not been declared in accordance with the provisions of sub-section (1). |

| 44AD(5) | Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee to whom the provisions of sub-section (4) are applicable and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB | ||

| Corresponding relevant provisions of Sec 44AB (Pre and Post Amendment) | |||

| 44AB(d) | carrying on the [business] shall, if the profits and gains from the [business] are deemed to be the profits and gains of such person under [section 44AD] and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his [business] and his income exceeds the maximum amount which is not chargeable to income-tax in any [previous year,] | 44AB(e) | carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year, |

(the provisions of mandatory maintenance of books of accounts and audit are applicable if the income exceeds Basic Exemption Limit. For the sake of brevity, we hereby always presume that income exceeds Basic Exemption Limit)

Thus, upto AY 16-17, it was mandatory for assessee to declare profits @ specified % or get the Books of Accounts Audited

W.e.f. AY 17-18,

44AD(4) – Where an eligible assessee declares profit for any previous year at the rate of 8% / 6% of the turnover u/s 44AD and he declares profit for any of the 5 consecutive assessment years at lower than 8% / 6%, the following consequences shall apply:

- He shall not be eligible to claim the benefit of Sec 44AD for 5 subsequent assessment years (i.e. subsequent to AY in which profits are not declared in accordance with Sec 44AD); and

- He will have to maintain and get his books of accounts audited u/s 44AB (irrespective of his Turnover)

Example of amended provisions:

Mr. Ram (an eligible assessee), has declared profits @ 8%/6% on presumptive basis u/s 44AD(1) for A.Y. 2018-19 [..the 1st year of 44AD]. Now he has to declare profits on presumptive basis for 5 consecutive subsequent years also i.e. [AY 19-20 to AY 23-24].

For the A.Y. 2019-20 and A.Y. 2020-21, he offered income @ 8%/6% on presumptive basis. For A.Y. 2021-22, he does not declare profits on presumptive basis and declares income at let’s say 3% only.

Accordingly, Mr. Ram has not offered profits on presumptive basis for 5 consecutive assessment years after A.Y. 2018-19 and therefore following consequences shall apply for AY 2021-22 and for subsequent 5 AY i.e. for AY 2021-22 to AY 2026-27, irrespective of his TURNOVER

(i) He will have to maintain Books of Accounts u/s 44AA

(ii) Get the Books of Accounts Audited u/s 44AB

Thus, unlike earlier i.e. (upto AY 16-17), the assessee is need not required to declare profits @ specified % or get it audited. The assessee can maintain books and declare lower profits without getting them audited.

However, ONCE PROFITS ARE DECLARED AT SPECIFIED % U/S 44AD(1), THEN IT SHALL BE FOLLOWED FOR SUBSEQUENT 5 YEARS ALSO.

Sec 44ADA: Special provision for computing profits and gains of PROFESSION on presumptive basis

This section overrides all the PGBP provisions as stated under Sec 28 to 43C. It states that, in case of an Individual or Partnership Firm (other than LLP) engaged in a specified profession as referred to in Sec 44AA(1)*, and whose Gross Receipts do not exceed Fifty Lakh rupees, a sum of 50% of the gross receipts shall be deemed profits under the head “PGBP”

The assessee may voluntarily declare profits at a higher percentage than specified above.

Similar to businesses covered u/s 44AD, the specified professionals opting for taxation u/s 44ADA, need to require to maintain Books of Accounts as per Sec 44AA

Inter-link of Sec 44ADA and 44AB

| Sec 44ADA(4) | Sec 44AB(d) |

|

(4) Notwithstanding anything contained in the foregoing provisions of this section, an assessee who claims that his profits and gains from the profession are lower than the profits and gains specified in sub-section (1) and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (1) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB. |

(d) carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits and gains of such person under section 44ADA and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his profession and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year; |

The provisions for Specified Professionals (44ADA) are different from the provisions of eligible businesses as per Section 44AD (they are similar to old provisions of 44AD)

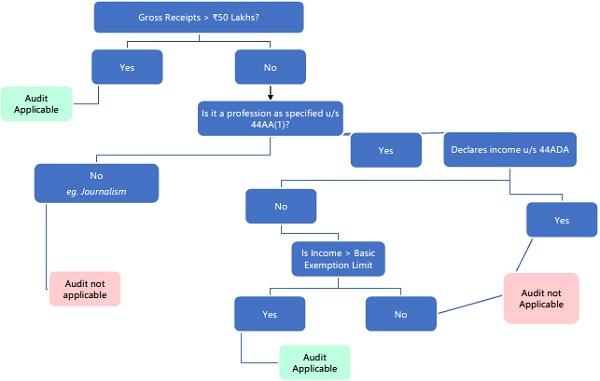

The specified professionals, if their Gross Receipts in an AY does not exceed ₹50 Lakhs, are mandatorily required to declare profits @ minimum of 50% as specified u/s 44ADA. In case, they wish to declare lower profits, they shall maintain Books of Accounts u/s 44AA and get them audited u/s 44AB.

*legal, medical, engineering or architectural profession or the profession of accountancy or technical consultancy or interior decoration or any other profession as is notified by the Board

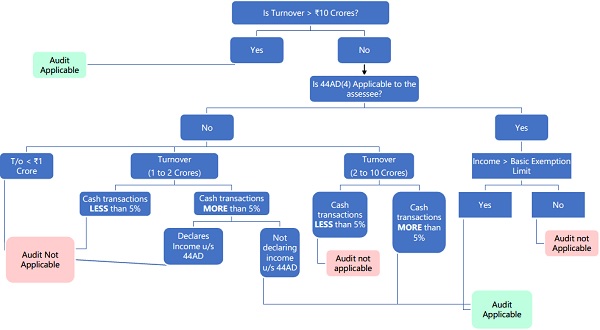

FLOW CHART REGARDING APPLICABILITY OF TAX AUDIT IN CASE OF BUSINESS

A.Y. 2023-24

–

Disclaimer: The author has made a sincere effort to provide thorough explanation of the subject matter and the drafting has been made based on own research and understanding. However, there is always a possibility for disagreement with the aforesaid interpretation of laws by Tax Authorities and Courts. While the author has taken care to present the provisions in a concise and visually accessible manner through flow charts, the risk of inadvertent errors creeping in cannot be ruled out. Readers are advised to cross-verify the legal provisions mentioned herein with the latest applicable laws, regulations, and official sources and to exercise their own judgment and due diligence when relying on the information provided. The author cannot be held personally liable for any consequences arising from the use or interpretation of the information provided in this article.

Disclaimer: The author has made a sincere effort to provide thorough explanation of the subject matter and the drafting has been made based on own research and understanding. However, there is always a possibility for disagreement with the aforesaid interpretation of laws by Tax Authorities and Courts. While the author has taken care to present the provisions in a concise and visually accessible manner through flow charts, the risk of inadvertent errors creeping in cannot be ruled out. Readers are advised to cross-verify the legal provisions mentioned herein with the latest applicable laws, regulations, and official sources and to exercise their own judgment and due diligence when relying on the information provided. The author cannot be held personally liable for any consequences arising from the use or interpretation of the information provided in this article.

Author Bio

Lakhan Sir, excellent and well researched writeup, Salute to you!

One scenario : Assessee has been declaring his income under 44AD i.e.@ > 8%, then in AY 22-23 his t/o exceeded the audit limit, so he had to file the ITR likewise, and here showed loss. now in AY 2324 his t/o is again below the audit limit, does he really need to get his books audited u/s. 44AB even if he will declare profit > 8% u/s 44AD?

Lakhan ji, excellent writeup, very well researched, kudos to you !

One scenario : assessee has been declaring his income under 44AD i.e.@ > 8%, then in AY 22-23 his t/o exceeded the audit limit, so he had to file the ITR likewise, and here too the profit was > 8%. now in AY 2324 his t/o is again below the audit limit, does he really need to get his books audited u/s. 44AB even if he will declare profit > 8% u/s 44AD?

He is eligible for Sec 44AD because during AY 22-23 he did not voluntarily opt out of Sec 44AD, he became ineligible due to turnover limitation. In AY 23-24, audit won’t be applicable to him if he is declaring income > 8% u/s 44AD.

One of the best write up read in Taxguru. Excellent clarity.