CA Bharat Mathur

RATIONALE FOR INTRODUCING GST

- The Goods & Service Tax is a comprehensive value added tax on the supply of goods and services.

- Destination based consumption tax.

- Aims to provide cost competitiveness to the indigenous goods / services in the international markets.

- Encourages foreign investment in India by providing for a simplified and easy to comply tax structure.

- Easier tax administration because of the inherent transparent character.

BENEFITS SOUGHT

- To simplify the current Indirect tax structure

- To avoid the cascading effects of taxation by providing for a single tax base

- To reduce the production costs for the industries and in turn check the inflation levels

- To provide for an easy and effective Input tax Credit mechanism

DUAL GST STRUCTURE

- The GST regime shall provide for a simultaneous levy by the Centre and the States on a common tax base.

- The intra state supply of goods & services shall be subject to Central GST (CGST) and State GST (SGST).

- The imports and inter state supply of goods & services shall be subject to Integrated GST (IGST).

TAXABLE EVENTS

> EXCISE: – Manufacturing or production of goods

> SERVICE TAX: – Provision of services

> VAT / CST: – Sale or supply of goods

> GST: – Supply of goods / services

SUPPLY

| 1. Sale

2. Transfer 3. Barter 4. Exchange 5. License 6. Rental 7. Lease 8. Disposal |

Importation of service | 1. Permanent transfer / disposal of business assets where ITC has been availed

2. Supply between related persons / distinct persons 3. Supplies to / by an agent to the principal 4. Gifts / free samples |

1.Transfer of the title in goods or rights thereof

2. Any treatment or process applied to another person’s goods 3.Declared services which are currently a part of the service tax regime (construction, works contract, IPR, renting of IP) |

| for a consideration and in the course or furtherance of business | Whether or not for a consideration & whether or not in the course or furtherance of business | Without consideration in the course or furtherance of business | Schedule II of the CGST Act |

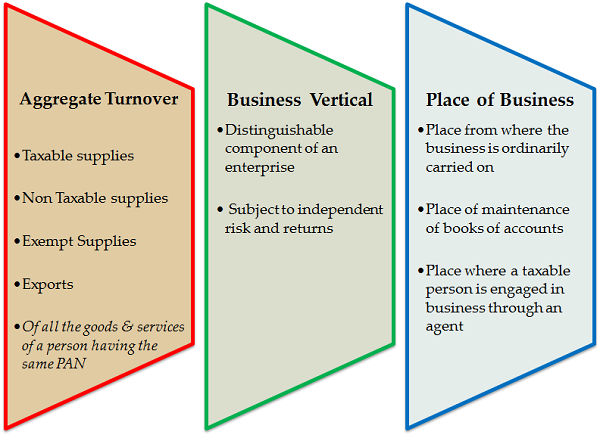

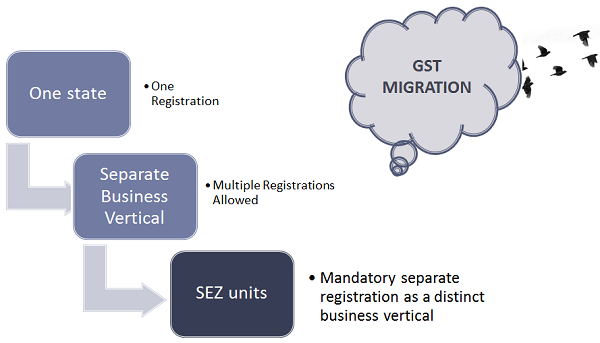

REGISTRATION CRITERIA

MANDATORY REGISTRATION

GST – SEZ Orientation

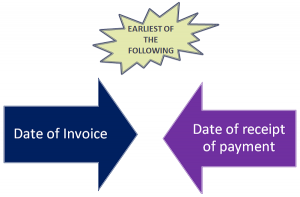

TIME OF SUPPLY (GOODS & SERVICES)

TIME OF SUPPLY

Reverse Charge Basis

- The date of receipt of goods

- The date on which payment is made

- The date after 30 days / 60 days from the date of issuance of goods / service invoice

Residual Provisions

- The date on which the periodical return has to be filed

- In any other case, the date on which CGST/ SGST is paid

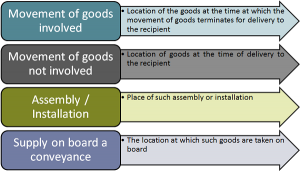

PLACE OF SUPPLY OF GOODS

PLACE OF SUPPLY OF SERVICES

Supply to a registered person – location of the recipient

Supply to any other person – location of the recipient where the address on record exists; else the location of the supplier

| Relation to Immovable Property | Location of the immovable property |

| Restaurant & Catering services and services which require the physical presence of the receiver |

Location where the services are actually performed |

| Admission to an entertainment / amusement event and ancillary services | Location where the event is actually held |

|

|

| Goods Transportation Services |

|

| Passenger Transportation Services |

|

| Services on board a conveyance |

|

| Telecommunication |

|

| Banking and other financial services |

|

| Insurance services |

|

| Advertisement services to government or statutory bodies or local authority |

|

Composite & Continuous Supply – Taxability

COMPOSITE SUPPLY

- Supply of 2 or more goods / services, AND

- Natural bundling thereof

- Tax liability will be the tax on the principal supply

- If it is a mixed supply, the composite supply shall be treated as supply of that goods or services which attract highest rate of tax.

CONTINUOUS SUPPLY

- Recurrent supply

- Periodic invoicing / payments

- The time of supply for such continuous supply shall remain the earlier of the date of payment or date of issue of invoice.

VALUATION

GST VALUATION RULES

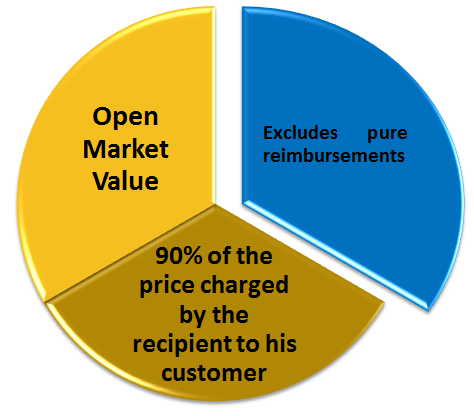

Where the recipient is eligible for full ITC, the invoice value shall be deemed to be the open market value of such goods or services.

GST VALUATION RULES

Principal – Agent Supplies

If the supply value cannot be determined in terms of the valuation rules, the value shall be 110% of cost of production / cost of provision of service

INVOICING MECHANISMS

|

Time Limit To Raise An Invoice |

|

| GOODS | SERVICES |

|

|

TAX PAYMENTS & REFUNDS

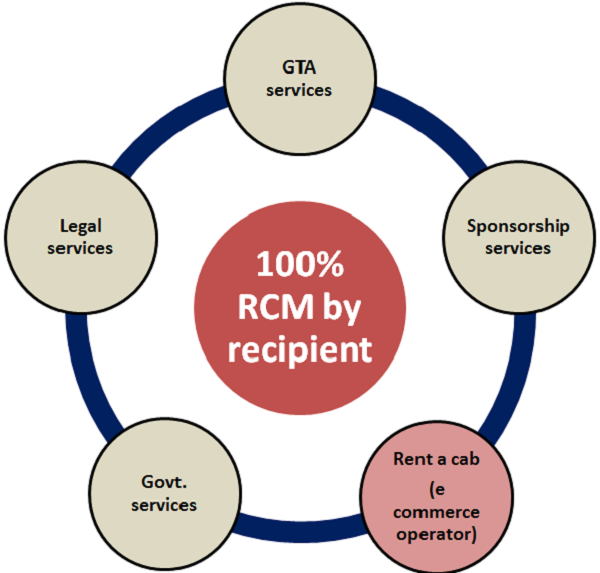

REVERSE CHARGE MECHANISM

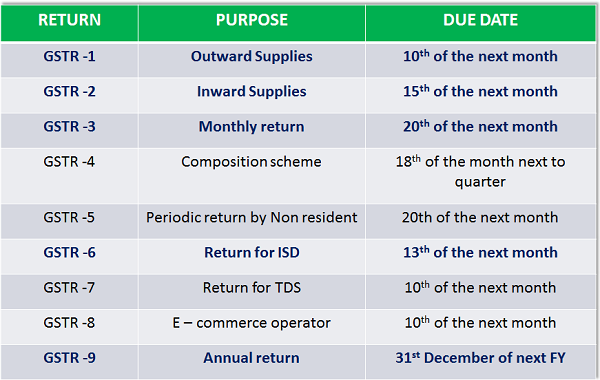

RETURNS

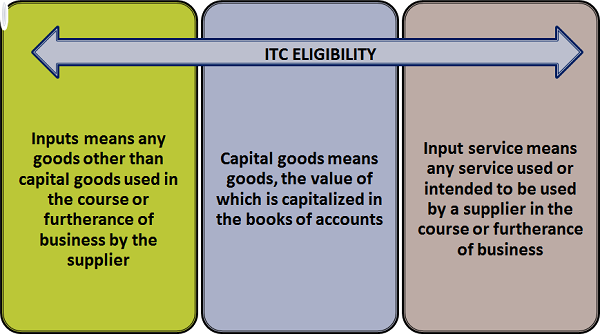

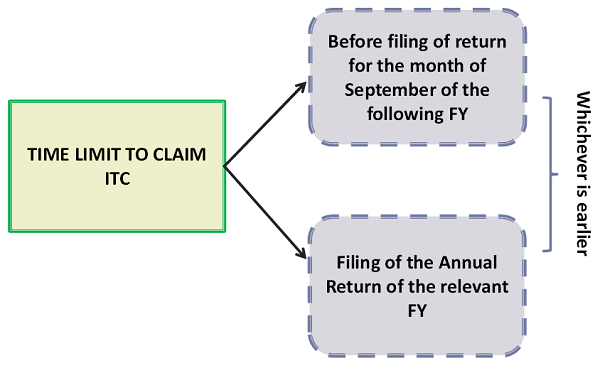

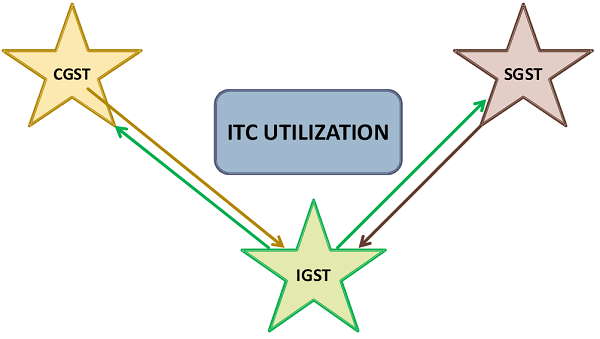

INPUT TAX CREDIT

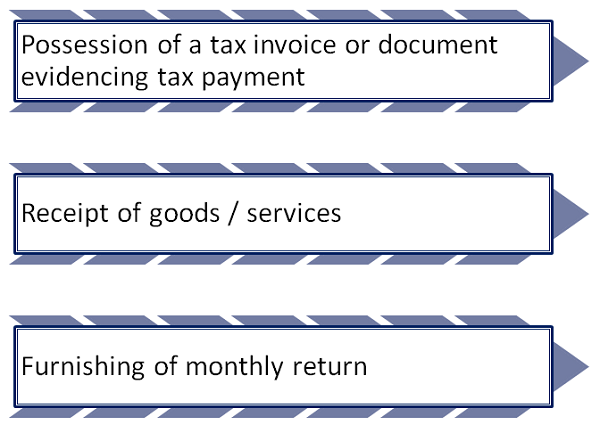

PRE – REQUISITES TO CLAIM INPUT TAX CREDIT

INPUT TAX CREDIT

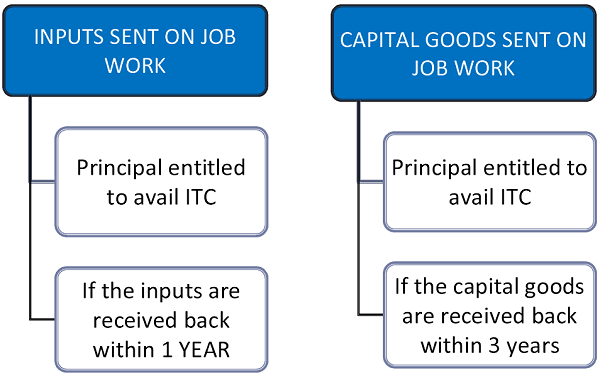

ITC IN RESPECT OF JOB WORK

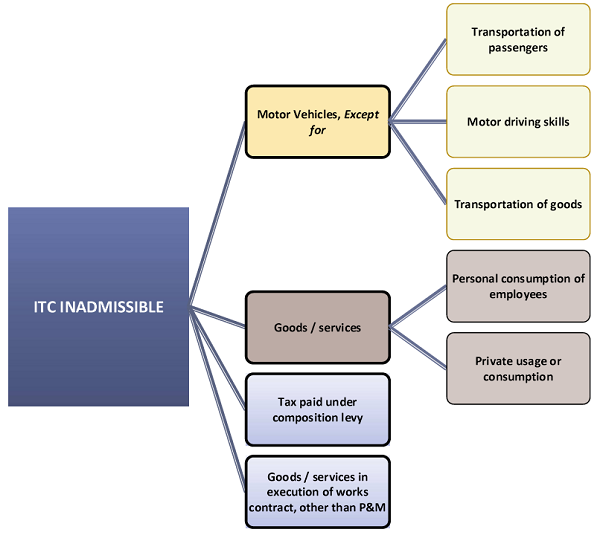

BLACKLISTING PROVISIONS

Factors affecting compliance rating score

- Regular payment of taxes

- Timely e-filing of returns

- Matching of transactions

- Transparent reconciliations

- Co-operations in assessments and audits

Triggers for Blacklisting

- Continuous default for 3 months in reversal of ITC

- Continuous default for 3 months in filing of returns

- Continuous short reporting of sales beyond prescribed margin for 6 months.

GEARING UP FOR GST…….

- Filing of previous refund claims before the appointed date

- Collection of Form C / H / F / I from the vendors

- Synchronization of HSN codes for goods and services

- Return of goods from the job worker within the prescribed time

- Accounting of stock / ITC details in the books / returns

- Re – configuration of accounting / invoicing systems

- Filing of Form Tran – 01 within 90 days from the appointed date to claim the carry forward of eligible ITC under the GST Act

- Details of stock held on the appointed date and the ITC availed thereof

- Change in the invoicing formats and documentation

- Ensuring monthly payments of GST for filing the returns

- Discharging the GST liability on the receipt of advances

- Ensuring due match of the monthly returns with the vendors to avoid legal recourse and financial obligations

TRANSITIONAL PROVISIONS

- The amount of CENVAT claimed in the last return filed under the earlier Laws shall be transferred to the e- Credit ledger after the appointed date.

- Unavailed credit on capital goods will be allowed after the appointed date.

- Credit of inputs held in stock / semi –finished / finished goods shall be admissible in the GST era in accordance with their admissibility

SWITCHING FROM / TO COMPOSITION SCHEME

- In case a taxable person who carries eligible ITC in a return (furnished under an earlier Law) switches over to Composition scheme under the GST regime, he shall be required to pay an amount equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in WIP or finished goods held in stock on the preceding date of switch over.

- A registered taxable person, paying tax under the Composition scheme under an earlier Law, shall be entitled to take credit of duties in respect of inputs held in stock and inputs contained in WIP or finished goods held in stock on the appointed date.

TRANSITIONAL PROVISIONS

- Every claim of refund / appeal / review / revision / CENVAT credit filed before the appointed day, shall be disposed of in accordance with the provisions of the earlier law.

- Where in pursuance of a contract entered into prior to the appointed day, the price of the goods is revised on or after the appointed day, the supplier may issue a supplementary invoice and the same shall be deemed to be outward supplies made under the GST Act.

- Any amount recovered / refunded pursuant to an assessment proceeding / revision of a return under an earlier law shall be recovered as arrears of tax under GST and shall not be eligible as ITC.

- Any amount of ITC reversed prior to the appointed day shall not be admissible as credit of input tax under this Act.

- Where any goods sent on approval basis, not earlier than 6 months before the appointed day, are rejected and returned to the supplier, no tax shall be payable thereon if the goods are returned within 6 months from the appointed day. In case the goods are returned after the so prescribed period, tax shall be payable by the person returning the goods.

Creating values through………

- Feasibility study of existing business processes

- Designing & implementing new business models

- Streamlining the compliance requirements

- Complete business outsourcing of finance & tax solutions

- Organizing training and awareness sessions for corporates

- Assisting business operations in the transition phase