APPEALS UNDER GST

(PROVISIONS GOVERNING APPEALS UNDER THE CENTRAL GST ACT, 2017 WHICH ARE APPLIED TO THE STATE/UT GST ACT, 2017 & THE INTEGRATED GST ACT, 2017 MUTATIS MUTANDIS.)

HIERARCHY OF APPEALS UNDER GST

> The First Appeal can be filed against an order issued by Adjudicating Authority to Appellate Authority by Assessee within 3 Months* from the issue of such order.

> The Appeal can also be filed by GST Department itself against the order issued by it if it is against the interest of revenue or after taking review by the Commissioner/Chief Commissioner within a period of 6 Months** from the issue of such order to The Appellate Authority.

> Before filing Appeal Assessee has to make payment of 10% of amount disputed*** related to Tax only But if Appeal is filed against the amount of Penalty then 10% of Penalty disputed is to be paid in such case. For the amount accepted by Assessee shall be paid entirely.

- *The time limit to file appeal by Assessee can be extended by Appellate Authority if reasonable cause exists by further 3 months. (3M+3M)

- **The time limit to file appeal by GST Deptt. Itself can be extended by 1 month if reasonable cause exists by Appellate Authority.(3M+1M)

- *** The pre-deposit of tax is least of following:

(A) 10% of Tax disputed

(B) Maximum Rs. 25 Crores.

NOTE: This Limit is only for Central GST means total amount will be doubled in case of CGST+SGST or IGST, as the case may be.

If Assessee is aggrieved by the order passed by Appellate Authority then he can lodge further Appeal against the order issued by Appellate Authority to GST Appellate Tribunal (GSTAT) within a period of 3 Months* from the issue of such order.

If The Deptt. is unsatisfied with the decision of Appellate Authority then it can also file a further Appeal against such order to GSTAT within a period of 6 Months** from the issue of such order.

If Assessee file Appeal with GSTAT then he shall pay 20% of Disputed Tax amount*** (Additionally to 10% deposited earlier at the time of Appellate Authority).

*The time limit to file appeal by Assessee can be extended by GSTAT if reasonable cause exists by further 3 months. (3M+3M)

**The time limit to file appeal by Deptt. Can not be further extended by GSTAT.

*** The pre-deposit of tax is least of following:

(A) 20% of Tax disputed

(B) Maximum Rs. 50 Crores.

NOTE: This Limit is only for Central GST means total amount will be doubled in case of CGST+SGST or IGST, as the case may be.

# The appeal shall be disposed off by Appellate Authority within 1 Year from the date of filling Appeal, Wherever possible.

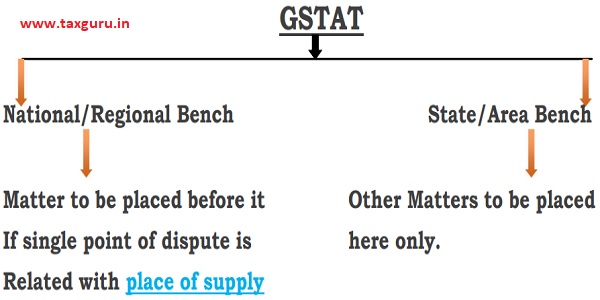

BENCHES UNDER GSTAT:

REVISIONARY AUTHORITY

> Revisionary Authority can suo-moto or at the request of CoCGST or CCoCGST revise the order issued by GST Deptt. Within a period of 3 Years from the date of issue of such order.

> An Appeal can also be filed against the order passed by Revisionary Authority by the Assessee or the Department itself.

> An Assessee can file Appeal Against it within 3 Months* of Order passed by it to GSTAT directly.

> The GST Deptt. Can file Appeal Against it Within 6 Months** of Order passed by it to GSTAT directly.

*The time limit to file appeal by assessee can be extended by GSTAT by further 3 months if reasonable cause exists.(3M+3M)

**The time limit to file appeal by Deptt. Can not be further extended by GSTAT.

# CoCGST= Commissioner of CGST

# CCoCGST= Chief Commissioner of CSGT

FACTS RELATED TO GSTAT:

1. GSTAT is the Final Fact Finding Authority means Appeal against the order passed by GSTAT can be forwarded to The High Court & The Apex Court only if it involves a Substantial Question of law.

2. It can rectify its order if mistake is apparent from records within a period of 3 Months from the issue of order by itself.

3. Appeal against the order passed by The National or Regional Bench of GSTAT can be lodged in front of The Apex Court directly.

4. Appeal against the order passed by The State/Area Bench of GSTAT can be filed first in front of The High Court within 180 days from the order passed by GSTAT.

5. Memorandum of Cross Objection (MOCO) can be filed within 45 days from the intimation by respondent. The GSTAT can condone the delay by further 45 days if the reasonable grounds are exists.

*The pre-deposit of disputed amount can be stayed by HC & SC, as the case may be.

**Delay in filing appeal can be condoned by HC & SC according to their respective Laws.

There is no guidance about it in The CGST/SGST/UTGST/IGST Act.

# The appeal shall be disposed off by GSTAT within 1 Year from the date of filling Appeal, Wherever possible.

6. GSTAT can reject the Appeal if it involves the disputed amount upto Rs. 50,000/-

7. A Single Member bench can be dispose the Appeal if it involves disputed amount upto Rs. 5,00,000/-

8. GSTAT has an exclusive right to Remand the Case Back to GST deptt. In case the Assessment is not done properly but The Appellate Authority Does not have any such right although it can Re-assess if it thinks to do so.

ADJUDICATING AUTHORITY?

Adjudicating Authority Includes:

1. Joint Commissioner/ Additional Commissioner

2. Assistant Commissioner/ Deputy Commissioner

3. Superintendent

IMPORATANT FACTS RELATED TO APPEAL:

1. The Appeal against the Assistant Commissioner/ Deputy Commissioner / Superintendent can be filed to The JOINT COMMISSIONER (APPEALS) first.

2. The Appeal against The JC(APPEALS) can be filed to GSTAT directly.

3. The Appeal against the order passed by The Joint Commissioner/Additional Commissioner can be filed directly to The COMMISSIONER (APPEALS).

4. The Appeal against the order passed by The Commissioner (Appeals) can be filed to GSTAT first.

5. Appeal Can not be filed against the NON-APPELLABLE Orders.

Author Bio