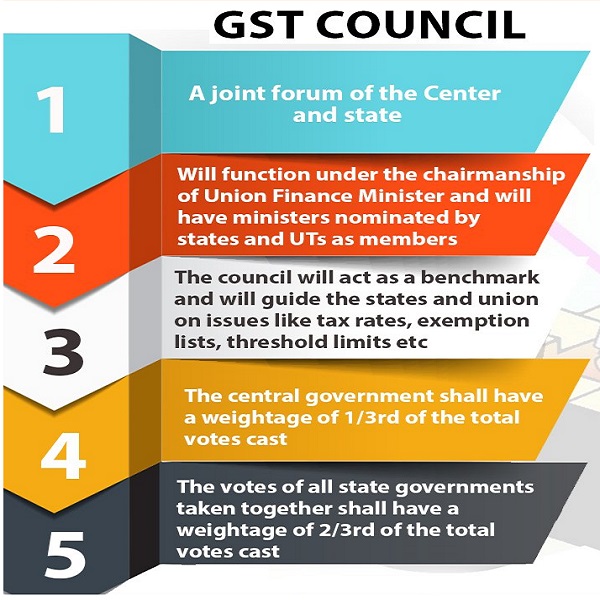

On 3rd November the meeting of GST council commenced with great hope, though there was some apprehension that debate on rate structure may remain inconclusive. But to surprise of every one the issue was sorted out and rate structure was unanimously agreed and cheered by businesses. Expectations soared. But the second day meeting was abruptly curtailed as there was total disagreement about power to assess and administer.

It is now out in the open that central Government wants all the powers to assess those whose turnover is above 1.5 crore and all service suppliers. If it is true and I believe it is so, then it is sheer matter of superiority complex on the part of Central Government, which is supposed to be at the behest of excise department. But state Governments also must shoulder the blame for It.

Under excise removal of goods has paramount importance. Excise is single point tax. Goods service tax is multi point tax which is nearer to VAT laws. If you look at the draft of Model GST Act you will realise that it is dominated by excise concepts. Special provision for job work, capital goods, input tax credit you name it and you will find foot print of excise in almost entire draft. Many provisions in Model draft of GST appear to be copy pasted from Central Excise and service tax provisions. Little thought appears to be given to the change in the subject matter of tax. Excise is applicable to organized sector. Majority of taxable persons under GST will be from unorganized sector, for whom these provisions will be difficult to comprehend and implement. It is learnt and appears that states either did not take part in drafting or they did not raise any objections effectively. Therefore I say that state Governments are responsible for creating superiority complex as mentioned above. But still there is time to redeem the situation. States must become active while draft is being finalized. Because it is necessary to remove the tilt towards excise provisions many of which are not compatible to GST.

Now it appears that Central Government wants control over the assessment of all suppliers of services and supplier of goods who are at present being assessed under excise and service tax. Therefore Central Government has proposed that power to assess having turnover above 1.5 crore shall be with Central Government. Why limit of 1.5 crore and why not 3, 4, or 5 crore? Because, the threshold limit for applicability of excise at present is 1.5 crore – it is so simple – Copy pasting method. If it is finally accepted, it will means peanuts powers to state governments. All states must come together to resist the Central Government shed the inferiority complex, if any, and secure sufficient powers under GST. States must also ensure that final draft of Act is simple to understand for the small and medium scale businesses. At present it is not so.

The central Government may be apprehensive that VAT official will have difficulty to understand the GST particularly taxation of services. As if all wisdom rests in central Government. Understanding taxation of services is not a rocket science. By training and experience the VAT officers are capable of learning the niceties of it. Having decided to brought goods and services under one Act and system, it will be travesty not to share power, to assess services, with states. I only hope that better sense will prevail and the matter will be sorted out amicably.

Suggestion : I would suggest that the taxable person having registration under one state only will be assessed by State authorities irrespective of the turnover and also irrespective of, whether he supplies services or goods or both. Power to assess all persons who have registration in more than one state may rest with Central Government. This will ensure that there is no conflicting view between one state and another. Under no circumstances the taxable person shall be subjected to assessment by both the authorities. This will relieve the taxable persons having multi state activities of being assessed by different states. The states will also get power to assess the large tax payers and services. In long run it will be beneficial to all.

Author Bio