The Government vide Notification No. 14/2022 – Central Tax dated 05th July, 2022 has notified few changes in Table 4 of Form GSTR-3B for enabling taxpayers to correctly report information regarding ITC availed, ITC reversal and ineligible ITC in Table 4 of GSTR-3B.

*Changes are highlighted as Red text in above img.

Below are the changes done in Table 4 of GSTR-3B.

All the non-reclaimable reversals i.e., reversal of ITC in cases where it can never be claimed in future such as reversal of ITC in case of damaged stock, stock sold free of cost and other cases of similar nature is to be reported in table 4(B)(1).

All reclaimable ITC reversals such as reversal of ITC in case of non-payment to vendor within 180 days where ITC can be reclaimed once the payment is made to the vendor and other such reclaimable nature transactions, may be reported in table 4(B)(2). It should be noted that ITC reversed under 4(B)(2) can be reclaimed in table 4(A)(5) at appropriate time and the break-up detail of such reclaimed ITC should be provided in 4(D)(1) in the same return.

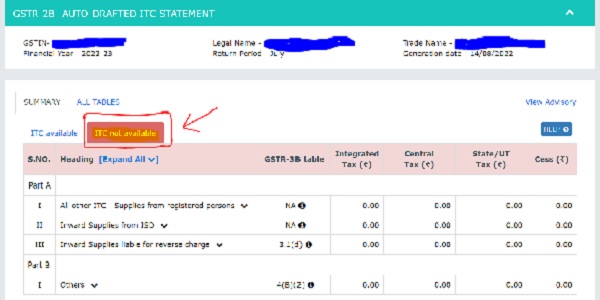

The ITC not-available mentioned in GSTR-2B of the taxpayer has to be reported in 4(D)(2) of table 4.

Any ITC availed inadvertently in Table 4(A) in previous tax periods due to clerical mistakes or some other inadvertent mistake maybe reversed in Table 4(B)2.

These are the major crux of the circular that one should keep in mind while filing GSTR-3b from Aug-22 onwards. For more clarification once can refer to the Circular No. 170/02/2022-GST issued by CBIC

Author Bio

Appreciate government making many changes periodically in making the tax payers file GST3B on time.

Small company’s depend on timely payments from their clients to run their business and for making statutory payments such as GSTR 3B etc. But Government has not made any rules for clients to make payments to vendors on time within time frame such as 15 or 30 days. Many small businesses company’s like us pay GST to government from our money or loan to avoid late payment and interest. Finally small companies like us are facing loss due to delayed payments by clients. We would appreciate if some rules are brought up for making payment on time and avail Gst ITC.

SMSE Provisions are there to take care of the same.