There are certain tasks that the taxpayers need to undertake during the end of each financial year (i.e. FY 24) in order to have a smooth transition to new financial year (i.e. 2024-25). Accordingly, we have listed down certain important activities that needs to be completed before the end financial year 2023-24.

The four activities as given below in the box are explained subsequently in details:

|

Reconciliations, ITC and outward Tax |

Other Important Aspects |

| Measures to be taken | Pro- active planning |

1. Reconciliations, ITC and outward Tax

a. Inward Reconciliation: –

i. GSTR 3B/2B Vs Inward register:

It is important to avail all your pending input tax credit for the ending financial year and to complete the GST reconciliation of GSTR 2B with your inward register namely purchase invoices, service invoices, expenses invoices, RCM invoices etc.

ii. Follow up with Suppliers:

A dedicated follow up with suppliers is required in cases wherein stated transactions is not populated in your GSTR 2B. Supplier should furnish/report transactions in their GSTR 1 with payment of taxes in GSTR 3B to avoid any unnecessary disputes later.

iii. Payments pending for more than 180 days:

Review the outstanding statement of suppliers to check the status of any payment which was pending beyond 180 days from the date of issuance of supplier’s invoice. ITC availed against those invoices whose payment are not released within 180 days needs to be reversed along with interest @ 18%. However, the same could be re-availed after respective payments.

iv. Ineligible credit reversals:

Ineligible ITC like blocked credit/ ITC on exempt supplies should be identified properly which were availed in GSTR 3B during FY 2023-24. If the same was utilised, it needs to be reversed/deposited along with interest thereon @18% in order to avoid any demand of tax, interest or penalty in future. However, please note that if the said ITC was not utilised, no interest & penalty is leviable on reversal of wrongly availed credit.

v. GST TDS/TCS:

It is important to cross verify the amount of GST TDS/TCS credit with books as the said amount gets transferred to the E-Cash ledger at the year-end.

b. Outward Reconciliations: –

i. GSTR 1/3B vs Outward Register:

Reconciliations should be prepared in respect of outward supplies as reported in GSTR 1 vs GSTR 3B vs Books of accounts. The same should also include classification of supplies under correct SAC/HSN code, GST rate, head (Export/SEZ) etc.

ii. Sales Register Vs Online Invoices Vs E-way Bills:

Reconciliation prepared in the above point should also be cross-checked with online portal invoices (wherever applicable) and E-way bills to avoid any variances later. It may help to avoid demand of tax, interest, or penalty during GST departmental audits.

iii. Tax Reconciliations:

Reconcile the amount of taxes paid GSTR 3B as well as declared in GTSR 1 during the FY 2023-24 with books of accounts. In case, if there is any shortfall, the same should be paid/ deposited.

iv. Advance adjustments:

A working should be prepared to capture the adjustments of the details of GST paid on advances received during FY 2023-24 against the supply of services made or agreed to be made.

v. Amendment/ Rectifications:

It is good to amend/ rectify any mistakes or omissions made in GSTR-1 or GSTR 3B returns (like uploading wrong GSTIN, submitting B2C invoices instead of B2B invoices, omitted invoices, etc.) in March 2024 returns.

2. Other Aspects

a. Reverse Charge mechanism (‘RCM’)

Review the transactions covered under RCM (like import of Services, sitting fees paid to directors, GTA, security services, rent a cab, advocate fees, etc.,) from registered suppliers as well as unregistered suppliers and make the payment of tax under RCM. The payment should be made as per time of supply provisions and thereafter, ITC could be claimed if not paid and claimed earlier. Further, respective self-invoice should also need to be raised against all the supplies received from unregistered person whose goods or services are covered under RCM.

b. GST Refund:

A streamlined GST process allows taxpayers to get a GST refund when they pay more tax than what they owe in certain circumstances. If taxpayers want to receive their GST refund, they must apply for it correctly duly within time. The refund will be credited to their respective bank accounts in accordance with the GST refund procedure. Refund could be applied for 11 cases as mentioned under GST law.

c. Material sent for Job work

Check whether the material sent for job work has been returned within the prescribed time limit (i.e. for Inputs – 1 year and for Capital goods – 3 years) and whether the same has been duly reported in ITC 04.

d. Goods sent on Approval Basis

Check whether the goods sent on approval basis has been either returned within 6 months or sold on issuance of tax invoice or not.

e. Misc.

Ensure that all the other provisions of GST Law (industry specific) have been duly complied with or not.

3. Measures to be taken

a. Fresh Invoice number series:

As per GST advisory, GST taxpayers should start a new (unique) series of invoices/ bill of supplies with the start of every new financial year. It helps in generating E-way bills on the E-way bill system, furnishing GST returns, applying for GST refunds etc.

b. Opt-in or out of GST Schemes:

i. QRMP Scheme under GST:

Registered persons having aggregate turnover up to Rs 5 Cr. are allowed to furnish their GST returns on a quarterly basis along with monthly payment of tax under Quarterly Return Monthly Payment or QRMP scheme under GST. The same should be timely opted in order to avoid any confusion later

ii. Composition Scheme under GST:

If you wish to opt for Composition Scheme for the financial year 2024-25 (both supplier of goods and service provider) in case of any small unit or company, the same should be opted by filing Form CMP-02 by 31st March 2024.

c. LUT – Exports / Supply to SEZ:

In terms of rule 96A of CGST Rule, 2017, any registered person availing the option to supply goods or services for export without payment of IGST needs to furnish, a bond or a LUT (Letter of Undertaking) in Form GST RFD-11. The validity of an LUT is generally of a financial year i.e. the LUT filed during FY 2023-24 is valid only till 31st March, 2024. Accordingly, a fresh LUT is need to be furnished by 31ST March,2024 or before supply for Exports / SEZ.

d. Physical Stock Checking

In order to be prepared well in advance for income tax and GST departmental audit, it is important that there should be no difference in physical stock and the books of accounts. The same is also essential to have a look on ITC reversals with respect to goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples.

4. Pro Active planning

a. ISD registration:

In line with the recommendations of the 50th council meet, the Finance Bill 2024 have proposed the following amendments to the CGST Act, 2017:

Proposed amendment to Section 2 (61) of the CGST Act, 2017:

” 2(61) “Input Service Distributor” means an office of the supplier of goods or services or both which receives tax invoices towards the receipt of input services, including invoices in respect of services liable to tax under sub-section (3) or sub-section (4) of section 9, for or on behalf of distinct persons referred to in section 25, and liable to distribute the input tax credit in respect of such invoices in the manner provided in section 20;”

Proposed amendment to Section 20 of the CGST Act, 2017:

“20 (1) Any office of the supplier of goods or services or both which receives tax invoices towards the receipt of input services, including invoices in respect of services liable to tax under sub-section (3) or sub-section (4) of section 9, for or on behalf of distinct persons referred to in section 25, shall be required to be registered as Input Service Distributor under clause (viii) of section 24 and shall distribute the input tax credit in respect of such invoices.

(2) The Input Service Distributor shall distribute the credit of central tax or integrated tax charged on invoices received by him, including the credit of central or integrated tax in respect of services subject to levy of tax under sub-section (3) or sub-section (4) of section 9 paid by a distinct person registered in the same State as the said Input Service Distributor, in such manner, within such time and subject to such restrictions and conditions as may be prescribed.

(3) The credit of central tax shall be distributed as central tax or integrated tax and integrated tax as Integrated tax or central tax, by way of issue of a document containing the amount of input tax credit, in such manner as may be prescribed.”.

Analysis of proposed amendments

Presently, it is not mandatory to distribute the common ITC among the branches via the ISD mechanism and the assessee can opt for cross charge billing for such distribution. (as clarified by Circular 199/11/2023-GST dated 17th July 2023)

However, with the proposed amendment to section 20 of the CGST Act,2017, all assessee having multi – state GST registration will have got themselves mandatorily registered as ISD to distribute the common ITC credit among its branches located in different state in the manner that will be prescribed separately.

Also, now with proposed new definition the person obtaining the ISD registration will have to now distribute the ITC in relation to reverse charge payment which is missing in the current definition.

Challenges

Now with ISD set to become a mandatory thing, all the assesses will have to strategize on how to implement the same. Also, assesses currently distributing common ITC through cross charge will now have to modify their systems and distribute the common ITC through ISD mechanism only. However, the common expenses of a group should be done through cross charge.

Further, the companies also need to consider whether they can follow single ISD registration or have multiple registrations. This would be specifically applicable in case of Banking & Insurance wherein there are concepts of regional and zonal offices. With ISD registration the assesses having vertical wise registrations / multi state presence will now have face quite a few challenges especially in area of compliances which will be going to increase.

The main challenge would be capturing invoices for common expenses where GST is payable under Reverse Charge Mechanism under ISD registration, discharging the same and distributing the said ITC.

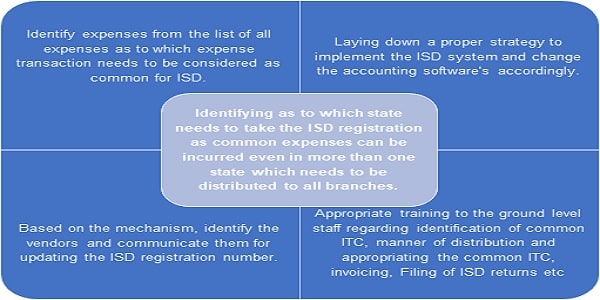

Steps to be taken.

For implementing the new ISD mechanism the assesses will be required to do following exercise:

One needs to wait for mechanism to be prescribed for such payment and distribution.

Conclusion: As businesses prepare to close the books on the current financial year, adherence to these key GST activities is paramount. By proactively addressing reconciliations, compliance issues, and strategic planning, taxpayers can navigate the year-end process smoothly and position themselves for success in the upcoming fiscal period. Hope the aforementioned activities are useful.