The Goods and Services Tax (GST) framework in India includes various mechanisms to ensure seamless tax credit flow across different branches of a business. One such mechanism is the Input Service Distributor (ISD). An ISD is a taxpayer that receives invoices for services utilized by its branches and distributes the Input Tax Credit (ITC) to these branches proportionally through ISD invoices. While these branches may have different GSTINs, they must share the same PAN as the ISD. This article delves into the ISD mechanism, its current clarifications, upcoming changes, and the procedural requirements for businesses.

> What is an Input Service Distributor (ISD)?

An Input Service Distributor (ISD) is a taxpayer that receives invoices for services utilized by its branches and distributes the Input Tax Credit (ITC) to these branches proportionally through ISD invoices. While these branches may have different GSTINs, they must share the same PAN as the ISD.

√ Current Clarifications and Future Changes

- According to Circular 199/11/2023-GST dated 17th July 2023, it is clarified that distributing common ITC among branches via the ISD mechanism is not mandatory. Taxpayers may opt for cross-charge billing instead.

- However, the 2024 budget introduces significant changes to the ISD mechanism under GST. These changes, based on recommendations from the GST Council’s 50th and 52nd meetings, will mandate the distribution of ITC for services procured by the Head Office (HO) that are attributable to both the HO and the Branch Offices (BO) or exclusively to one or more BOs. This will be achieved through amendments to Section 2(61), Section 20 of the CGST Act, 2017, and Rule 39 of the CGST Rules, 2017.

- These amendments aim to streamline and clarify the ITC distribution procedure, ensuring consistency and compliance. Once implemented, all assessee with multi-state GST registrations must register as ISD to distribute common ITC credit among their branches located in different states. The proposed amendments also include the mandatory distribution of ITC in relation to reverse charge payments, which is not covered under the current definition.

√ Definition Changes

- Current Definition:

Section 2(61) of the CGST Act, 2017

“Input Service Distributor” means an office of the supplier of goods or services or both which receives tax invoices issued under section 31 towards the receipt of input services and issues a prescribed document for the purposes of distributing the credit of central tax, State tax, integrated tax or Union territory tax paid on the said services to a supplier of taxable goods or services or both having the same Permanent Account Number as that of the said office;

** Section 31 – Defines Tax Invoices

- Amended Definition:

Section 2 (61) of the CSGT Act, 2017

Input Service Distributor” means an office of the supplier of goods or services or both, which receives tax invoices towards the receipt of input services, including invoices in respect of services liable to tax under sub-section (3) or sub-section (4) of section 9, for or on behalf of distinct persons referred to in section 25, and liable to distribute the input tax credit in respect of such invoices in the manner provided in section 20

** Section 9(3) – RCM for registered suppliers & 9(4) RCM for unregistered persons;

** Section 25 – Pan-India registration with same PAN number – called distinct persons.

** Section 20 – Defines the procedure for ISD

√ Distribution Procedure under Section 20 of the CGST Act, 2017 changes

- Current Procedure:

Section 20 of the CSGT Act, 2017:

Manner of distribution of credit by Input Service Distributor:

(1) The Input Service Distributor shall distribute the credit of central tax as central tax or integrated tax and integrated tax as integrated tax or central tax, by way of issue of a document containing the amount of input tax credit being distributed in such manner as may be prescribed.

(2) The Input Service Distributor may distribute the credit subject to the following conditions, namely:

(a) the credit can be distributed to the recipients of credit against a document containing such details as may be prescribed;

(b) the amount of the credit distributed shall not exceed the amount of credit available for distribution;

(c) The credit of tax paid on input services attributable to a recipient of credit shall be distributed only to that recipient;

(d) the credit of tax paid on input services attributable to more than one recipient of credit shall be distributed amongst such recipients to whom the input service is attributable and such distribution shall be pro rata on the basis of the turnover in a State or turnover in a Union territory of such recipient, during the relevant period, to the aggregate of the turnover of all such recipients to whom such input service is attributable and which are operational in the current year, during the said relevant period;

(e) the credit of tax paid on input services attributable to all recipients of credit shall be distributed amongst such recipients and such distribution shall be pro rata on the basis of the turnover in a State or turnover in a Union territory of such recipient, during the relevant period, to the aggregate of the turnover of all recipients and which are operational in the current year, during the said relevant period.

- Amended Procedure:

Section 20 of the CSGT Act, 2017:

(1) Any office of the supplier of goods or services or both which receives tax invoices towards the receipt of input services, including invoices in respect of services liable to tax under sub-section (3) or sub-section (4) of section 9, for or on behalf of distinct persons referred to in section 25, shall be required to be registered as Input Service Distributor under clause (viii) of section 24 and shall distribute the input tax credit in respect of such invoices.

(2) The Input Service Distributor shall distribute the credit of central tax or integrated tax charged on invoices received by him, including the credit of central or integrated tax in respect of services subject to levy of tax under sub-section (3) or sub-section (4) of section 9 paid by a distinct person registered in the same State as the said Input Service Distributor, in such manner, within such time and subject to such restrictions and conditions as may be prescribed.

(3) The credit of central tax shall be distributed as central tax or integrated tax and integrated tax as integrated tax or central tax, by way of the issue of a document containing the amount of input tax credit, in such manner as may be prescribed.

> Conditions to be fulfilled by ISD

- Registration: Input Service Distributor has to compulsorily register as “ISD” apart from its registration under GST as a normal taxpayer. Such taxpayer has to specify under serial number 14 of the REG-01 form as an ISD. They shall be able to distribute the credit to the recipients only after this declaration.

- Invoicing: ISD can distribute the amount of tax credit to recipients as earlier stated by issuing an ISD invoice.

- Returns: The amount of tax credit distributed should not exceed the amount of tax credit available with the ISD at the end of a relevant month to be filed in GSTR-6 by the 13th of the succeeding month by the ISD. The ISD can get the information of the ITC from the GSTR-2B return. The recipient of the tax credit can view the tax credit so distributed by ISD in GSTR-6A that is auto-populated from the supplier’s return. In turn, the recipient branch can claim the same by declaring it in GSTR-3B. An ISD need not file annual returns in form GSTR-9.

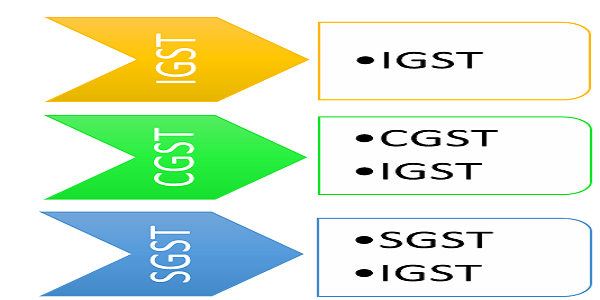

- Restrictions: Credit under reverse charge cannot be distributed and must be used by ISD as a normal taxpayer. The distribution of CGST, IGST, and SGST is prescribed and follows a proportional basis based on recipient turnover.

- The credit of CGST, IGST, and SGST shall be distributed, in the prescribed manner as per the below chart:

- The tax credit available against any specific input services used entirely by one of the recipients can be allocated only to that recipient for utilization of such credit and not to other recipients.

- The tax credit available against the input services used commonly by more than one recipient of the ISD shall be allocated to those recipients on a proportionate basis in the ratio of the turnover of all such recipients that are operational during the year.

> Situations where ISD is not applicable

ISD cannot distribute the input tax credit in the following cases:

- Distribution of Input Goods or Capital Goods Credit: ISD provisions are strictly for distributing the credit of input services. They do not apply to the distribution of credit for input goods or capital goods. Therefore, any credit related to input goods or capital goods cannot be distributed using the ISD mechanism.

- Distribution of Credit for Services Not Used by the Recipient: The ISD mechanism is intended to distribute credit for input services that are used by the recipient units. If the input services are not used by a particular unit, the credit for those services cannot be distributed to that unit through ISD.

- Distribution to Entities Not Registered under the Same PAN: The ISD mechanism applies only to entities that are registered under the same Permanent Account Number (PAN). Credit cannot be distributed to entities that do not share the same PAN.

- Distribution Outside India: ISD provisions are meant for the distribution of credit within India. Any distribution of input service credit to entities located outside India is not covered under the ISD mechanism.

- Distribution of Credit in case of Non-Availability of GST Registration: ISD provisions cannot be used if the distributing entity or the recipient entity does not have a valid GST registration. Both the distributor and the recipient must be registered under GST for ISD provisions to apply.

- Distribution to Non-Taxable Persons: ISD credit distribution applies to taxable persons only. If the recipient of the credit is a non-taxable person under GST, the ISD mechanism cannot be utilized.

- Use of ISD for other than Input Services: The ISD mechanism is strictly for input services. Any other type of distribution, such as distribution of goods or capital goods credit, must follow different procedures and cannot utilize the ISD mechanism.

Hence, post amendment, which is yet to be notified, all the companies who have multi state registrations will have to register themselves under ISD and distribute appropriate credit to the unit who is the actual user of the respective services.

Authors:

Jalpesh Vora | Partner | Email: jalpesh@bilimoriamehta.com

Bhavik Shah | Manager

Author Bio