Implementation of India’s Goods and Services Tax: Design and International Comparison

Introduction

The Goods and Services Tax (GST) was introduced in India on 1st July, 2017, after more than a decade of efforts. It replaced an existing system of fragmented and complex indirect taxes, consisting of multiple central and state taxes.104 Under the earlier tax system, states unilaterally levied ‘entry taxes’ on all goods that entered its territory, resulting in inefficiencies and huge costs to the economy. The new GST was designed to bring about a common policy and administrative framework for taxation of the supply of goods and services across the entire country while causing minimum tax based restrictions on trade, besides harmonizing the rates on goods and services. This note provides a brief description of the GST and benchmarks it against other countries.

GST Structure and Administration

Any tax on value added in a federal system of government with overlapping taxing powers is challenging, as taxing powers must be clearly defined and tax rates should be as uniform as possible across the country. The Indian GST applies to supply of most goods and services occurring throughout the territory of India with taxing powers assigned as follows:

- All sales within a state are taxed both by the center as well as the states over a common base and at the same rate, which together add up to the full GST rate. The taxes levied are called the State GST (SGST) and the Central GST (CGST), respectively.

- All sales from one state to another are taxed by the center at the full GST rate applicable. The relevant tax levied is called the Inter-State GST (IGST).

- For sales across state lines, any input taxes on purchases can be deducted (i.e. an input tax credit is available) from taxes collected on sales regardless of the source of the purchases.

The GST has different tax rates – 0, 5, 12, 18, and 28 percent.105 Further, there are several exempted sales and exports are zero rated, which allows exporters to claim refund for taxes paid on inputs. The GST excludes small firms with turnover below INR 2 million, and only taxpayers with turnover of INR 15 million (~US$230,770) or more charge GST on sales at the prescribed rates and can deduct GST paid on their purchases. Taxpayers who have turnover from INR 2 million to INR 15 million have the option of participating in a ‘composition scheme’ whereby they pay a tax on turnover instead on value added.

India Development Update, March 2018

The administration of GST has been harmonized between the center and the states using a common IT system and common rules with the powers to audit being shared.106 To support the administration of the taxpayers, a common nation-wide IT backbone called the GST Network (GSTN) has been put in place, through which all tax returns are required to be filed. This portal captures all tax returns and allows for verifying input tax credits claimed by businesses. The system can also aid in the selection of taxpayers for audit through a risk based selection mechanism. On the policy side, coordination between the Center and the States and, between States is made possible through a GST council comprising of the finance ministers of all the State governments and the Central government. The GST council is an innovative and integrative body that formulates a common policy and administrative framework for the GST that applies to the entire country.

The administration of GST has been harmonized between the center and the states using a common IT system and common rules with the powers to audit being shared.106 To support the administration of the taxpayers, a common nation-wide IT backbone called the GST Network (GSTN) has been put in place, through which all tax returns are required to be filed. This portal captures all tax returns and allows for verifying input tax credits claimed by businesses. The system can also aid in the selection of taxpayers for audit through a risk based selection mechanism. On the policy side, coordination between the Center and the States and, between States is made possible through a GST council comprising of the finance ministers of all the State governments and the Central government. The GST council is an innovative and integrative body that formulates a common policy and administrative framework for the GST that applies to the entire country.

Policy Parameters and Trade-Offs

The introduction of the GST to replace state level value added taxes was motivated by an attempt to harmonize indirect taxation across India, therefore eliminating state level barriers to trade and broadening the tax base. The challenge with designing any tax system is that most forms of taxation may reduce the private sector’s incentives to save or to invest. In addition to the direct burden of taxation, taxpayers are also affected by the cost of complying with tax obligations, for example through effort required to file tax returns.107 Taking these considerations into account, the design of the Indian GST system was guided by the objective to raise revenue while minimizing the burden of taxation on consumers and producers and limiting the cost of compliance to businesses.108 In practice, the fitment committee, tasked with selecting GST rates, approximated rates for a certain good or service to the most prevailing total rate including excise and state VAT and other levies. This procedure meant that the feature of traditional indirect taxes in India, which protected the consumption basket of the poor, has been maintained in the GST.109

GST design has two policy instruments to achieve these objectives: the tax rate and the tax base. The GST tax rate is the central parameter that determines the collection of tax revenue, with higher tax rates typically leading to higher tax collection rates, holding constant the tax base.110 However, increasing tax rates also increases the tax burden on firms and consumers, can discourage production and consumption and incentivize tax evasion.

The coverage of the GST is determined by two factors. First, the number of different tax rates (including the introduction of tax exemptions) determines the extent to which different products are covered. This design parameter is typically used to protect the consumption baskets of the poor and achieve other social objectives. The number of different tax rates also determines the complexity of the GST, with multiple rates imposing additional costs on compliance for businesses as well as the tax administration and encouraging evasion.

Second, the registration threshold determines which taxpayers are covered by the system. This is thus an instrument that governments can use to relieve smaller firms from the burden of complying with a GST. As is the case in India, it is also possible to introduce a simplified system in lieu of exemptions for smaller firms which is administratively easier. The disadvantage of introducing registration thresholds and having a simplified and presumptive tax regime is that it inevitably fragments the tax system, which may reduce the tax base and provide an incentive for larger firms to mask their size and benefit from the reduced compliance burden. In addition, tax schemes that levy taxes on sales rather than value added provide incentives for sellers to reduce their taxable sales, and potentially promoting economic inefficiencies by dis-incentivizing business growth, integration and expansion.

Taken together, this discussion suggests that the design of a GST systems faces trade-offs between revenue collection, protecting the poor and reducing the taxation and compliance burden on firms and consumers. The way that the design parameters are set is ultimately a policy decision that depends on the objectives of the government. The next section compares the design of the Indian system with international practices, keeping in mind that the introduction of a new tax system is the start of a process of reforms rather than the end and will require strong accompanying measures with continuous adjustments and improvements during implementation.

Tax Design: An international comparison

Comparing the design of India’s GST system with those prevailing internationally, we note that the tax rates in the Indian GST system are among the highest in the world. The highest GST rate in India, while only applying to a subset of goods and services traded, is 28 percent, which is the second highest among a sample of 115 countries which have a GST (VAT) system and for which data is available (Figure 61). Table 8 compares the highest and lowest standard tax rate (i.e. the tax rate that applies to the majority of transactions) across regions around the globe and shows that India has the highest standard GST rate in Asia. The table also highlights that the ASEAN region has the lowest rates as compared to the other regions.

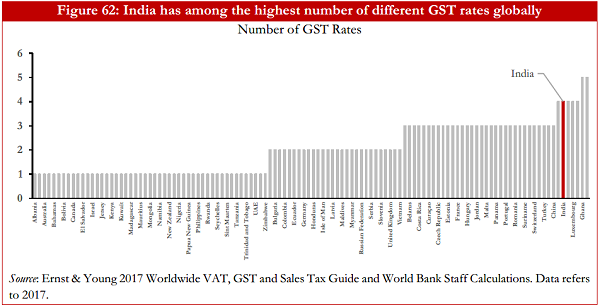

Next, we assess how the number of different GST rates prevalent in the Indian system, and thus its complexity, compares internationally. The Indian GST system currently has 4 non-zero GST rates (5, 12, 18, and 28 percent). Figure 62 shows the number of countries and the number of GST rates (not including the zero rate) among the sample of 115 countries described previously. Most countries around the World have a single rate of GST: 49 countries use a single rate, 28 use two rates, and only 5 countries including India use four rates. The countries that use four or more rates of GST include Italy, Luxembourg, Pakistan and Ghana. Thus, India has among the highest number of different GST rates in the world.

In addition to the number of rates, the extent of exemptions and sales at a zero rate is a critical design parameter for a GST. While exemptions allow to ease the tax burden on items with a high social value, such as healthcare, they also reduce the tax base and compromise the logic of the GST as they can: reintroduce cascading where an exempted good or service is an input into another taxable good or service; create incentives for vertical integration to keep the exempt status; and raise compliance costs by making it necessary to allocate input taxes between exempt and non-exempt output when manufactured or traded together.

In addition to the number of rates, the extent of exemptions and sales at a zero rate is a critical design parameter for a GST. While exemptions allow to ease the tax burden on items with a high social value, such as healthcare, they also reduce the tax base and compromise the logic of the GST as they can: reintroduce cascading where an exempted good or service is an input into another taxable good or service; create incentives for vertical integration to keep the exempt status; and raise compliance costs by making it necessary to allocate input taxes between exempt and non-exempt output when manufactured or traded together.

In contrast to other GST design parameters, comparing the prevalence of exemptions across countries is challenging. This is because the impact of declaring various goods as zero-rated does not only depend on the number of products exempt, but also on the revenue generated from each product. The latter figure is difficult to assess in the absence of tax revenue figures. Hence an assessment of the role of exemptions in the Indian GST system cannot be made before revenue figures have stabilized.111

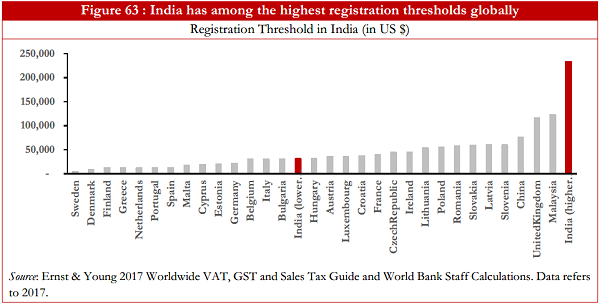

The threshold to register for the GST is another important policy parameter. In India, businesses having annual sales above the threshold of INR 15 million fall under the full GST, and are thus liable to remit GST and eligible to deduct input tax credit. Those with annual sales above the lower threshold of INR 2 million and below 15 million are required to register for the GST and pay a ‘flat’ 1 percent tax on sales, but are neither allowed to charge GST on sales nor deduct any taxes on inputs.

Comparing India internationally, Figure 63 shows the upper GST threshold for a sample of 31 countries compiled by the European Commission, which includes all the EU countries and China and Malaysia. India started with a higher threshold of $116,000 (7.5 million rupees) but in the span of a few months doubled it to $232,000 (15 million rupees) mainly to ease the cost of compliance for SMEs. India’s new threshold is the highest among all the 31 comparator countries.

The lower threshold of INR 2 million ($30,770) is in line with most countries in the EU. In contrast to the EU, however, the registration threshold in the EU applies to the full GST, unlike in the case of India where the lower threshold implies participation in the “composition scheme”. Such schemes for SMEs under the GST also exist in other countries, where businesses below a certain threshold pay a (lower) ‘flat’ turnover tax and are not allowed to collect tax as well as claim input tax credits. China and Poland use a similar ‘flat’ rate scheme. In other simplified schemes, businesses collect taxes on sales just like other registered GST business but can pay the tax as a ‘flat’ percentage of sales but the input credit is ‘deemed’ as a fixed percentage of sales. Such countries include the UK, Canada, Austria and Belgium.

Policy Considerations

The introduction of GST has been accompanied by state administrations experiencing disruptions in the initial days after GST introduction. This included a lack of clarity on discontinuation of local taxes (e.g. in Tamil Nadu where the state government devolved an entertainment tax to local governments in order to impose it over and above a 28 percent GST); demands for exemptions or lower tax rate (e.g. by the textile sector in Gujarat); and on account of coping mechanisms to preserve revenue collections (Maharashtra increased motor vehicles tax to compensate for losses due to GST). There also have been reports of an increased administrative tax compliance burden on firms and a locking-up of working capital due to slow tax refund processing. High compliance costs are also arising because the prevalence of multiple tax rates implies a need to classify inputs and outputs based on the applicable tax rate. Along with the need to apply the correct rate, firms are required to match invoices between their outputs and inputs to be eligible for full input tax credit, which increases compliance costs further.

To address these challenges, the GST council has begun a process of lowering and consolidating tax rates. In August 2017, the council lowered the tax rate for job work along the textile sector value chain to 5 percent from 18 percent. In September 2017, the GST rate on about 30 commonly used products was lowered, and this process was extended to another 27 goods in October 2017. On the administrative side, the GST council recommended faster processing and payments of refund claims. To ease the compliance burden for small and medium businesses the council changed the filing frequency from monthly to quarterly for firms with annual aggregate turnover up to INR 15 million. The council also increased the turnover limit for the “composition scheme” from INR 7.5 million to INR 15 million.

In addition to procedural amendments, the council is also considering technological improvements to facilitate GST administration. As such, the GST council announced the introduction of an “e-wallet” scheme by April 1st, 2018. Under this scheme, advance refund payments will be credited to a virtual account, which can be used to make GST related payments. In addition, early 2018 is expected to see the wider introduction of the “e-way bill system”, which facilitates a technology-driven tracking of movement of goods worth more than INR 50,000 and for sale beyond 10 km in distance.

Despite the initial hiccups, the introduction of the GST is having a far-reaching impact on reducing tax related barriers to trade barriers which was one of the primary goals of the introduction. Logistics companies are reporting that trucks now cover an additional 100-150 km per day after GST an increase of up to 30 percent.112 Logistics companies are also consolidating their existing fragmented set of small warehouses in each state, now that the GST has removed state imposed barriers thereby increasing their efficiency113. However, the introduction of the “e-way bill” may result in some fresh barriers to the free movement of goods in the form of road inspections to verify the goods being transported.

Conclusion

The introduction of GST in India is a historic reform. Comparing the design of India’s GST system to similar taxes on value added across other countries, the note highlights that India’s GST system is relatively more complex, with its high tax rates and a larger number of tax rates, than in comparable systems in other countries. However, while teething problems on the administrative and design side persist, the introduction of the GST should be considered as the start of a process, not the end. With the economy adapting to the new system, the GST council has been evaluating and evolving the tax structure and its implementation. While international experience suggests that the adjustment process can affect economic activity for multiple months, the benefits of the GST are likely to outweigh its costs in the long run. Key to success is a policy design that minimizes compliance burden, for example by minimizing the number of different rates and limiting exemptions, with simple laws and procedures, an appropriately structured and resourced administration, compliance strategies based on a balanced mix of education and assistance programs and risk-based audit programs. A nuanced communications campaign is crucial to convey the various aspects of the new system of GST amongst businesses, consumers and key intermediaries, such as tax practitioners, as well as amongst the tax administration itself and the political class.

Box 5: Preliminary Figures on Revenue Collection under GST

Due to its recent introduction, only preliminary figures on GST revenue are available. As the estimates cannot accurately account for the application of input credit and payments by taxpayers under the “composition scheme”, who only file returns every quarter, figures are subject to revision and should be treated as such.

Based on preliminary figures, collection from GST exceeded expectations initially, but has declined more recently. In the first month of taxes filed, July 2017, revenue was initially estimated at INR 922.8 billion and has since been revised upwards to INR 940 billion. Collection stems primarily from IGST, with SGST and CGST following. Since July, estimates of revenue collection have weakened slightly, with a dip to INR 837 billion in December 2017. In January, GST collections rose again to INR 888.9 billion. Possible reasons for the decline in November and December include an application of tax credit, consolidation of tax rates and the introduction of self-declaration. Since the introduction of GST in July 2017, government estimates suggest that the tax base has widened and a total of 10.3 million tax payers have registered on the new system as of February 15th, 2018. Data on 10 states suggests that there was no uniform pattern in change in sales tax revenues at the state level. Year-on-year growth of sales tax in July increased in 4 states (including Telangana and Himachal Pradesh), while it decreased in 6 states (including Punjab and Chhattisgarh).

Notes:

104 The GST replaced the following centrally levied taxes: Central Value Added Tax, Service Tax, Central Sales Tax, Countervailing Duties, Special Additional Duty of Customs. At the state level, the GST replaced the following taxes: Value Added Tax, Sales Tax, Entry Tax, Luxury Tax, Entertainment Tax.

105 Some goods receive special treatment under the GST: there is a special cess on luxury and “sin” goods. Gold is taxed at 3 percent rate, precious stones at 0.25 percent, while alcohol, petroleum products, stamp duties on real estate and electricity duties are excluded from the GST and they continue to be taxed by the state governments at state specific rates.

106 Audit and administration duties are shared as follows: For taxpayers with turnover not exceeding INR 15 million, state tax administrations administer 90 percent of taxpayers the central tax administration the remaining 10 percent. For taxpayers with turnover over 15 million 50 percent are administered by the central tax administration and 50 percent by the states.

107 See Rao (2017) for a discussion of tax system design in India.

108 Arvind Subramanian, the CEA, stated in April 2017 with regards to GST design: “[…] the guiding principle must be: what will make for a good GST, a GST that will: facilitate compliance, minimize inflationary pressures, be a buoyant source of revenue, and command support from the public at large.”

109Some commentators also imply that GST rates were chosen directly to protect the consumption basket of the poor: http://www.livemint.com/Opinion/yYtp9VpGJBMXpcsOkTfLEN/GSTs-last-and-critical-lap–Arvind-Subramanian.html

110 Higher tax rates only yield higher revenue as long as they don’t exceed the revenue-maximizing level, typically known as the peak of the so-called “Laffer curve”.

111 Despite these limitations, back of the envelope calculations suggest that the impact of exemptions on revenue collection for the GST is comparable with the international median. A way to measure the extent to which exemptions in the GST system is prevalent is by computing tax efficiency, defined as tax revenue as a share of the tax rate multiplied with GDP, with GDP measuring aggregate value added. In the absence of exemptions and full compliance, tax efficiency would equal 100 percent. India collected about 7 percent of GDP in taxes on goods and services prior to the introduction of the GST. Assuming the new GST would collect the same amount of tax (a revenue neutral policy was an important goal of the reform) and the GST rate is 15 percent (average of the 12 and 18 percent rate), this implies a GST-efficiency of approximately 47 percent. This leaves India in the 42nd rank among 106 countries being compared.

112 Average distance covered by trucks up by 100-150 km/day post GST (2017, Dec 31), Times of India. retrieved from timesofindia.indiatimes.com

113 Mundy, Simon. (2018, January 7). India’s tax overhaul unleashes logistics revolution. Financial Times.

Source- http://www.worldbank.org/en/news/press-release/2018/03/14/india-growth-story-since-1990s-remarkably-stable-resilient