The 50th Meeting of the GST Council was held on 11th July, 2023 in New Delhi, under the chairpersonship of the Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman. The GST Council inter-alia made various recommendations relating to changes in GST tax rates, measures for facilitation of trade and measures for streamlining compliances in GST. In this article, we are going to dive deep to understand one such recommendation relating to Circular to be issued on manner of calculating “Adjusted Total Turnover” w.r.t explanation inserted in Rule 89(4) of CGST Rules, 2017.

The exact phrase from Para 5(b) on the ‘Measures for facilitation of trade’ in Page 4 of the press release is reproduced below:

“Consequent to Explanation having been inserted in rule 89(4) of CGST Rules vide Notification No. 14/2022- CT dated 05.07.2022, the value of export goods, to be included while calculating “adjusted total turnover” in the formula under rule 89(4), will be determined as per the said explanation.”

A. EXPORT WITHOUT PAYMENT OF DUTY – THE FORMULA:

√ Section 16(3) of the IGST Act gives the option to an exporter to claim refund either as ITC by making export without payment of tax through LUT, as below:

“A registered person making zero rated supply shall be eligible to claim refund of unutilised input tax credit on supply of goods or services or both, without payment of integrated tax, under bond or Letter of Undertaking, in accordance with the provisions of section 54 of the Central Goods and Services Tax Act or the rules made thereunder, subject to such conditions, safeguards and procedure as may be prescribed”

√ The manner and the calculation for determining the amount of eligible refund of accumulated ITC for Exports made without payment of tax is prescribed in rule 89(4) of the CGST Rules, 2017.

The formula is reproduced below:

Refund Amount = (Turnover of zero-rated supply of goods + Turnover of zero-rated supply of services) x Net ITC ÷ Adjusted Total Turnover

√ Further Rule 89(4)(C) also defines what is ‘Turnover of Zero rated supply of goods’

Original definition:

89(4)(C) “Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking;

Substituted (w.e.f. 23.10.2017) by Notification No. 75/2017-C.T., dated 29.12.2017

(C) “Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking, other than the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both;”

Further substituted vide Notification No. 16/2020-CT dated 23.03.2020

89(4)(C) “Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking or the value which is 1.5 times the value of like goods domestically supplied by the same or, similarly placed, supplier, as declared by the supplier, whichever is less, other than the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both

B. WHAT’S THE ISSUE ALL ABOUT?

√ There are discrepancies between the Invoice Value and value in the shipping bill/bill of export and hence required clarity on which one should be adopted as export value for the purpose of refund. This has been clarified in circular no. 37/11/2018-GST dated 15/Mar/2018 and further reiterated in the Master Circular 125/44/2019 dated 18/Nov/2019 that the lower of the two is to be considered in the numerator for calculating the refund. Para 9 of circular no. 37/11/2018-GST dated 15/Mar/2018 is reproduced below:

9. Discrepancy between values of GST invoice and shipping bill/bill of export: It has been brought to the notice of the Board that in certain cases, where the refund of unutilized input tax credit on account of export of goods is claimed and the value declared in the tax invoice is different from the export value declared in the corresponding shipping bill under the Customs Act, refund claims are not being processed. The matter has been examined and it is clarified that the zero rated supply of goods is effected under the provisions of the GST laws. An exporter, at the time of supply of goods declares that the goods are for export and the same is done under an invoice issued under rule 46 of the CGST Rules. The value recorded in the GST invoice should normally be the transaction value as determined under section 15 of the CGST Act read with the rules made thereunder. The same transaction value should normally be recorded in the corresponding shipping bill / bill of export.

9.1 During the processing of the refund claim, the value of the goods declared in the GST invoice and the value in the corresponding shipping bill / bill of export should be examined and the lower of the two values should be sanctioned as refund.

√ Whereas this clarification has created further ambiguity amongst the taxpayers and the tax officers on two matters:

1. There are two values reflecting in the Shipping Bills – (1) the invoice value based on the terms of shipment and (2) FOB value. If the incoterms of shipment are CIF, C&F, DDP, etc., the invoice value and the FOB value will differ. In such a case, which value to consider as Shipping Bill Value – invoice value or FOB value?

2. Which value to be considered as export value for the purpose of the calculation of Adjusted Total Turnover – whether the value determined in the numerator as ‘Turnover of Zero rated supply of goods’ or the value as declared in the returns filed for the relevant period?

√ As per export promotion policy of the Government, all export benefits under the Foreign Trade Policy (FTP) shall always be at FOB value, in order to eliminate discrimination due to different incoterms followed by various exporters merely attributable towards cost of freight, insurance, etc. and to create a level playing field.

√ With only internal communications given to the officers in this regard, refund applications were processed by adopting ‘FOB value’ as ‘Turnover of Zero-rated supply of goods’ and the difference being rejected, without any such rules prescribed in this regard then.

√ However, the same has been later ratified by inserting an explanation to rule 89(4) of the CGST Rules 2017 vide Notification No. 14/2022-CT dated 05/July/2022. The exact explanation is reproduced below:

“Explanation.–For the purposes of this sub-rule, the value of goods exported out of India shall be taken as –

(i) the Free on Board (FOB) value declared in the Shipping Bill or Bill of Export form, as the case may be, as per the Shipping Bill and Bill of Export (Forms) Regulations, 2017; or

(ii) the value declared in tax invoice or bill of supply,

whichever is less.”

Note: By inserting this as an ‘explanation’, Government also tried to ratify it for the past matters, since explanations are usually given to explain the meaning of how it is expected to be understood always, including for the past period! Though this can be a matter of debate!

√ However, the second question on which value to be considered as export value for the purpose of the calculation of Adjusted Total Turnover – whether the value determined in the numerator as ‘Turnover of Zero rated supply of goods’ or the value as declared in the returns filed for the relevant period – remained unanswered.

√ Meanwhile, when a similar question aroused post substitution of Rule 89(4)(C) vide Notification No. 16/2020-CT dated 23.03.2020 imposing restriction on the export value limited to 1.5 times the value of like goods domestically supplied, Circular 147/03/2021-GST, dated 12/Mar/2022 has clarified the manner of calculation of Adjusted Total Turnover in terms of Zero-rated turnover (export turnover) being determined as per amended rule 89(4)(C). The exact extract from para 4 of Circular 147 is reproduced below:

“4.6 – Accordingly, it is clarified that for the purpose of Rule 89(4), the value of export/ zero-rated supply of goods to be included while calculating ‘adjusted total turnover’ will be same as being determined as per the amended definition of ‘Turnover of zero-rated supply of goods’ in the said sub-rule.”

At this juncture, it is noteworthy to refer to the decision of the Hon’ble Karnataka High Court in M/s. Tonbo Imaging India Pvt Ltd v. Union of India [W.P.C No. 13185 of 2020] (T-RES) dated February 16, 2023, where Rule 89 (4)(C) restricting the exports made without payment of tax to 1.5 times value of like goods supplied domestically, is held UNCONSTITUTIONAL and ULTRAVIRES the provisions of the GST Act, since it is violative of Article 14 and 19(1)(g) of the Constitution of India. While this decision on the High Court could be further tested in the Apex court, we are refraining from getting into any further analysis of this judgment, to stay focused on the issue of FOB value rather.

√ Getting back to the issue of FOB value, though circular 147 has clarified the manner of calculating Adjusted Total Turnover, the same has been restricted only to the extent of clarifying in terms of Rule 89(4)(C) and not on the explanations inserted.

C. EXPECTING A CIRCULAR!

√ In order to set an end to this ambiguity, it has been decided in the 50th GST Council Meeting to clarify on the same by way of issuing a circular. The exact phrase from Para 5(b) on the ‘Measures for facilitation of trade’ in Page 4 of the press release is reproduced below:

“Consequent to Explanation having been inserted in rule 89(4) of CGST Rules vide Notification No. 14/2022- CT dated 05.07.2022, the value of export goods, to be included while calculating “adjusted total turnover” in the formula under rule 89(4), will be determined as per the said explanation.”

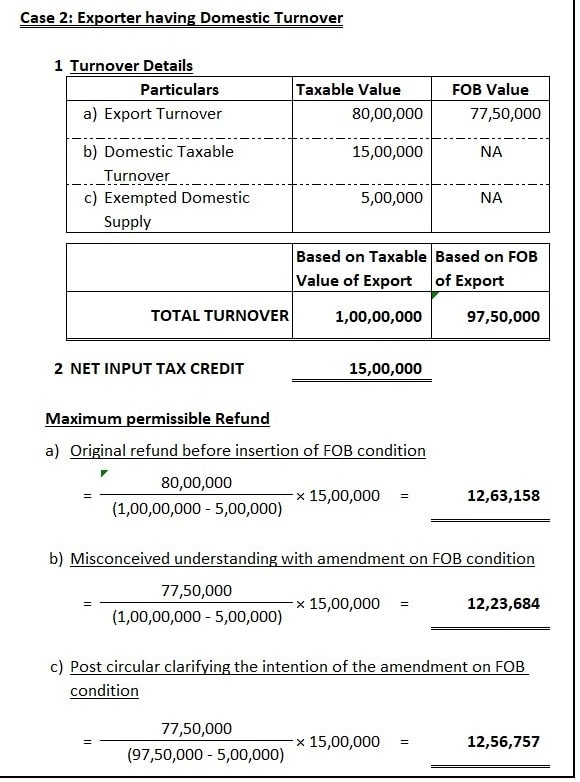

D. LET’S UNDERSTAND WITH AN ILLUSTRATION!

Let us take an example of an Exporter with INR 1 crore as total turnover.

From the above illustration, it can be well understood that the proposed circular would facilitate completely for a 100% exporter and would partially facilitate for an exporter with domestic turnover on a pro-rata basis, irrespective of the impact due to Rule 89(4)(C) restricting exports made without payment of tax to 1.5 times value of like goods supplied domestically! And the intensity of impact would depend upon the proportion of domestic turnover on the total turnover. This undoubtedly creates parity between 100% exporter vis-a-vis an exporter also making domestic turnover merely due to FOB value impact, without a rationale behind. Nevertheless, such issues will have insignificant real impact in business transactions, owing to the utilisation of ITC towards tax liability on domestic supplies.

E. AUTHOR’S NOTE:

It has been made clear in the council recommendation that this is going to be clarified through a CIRCULAR and not through amendment, which indicates that the rule has to be understood and read in this matter from the inception. In such a scenario, it is worth noting that in all cases where a refund has been rejected with an alternate understanding, the matter can be litigated through an appeal procedure citing this circular. Also, wherever appeal has been already preferred on such rejections, this circular would help to resolve and conclude the litigation in a favorable way!

Interestingly, in the light of the aforecited decision of the Hon’ble Karnataka High Court in M/s. Tonbo Imaging India, one of the reasons to declare the impugned offending words, “or the value which is 1.5 times the value of like goods domestically supplied by the same or, similarly placed supplier” appearing in Rule 89(4)(C) as ultra vires the provisions of the CGST Act, is due to the reasonable classification for the purpose of legislation permissible in Article 14 has not passed the twin test of ‘intelligible differentia’ and ‘a rational relation with the object sought to be achieved by the statute’. In setting a differentia between ‘export without payment of tax under LUT’ and ‘export with payment of tax’, it bears no rational nexus with the objective sought to be achieved by Section 16 of the IGST Act seeking to make exports tax-free by “zero-rating” them. In this context, while the larger question of differentiating between ‘export without payment of tax under LUT’ and ‘export with payment of tax’ on various parameters like imposing restriction to the extent of FOB value or the restriction of ITC on capital goods while claiming refund under export without payment of tax, are still remaining unaddressed, this clarification proposed to be issued based on the recommendations of the 50th GST council meeting would at least settle down some ambiguity on the practical application of the formula.

While the press release of the 50th GST Council Meeting in this regard creates hope in resolving the difficulty faced by exporters in this ambiguity on the formula, one has to wait for the circular and the actual wordings of it, before concluding if this really concludes the ambiguity or creates further! Let’s await and look forward to a circular in the true spirit of ‘MEASURE TOWARDS FACILITATION OF TRADE’!

Author Bio

Madam

1) Why Exempt sales are excluded from Denominator, there may be cases where some goods/services are used in exempt sales on which Tax has been paid. 2) in case of local sales Tax Payer has to Pay tax on Local sales then why again added in adjusted total Turnover in Denominator.

Madam, in refund cases of previous years where refund has been partially rejected based on different export turnover value in numerator and denominator of the refund calculation formula for a 100% EOU, can an appeal be made before the GST Appellate Authority for the refund of such rejected ITC with the help of this circular? It has been specifically mentioned in Refund Sanction/Rejection Orders that an appeal can be made only within 3 months from the date of order; in that case is it legally possible to go for an appeal now?

Hello Mr.Ashok! If Appeal time limit is lost, you dont have remedy under amnesty scheme also since refund is not covered. But you can try to apply for differential refund through any other category depending upon the time limit of 2 years for refund, coupled along with covid relief of 2 years. Hope this helps! Should you still have any further doubts, pls feel free to reach me saradha@ggsh.in or mobile 8015014800.