After a round of discussions, finally a notifications in regard to changes suggested by GSTN Council Meetings 33rd and 34th dated 24th Feb 2019 and Mar 19, 2019 respectively has been issued for the real estate sector.The GST Council, on March 19, 2019, approved a transition plan for the implementation of the new tax structure for housing units. As per the plan, builders will be allowed to choose between the old tax rates and the new ones for under-construction residential projects, to help resolve input tax credit (ITC) issues.In meetings, majorly it was held that Real Estate Industry would be brought to subsidized rate of GST without allowing them an option to avail ITC. The Key Changes as indicated by Press notes to these meetings are as follow :-

| 1) | 33rd GST Council Meeting dated 24thFeb, 2019 | |

| A) | GST rate on: | |

| a) Affordable housing properties. * | 1% | |

| b) Residential properties outside affordable * segment; | 5% | |

| *No Input Tax credit is allowed to be setoff against tax liability | ||

| B) | Effective date | from 1st of April, 2019. |

| C) | Definition of affordable housing | |

| a) Non-metropolitan cities/towns | 90 sqm | |

| b) Metropolitan cities | 60 sqm | |

|

||

|

||

| D) | GST exemption on TDR/ JDA, long term lease (premium), FSI: | Intermediate tax shall be exempted only for such residential property on which GST is payable. |

| 2. | Decision taken 34th GST Council Meeting dated 19th March, 2019 | |

| A) | Option in respect of ongoing projects: | |

| a) One Time option :- to continue to pay tax at the old rates on ongoing projects which have not been completed by 31.03.2019. | Condition :

1) where construction and actual booking have both started before 01.04.2019 2) option shall be exercised once within a prescribed time frame and if not opt/exercised new rates shall apply. |

|

| B) | New tax rates: | |

| a) on construction of affordable houses | 1% (without input tax credit ) | |

| b) on construction of houses other than affordable Houses | 5% (without input tax credit ) | |

| c) Commercial apartments such as shops, offices etc In a residential real estate project (RREP) (carpet area of Commercial apartment is not more then 15% of total carpet area of all apartment | 5% (without input tax credit ) | |

| d) For ongoing projects: if opt for new rate:

i) on construction of affordable houses ii) Other than Affordable houses iii) Commercial apartment (in RREP) iv) Commercial apartment (in REP) • In case of houses booked prior to 01.04.2019, new rate shall be available on instalments payable on or after 01.04.2019 |

1%

5% 5% 12% (with input tax credit related to commercial apartment) |

|

| 3) | Conditions for the new tax rates: | |

| i) ITC will not be available.

ii) 80% of inputs and input services (other than capital goods, TDR/ JDA, FSI, long term) shall be purchased from registered persons. On shortfall of purchases from 80%, tax shall be paid by the builder @ 18% on RCM basis. However, Tax on cement purchased from unregistered person shall be paid @ 28% under RCM, and on capital goods under RCM at applicable rates. |

||

| 4) | Transition for ongoing projects opting for the new tax rate: | |

| a) Ongoing Projects:

Transition the ITC as per the prescribed method. b) The transition formula approved by the GST Council, for residential projects (refer to para 4(ii)) extrapolates ITC taken for percentage completion of construction as on 01.04.2019 to arrive at ITC for the entire project. Then based on percentage booking of flats and percentage invoicing, ITC eligibility is determined. Thus, transition would thus be on pro-rata basis based on a simple formula such that credit in proportion to booking of the flat and invoicing done for the booked flat is available subject to a few safeguards |

||

| c) For a mixed project:

Transition shall also allow ITC on pro-rata basis in proportion to carpet area of the commercial portion in the ongoing projects (on which tax will be payable @ 12% with ITC even after 1.4.2019) to the total carpet area of the project. |

||

| 5) | Treatment of TDR/ FSI and Long term lease for projects commencing after 01.04.2019 | |

a) Taxability on same:

|

||

| b) Liability to pay tax:

On Builder under the reverse charge mechanism (RCM) |

||

| c) Taxability Date / Point of Taxation if flat not sold before Completion Certificate:

Builder shall be liable to pay tax on TDR, FSI, long term lease (premium) of land under RCM on the date of issue of completion certificate. |

||

| d) Liability of builder to pay tax on construction of houses given to land owner in a JDA

is also being shifted to the date of completion. |

||

Now, to give effect to the above decisions the following notifications have been issued by CBIC on 29th March, 2019.

| SNo | Notification No. | Remarks |

| 1 | 03/2019- Central Tax (Rate) | Discusses the Rate,Conditions and Modalities of Both Options. (Most Important of All Notification.) |

| 2 | 04/2019- Central Tax (Rate) | For Transfer of Development Rights, FSI, Lease Premium – Exemption |

| 3 | 05/2019- Central Tax (Rate) | For Transfer of Development Rights, FSI, Lease Premium – Conditions of Reverse Charge |

| 4 | 06/2019- Central Tax (Rate) | For Transfer of Development Rights, FSI, Lease Premium – Conditions of Time of Supply |

| 5 | 07/2019- Central Tax (Rate) | Treatment of Short purchases from decided limits (80%) of Registered Dealer Purchaser |

| 6 | 08/2019- Central Tax (Rate) | Prescribing the Rate of GST on Unregistered Dealer Purchases |

| 7 | Notification No. 16/2019 – Central Tax | Central Goods and Services Tax (Second Amendment) Rules, 2019 for ITC Computation in light to Real Estate Changes and Forms for Assessment DRC Forms |

Before, we discuss in depth the Notification 03/2019 CTR and Notification 16/2019 – CT with sample calculations; let’s quickly understand what the other notifications prescribe and how law changes on builders/ real estate developers after 1st April, 2019..

Note:- The notification uses the term Promoter in all the cases. The same shall be referred to as per RERA provisions. For this article the term promoter / builder / developer has been used interchangeably for sake of better understanding.

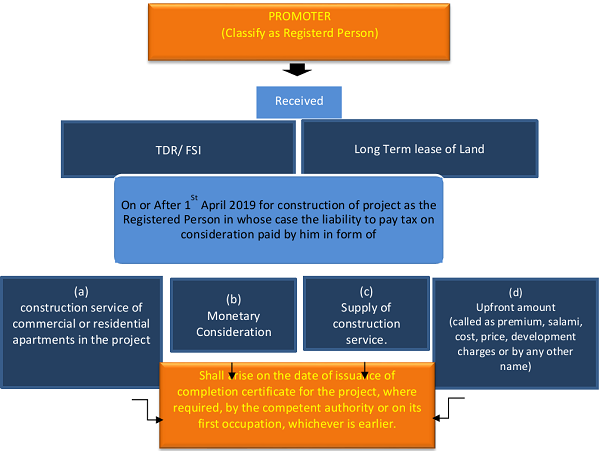

The above said notification basically exempts Transfer of Development Rights (TDR), FSI (including additional FSi),Upfront amount (called as premium, salami, cost, price, development charges or by any other name) payable in respect of service by way of granting of long term lease of thirty years, or more etc in pursuance to Section 11(1) of CGST Act, 2017 where the tax is payable on final output of builder.

| 1) | 41A and 41B (Heading 9972) | ||

| 41A | Service by way of TDR, FSI |

|

|

| 41B | Service by way of long term lease of 30 years or more | ||

| by a promoter in a project, intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier | |||

| a) Amount of Exemption:- | |||

| GST payable on TDR or FSI or both Carpet area of the residential apartments

Or the Upfront amount X in the Project Lease premium) For construction Total carpet area of residential and of the project commercial apartments in the project |

|||

|

|

Provided that :- Taxability if residential unit not sold After CC or OC

The promoter shall be liable to pay tax at the applicable rate, on reverse charge basis, on such proportion of value of TDR, or FSI or both, or Lease premium as is attributable to the residential apartments, which remain unbookedon the date of issuance of completion certificate, or first occupation of the project, as the case may. |

||

| GST payable on TDR or FSI or both Carpet area of the residential apartments in Project Or Upfront amount(Lease premium) Which remain un- booked on the date of For construction of the residential X issuance of completion certificate or first Occupation apartments in the project but for the Total carpet area of residential and commercial exemption contained herein apartments in the project | |||

| Taxable amount/ Rate on unbooked residential apartment for TDR/FSI/LP claimed as exempt:-

For Affordable Housing unit 1% Other Than Affordable housing unit 5% |

|||

| Date of liability of payment of GST on TDR/FSI/LP on portion of unsold unit :-

shall arise on the date of completion or first occupation of the project, as the case may be, whichever is earlier |

|||

| 1A) | Valuation of TDR/ FSI :-

Value of supply of service by way of TDR or FSI by a person to the promoter against consideration in the form of residential or commercial apartments |

shall be deemed to be equal to

the value of similar apartments charged by the promoter from the independent buyers nearest to the date on which such development rights or FSI is transferred to the promoter. |

|

| 1B) | Valuation for portion of unsold unit for TDR/ FSI :

Value of portion of residential or commercial apartments remaining un-booked on the date of issuance of completion certificate or first occupation, as the case may be |

shall be deemed to be equal to the value of similar apartments charged by the promoter nearest to the date of issuance of completion certificate or first occupation, as the case may be. | |

Key Definitions of RERA that have been used in the above Notifications

| Term | Section of RERA | Interpretation of Statute | |

| Apartment | Section 2(e) | “apartment” whether called block, chamber, dwelling unit, flat, | |

| office, showroom, shop, godown, premises, suit, tenement, unit or by any other name, means a separate and self-contained part of any immovable property, including one or more rooms or enclosed spaces, located on one or more floors or any part thereof, in a building or on a plot of land, used or intended to be used for any residential or commercial use such as residence, office, shop, showroom or godown or for carrying on any business, occupation, profession or trade, or for any other type of use ancillary to the purpose specified | |||

| Promoter | Section 2(zk) | (zk) “promoter” means,—

(i) a person who constructs or causes to be constructed an independent building or a building consisting of apartments, or converts an existing building or a part thereof into apartments, for the purpose of selling all or some of the apartments to other persons and includes his assignees; or (ii) a person who develops land into a project, whether or not the person also constructs structures on any of the plots, for the purpose of selling to other persons all or some of the plots in the said project, whether with or without structures thereon;or (iii) any development authority or any other public body in respect of allotteesof— (a) buildings or apartments, as the case may be, constructed by such authority or body on lands owned by them or placed at their disposal by the Government;or (b) plots owned by such authority or body or placed at their disposal by the Government, for the purpose of selling allor some of the apartments or plots;or (iv) an apex State level co-operative housing finance society and a primary co-operative housing society which constructs apartments or buildings for its Members or in respect of the allottees of such apartments or buildings; (v) or any other person who acts himself as a builder, coloniser, contractor, developer, estate developer or by any other name or claims to be acting as the holder of a power of attorney from the owner of the land on which the building or apartmentis constructed or plot is developed for sale; or (vi) such other person who constructs any building or apartment for sale to the general public. Explanation.—For the purposes of this clause, where the person who constructs or converts a building into apartments or develops a plot for sale and the persons who sells apartments or plots are different persons, both of them shall be deemed to be the promoters and shall be jointly liable as such for the functions and responsibilities specified, under this Act or the rules and regulations made there under; |

|

| Either REP or RREP | |||

| Real Estate Project (REP) | Section 2(zn) | “real estate project” means the development of a building or a building consisting of apartments, or converting an existing building or a part thereof into apartments, or the development of land into plots or apartment, as the case may be, for the purpose of selling all or some of the said apartments or plots or building, as the case may be, and includes the common areas, the development works, all improvements and structures thereon, and all easement, rights and appurtenances belonging thereto; | |

| Residential Real Estate Project (RREP) | REP in which the carpet area of the commercial apartments is not more than 15 per cent. of the total carpet area of all the apartments in the REP | ||

| Carpet area | Section 2(k) | “carpet area” means the net usable floor area of an apartment, excluding the area covered by the external walls, areas under services shafts, exclusive balcony or verandah area and exclusive open terrace area, but includes the area covered by the internal partition walls of the apartment. | |

| Floor space

index (FSI)” |

the ratio of a building’s total floor area (gross floor area) to the size of the piece of land upon which it is built. | ||

| An apartment booked on or before the date of issuance of completion certificate or first occupation of the project | ALL CONDITIONS MUST MEET

(a) part of supply of construction of the apartment servicehas time of supply on or before the said date;and (b) consideration equal to at least one installment has been credited to the bank account of the registered person on or before the said date;and (c) an allotment letter or sale agreement or any other similar document evidencing booking of the apartment has been issued on or before the said date. |

||

Notification 05/2019 CTR: Service to be taxed under RCM – Liabilty cast – on Promoter

This notification simply casts the reverse charge mechanism on Promoter (Builder / Developer) in case of TDR / FSI / Upfront Long term lease premium of 30yrs or more in any case of service provider. So in all cases where the service provider is Any person (Individual , HUF or Body corporate) the liability to pay tax is on the Promoter.

Notification No. 06/2019-Central Tax (Rate):-Notify certain class of persons & prescribe Point of Taxation

he Liability casted on the Builder Promoter to pay under reverse charge on TDR/FSI / Upfront Long Term lease premium has been made to arise on the date of issuance of completion certificate for the project, where required, by the competent authority or on its first occupation, whichever is earlier

In a nutshell, this notification prescribes Point of Taxation in these transactions as stated in brief below:

Notifies the following classes of registered persons, namely:-

Notification No. 07/2019-Central Tax (Rate) :- RCM Compliances If Services or Purchase Procure is shortfall or Less Then 80% from registered dealer For Those Who Opting Scheme of 1% / 5% GST Rate

This notification state about Reverse Charge Compliance on the Promoter ands have to pay tax on reverse charge basis as recipient of such goods or services or both if the porchase or service taken are less then 80% from Registered Dealer, namely:-

a) Any Supply of goods and service or both received from Unregistered Suppliers such that in a FY shortfall is below 80% would be Promoter Liability to Pay under ReverseCharge.

b) Cement falling in chapter heading 2523 in the first schedule to the Customs Tariff Act, 1975 (51 of 1975) which constitute the shortfall from the minimum value of goods or services or bothrequired to be purchased by a promoter for construction of project, in a financialyear

c) Capital goods falling under any chapter in the first schedule to the Customs Tariff Act, 1975 (51 of 1975) – This is worth Attention also, all the capital goods have been brought in reversecharge irrespective of ceiling or any prescribedlimit.

Notification No. 08/2019-Central Tax (Rate): Rate Prescribe @ 18% as RCM on services or purchase from Unregistered Dealer

This Notification has prescribed the rate of Reverse Charge @ 18% for all cases of Reverse charge liability except cement and capital Goods.

| 1) Affordable Residential Apartment:

A) Carpet Area: area not exceeding 60 square meter in metropolitan cities or 90 square meter in cities or towns other than metropolitan cities B) Gross Amount Charged Not more Than Rs 45 lakhs |

| 2) In REP projects :

On commercial units the Rate is 12% and on same the proportionate credit of Input Tax is allowed. 3) Output liability must be paid in Cash and not via Input tax credit. 4) No Input tax credit should be taken except as per calculations discussion below (Annexure 1 for REP & Annexure II for RREP) 5) Input Tax Credit not availed shall be reported every month by reporting the same as Ineligible credit in GSTR-3B [Row No. 4 (D)(2)]. 6) Projectwise segregation of Accounts: The promoter shall maintain project wise account of inward supplies from registered and unregistered supplier and calculate tax payments on the shortfall at the end of the financial year and shall submit the same in the prescribed form electronically on the common portal by end of the quarter following the financial year. The tax liability on the shortfall of inward supplies from unregistered person so determined shall be added to his output tax liability in the month not later than the month of June following the end of the financial year. 7) An apartment booked on or before the 31st March, 2019 shall mean an apartment which meets all the following three conditions, namely (a) part of supply of construction of which has time of supply on or before the 31st March, 2019 and (b) at least one instalment has been credited to the bank account of the registered person on or before the 31st March, 2019 and (c) an allotment letter or sale agreement or any other similar document evidencing booking of the apartment has been issued on or before the 31st March, 2019;” |

Calculation of ITC in Several Cases – Simplified Analysis

Where project is REP i.e. Non RREP and it has commercial and builder is under 1%/5% for residential (To be Done beforeSep’19)

a. On 31.3.2019 % Completion > 0% { Tx =T-Te}

Tx@ITC to be reversed on 1.4.2019

T Total ITC of Input and Input Services (not capital Goods) availed bw 1.7.2017 to 31.3.2019 including TRAN-1 Credit

TeCredit Pertaining to Commercial and Time of Supply of Residential prior to 1.4.2019

(ELIGIBLE ITC)

b. On 31.3.2019 % Completion is 0% but Invoice done and no Input service received { Te = Tc + Tr}

TrEligible ITC on Residential for TOS <= 31.3.2019

TcEligible ITC on Commercial

Te Total Eligible Credit allowed to be carried forward

B) In case of RREP, in the effectively commercial to be treated as Residential

Note:- The Calculations of Tx, Te, Tr, Tc and others has to be on the basis of excel sheet computation based on multiple factors like % Completion PUCM, Carpet Area Sold Ratio, Demand (POS) Ratio to arrive at final Figure.

3 Exceptions to above rule :-

a) If % Demand > % Completion by 25% then % Invoicing to be deemed % Completion +25%

b) Demand upto 31.3.2019 > Receipts by 25% then % Invoicing with Value = Receipts +25%

c) Value of Input/Input Service received > Actual Consumption by 25% – Commissioner toprescribe method with CACertificate

Rate of Works Contract Reduced

Rate of Works Contract Reduced to 12% on Works Contractors supplying services to Builders on following conditions :-

a) The Project must have atleast 50% carpet area of affordable residentialapartments.

b) Value of the apartments shall be the value of similar apartments booked nearest to the date of signing of the contract for supply of the service and must be 45 Lacs or Less.

c) If during or after CC/OC condition (a) not met even if (b) met, promoter developer will be liable to pay differential tax under reverse charge.

Concluding remarks:

For Ongoing Projects:

Projects which are nearby on completion phase as on 31.3.2019 should workout before taking any decision relate to Opt with the Old regime or can go with the new scheme of 1% or 5%. As it would have more eligible ITC even under 5% regime and can go for 5% with substantial ITC carry forward if it has in its Cenvat Ledger depending upon the Booking and completion percentage. Hence whether one choose 5% or 12% for Ongoing Project is to be done very logically as a lot of tax can either be saved or vice versa.

If you have any queries regarding the provision, or working in relation to opting new scheme or any queries regarding RERA, can mail us or contact :

Author can be reach at amiitj@gmail.com. Mob: 9821923411

Wonderfully explained. Nice.

Mr. Amit, Please clarify the GST applicable on a flat booked in Sept. 2017, who’s OC was received in May 2019 and thereafter possession letter in June 2019. Builder has calculated GST @ 12% on total cost of the flat and 18% on EDC/IDC and services. As per our calculation GST of 12% should be on 2/3 value of the total cost of the flat (as 1/3 is considered as land value, which we are not going to pay). Am I right ? Please correct me.

Thanks a lot Amit. The information is very useful and presented really well. Really appreciate your efforts in explaining every point in detail and putting together all information at one place

presentation of the topics excellent however upto which date builders/promoters can exercise option not clear