45th GST COUNCIL MEETING TO BE HELD ON 17TH SEPTEMBER 2021

The 45th meeting of the GST Council is scheduled to be held on 17th September 2021 at Lucknow, Uttar Pradesh under the chairpersonship of Hon’ble Finance Minister Smt. Nirmala Sitharaman. The GST council would be holding physical meeting after a gap of 16 months. The council had last met physically on 14th March 2020 at New Delhi. The Council met for the 37th meeting at Goa on 20th September 2019, for the 23rd meeting at Guwahati, Assam on 10th November 2017 and for the 10th meeting at Udaipur, Rajasthan on 18th February 2017.

GST REVENUE FOR AUGUST 2021

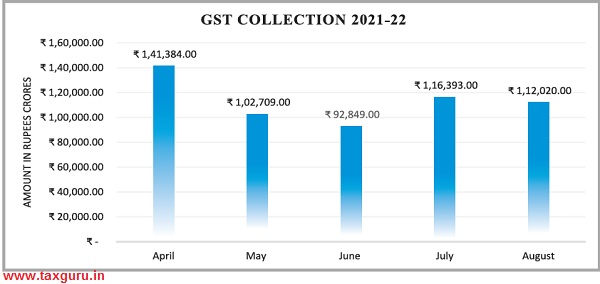

Rs. 1,12,020 crore of gross GST revenue collected in August 2021

The gross GST revenue collected in the month of August 2021 was Rs. 1,12,020 crore of which CGST was Rs. 20,522 crore, SGST was Rs. 26,605 crore, IGST was Rs. 56,247 crore (including Rs. 26,884 crore collected on import of goods) and Cess was Rs. 8,646 crore (including Rs. 646 crore collected on import of goods).

The government has settled 23,043 crore to CGST and Rs. 19,139 crore to SGST from IGST as regular settlement. In addition, Centre has also settled Rs. 24,000 crore as IGST ad-hoc settlement in the ratio of 50:50 between Centre and States/UTs. The total revenue of Centre and the States after regular and ad-hoc settlements in the month of August’ 2021 is Rs. 55,565 crore for CGST and Rs. 57,744 crore for the SGST.

The revenues for the month of August 2021 are 30% higher than the GST revenues in the same month last year. During the month, the revenues from domestic transaction (including import of services) are 27% higher than the revenues from these sources during the same month last year. Even as compared to the August revenues in 2019-20 of Rs. 98,202 crore, this is a growth of 14%.

GST collection, after posting above Rs. 1 lakh crore mark for nine months in a row, dropped below Rs. 1 lakh crore in June 2021 due to the second wave of covid. With the easing out of COVID restrictions, GST collection for July and August 2021 have again crossed Rs. 1 lakh crore, which clearly indicates that the economy is recovering at a fast pace. Coupled with economic growth, anti-evasion activities, especially action against entities generating fake invoices have also been contributing to the enhanced GST collections. The robust GST revenues are likely to continue in the coming months too.

NOTIFICATIONS & CIRCULARS

- Notification extending timelines for filing of application for Revocation of Cancellation of Registration vide Notification No. 34/2021-Central Tax dated 29.08.2021

The Government has notified that the timelines for filing of application for revocation of cancellation of registration has been extended to 30.09.2021, where due date for filing such application falls between 01.03.2020 to 31.08.2021. The extension would be applicable only in those cases where registration has been cancelled under clause (b) or clause (c) of section 29(2) of the CGST Act.

- Notification with regards to extension of FORM GSTR-3B late fee Amnesty Scheme vide Notification No. 33/2021-Central Tax dated 29.08.2021.

The Government, vide Notification No. 19/2021- Central Tax, dated 01.06.2021, had earlier provided relief to the taxpayers by introducing an amnesty scheme with regards to late fee for non-furnishing FORM GSTR-3B for the tax periods from July, 2017 to April, 2021, provided that returns for these tax periods are furnished between 01.06.2021 to 31.08.2021. It is pertinent to mention that with the abovementioned notification the government extended the last date to avail benefit of the late fee amnesty scheme from existing 31.08.2021 to 30.11.2021.

- Notification with respect to Seventh Amendment (2021) to CGST Rules, 2017 Notification No. 32/2021-Central Tax dated 29.08.2021.

The Government with the said notification has extended the facility of filing of FORM GSTR-3B and FORM GSTR-1/ IFF by companies using electronic verification code (EVC), instead of Digital Signature certificate (DSC) which has already been enabled for the period from 27.04.2021 to 31.08. 2021.It is pertinent to note that this facility has been further extended to 31st October, 2021..

GST PORTAL UPDATES

- Advisory for Taxpayers regarding Blocking of E-Way Bill (EWB) generation facility resume after 15th August, 2021.

1. The E Way Bill generation facility of a person is liable to be restricted, in case the person fails to file their return in Form GSTR-3B (Monthly /Quarterly) / statement in CMP-08, for a two or more consecutive tax periods, in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017. As you may be aware, the facility of blocking E way bill generation has been temporarily suspended due to pandemic.

2. The government has now decided to resume the blocking of EWB generation facility on the EWB portal, for all the taxpayers in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017, after 15th August onwards.

3. Thus, after 15th August 2021, the System will check the status of returns filed in Form GSTR-3B or the statements filed in Form GST CMP-08, and block the generation of EWB in cases of:

Non-filing of two or more returns in Form GSTR-3B (Monthly/Quarterly frequency as may be applicable) for the tax periods up to June, 2021 and Non-filing of 02 or more statements in Form GST CMP-08 for the quarters up to April to June, 20214.

4. To avail continuous EWB generation facility on EWB Portal, you are therefore advised to file your pending Form GSTR 3B (Monthly/Quarterly frequency as may be applicable) Returns/ Form GST CMP-08 Statements immediately.

5. For more details on blocking and unblocking of EWB generation facility, click on below links

https://tutorial.gst.gov.in/userguide/returns/index.htm#t=FAQs_unblo ckingewaybill.htm

- Updating the Annual Aggregate Turnover (AATO) by taxpayers.

The Annual Aggregate Turnover (AATO) has been calculated based on the returns filed by the taxpayers. The detailed advisory on calculation methodology of AATO has been specified under the ‘Advisory’ hosted at Taxpayers’ Dashboard. A functionality has been provided at the Common Portal to modify the AATO where taxpayers have reason to believe that the AATO has been calculated wrongly. In such cases, taxpayers may modify the Annual Aggregate Turnover (AATO). In case such modification is made beyond a certain limit (as specified in the ‘Advisory’), the same shall be sent to the jurisdictional officer’s Dashboard for appropriate action, if required. However, it has been seen that many taxpayers have used the functionality to modify AATO just for confirming it, which is not required. In case, the AATO is correct in their opinion, they are not required to take any action.

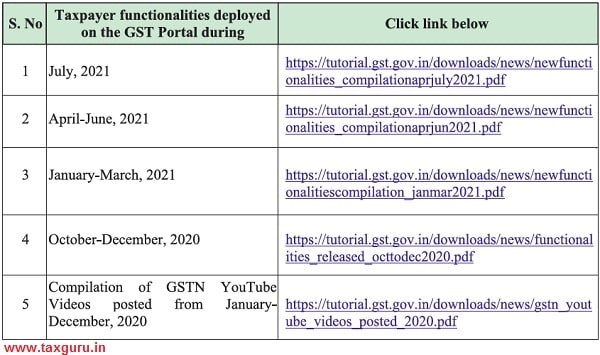

- Module wise new functionalities deployed on the GST Portal for taxpayers

Various new functionalities are implemented on the GST Portal, from time to time, for GST stakeholders. These functionalities pertain to different modules such as Registration, Returns, Advance Ruling, Payment, Refund and other miscellaneous topics. Various webinars are also conducted as well informational videos prepared on these functionalities and posted on GSTNs dedicated YouTube channel for the benefit of the stakeholders.

To view module wise functionalities deployed on the GST Portal and webinars conducted/ Videos posted on our YouTube channel, refer to table below:

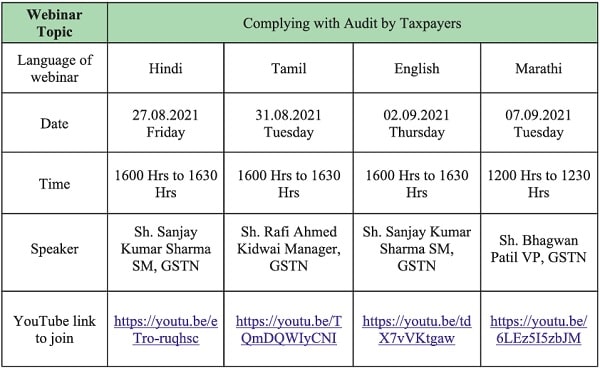

- Webinars on ‘Complying with Audit by Taxpayers’

GSTN has recently implemented Audit functionality. For creating awareness amongst all the stakeholders, GSTN is holding webinars, as per details given below:

- Implementation of Rule-59(6) on GST Portal.

1. Rule-59(6) of CGST Rules, 2017; inserted vide Notification No. 1/2021 dated 1st January 2021, provides for restriction in filing of GSTR-1 in certain cases:

a) a registered person shall not be allowed to furnish the details of outward supplies of goods or services or both under section 37 in FORM GSTR-1, if he has not furnished the return in FORM GSTR-3B for preceding two months;

b) a registered person, required to furnish return for every quarter under the proviso to sub-section (1) of section 39, shall not be allowed to furnish the details of outward supplies of goods or services or both under section 37 in FORM GSTR-1 or using the invoice furnishing facility, if he has not furnished the return in FORM GSTR-3Bfor preceding tax period;

GST PORTAL UPDATES

2. This Rule will be implemented on GST Portal from 1st September, 2021.

On implementation of the said Rule, the system will check that whether before the filing of GSTR-1/IFF of a tax-period, the following has been filed or not:

a) GSTR-3B for the previous two monthly tax-periods (for monthly filers),

b) GSTR-3B for the previous quarterly tax period (for quarterly filers), as the case may be. The system will restrict filing of GSTR-1/IFF till Rule59(6) is complied with.

3. This check will operate on clicking the SUBMIT button of GSTR-1 and the system will give an error message if the condition of Rule-59(6) is not met. It may be noted that records which have been saved in GSTR-1 will remain saved and filing of such records will be permitted after Rule-59(6) is complied with.

4. Implementation of Rule-59(6) on the GST Portal will be completely automated, similar to the blocking & un-blocking of e-way bill as per Rule138E and facility for filing of GSTR-1 will be restored immediately after filing of relevant GSTR-3B. No separate approval would be needed from the tax-officer to restore the facility for filing of GSTR-1.

5. To ensure no disruption in filing GSTR-1/IFF, taxpayers who have not filed their pending GSTR-3B, especially from period November 2020 and afterwards may do so at the earliest.

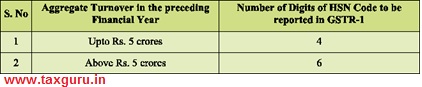

- Advisory on HSN and GSTR-1 Filing

1. In accordance with Notification No. 78/2020 – Central Tax, dated October 15, 2020, taxpayers need to declare Harmonized System of Nomenclature (HSN) Code of Goods and Services supplied by them on raising of tax invoices, with effect from 1st April 2021 on the below

mentioned lines.

2. It has been reported by few taxpayers that HSN used by them for reporting in GSTR-1 is not available in the table 12 HSN drop-down. They have further stated that they are facing issues in adding the required HSN details in table -12 and filing of statement of outward supplies in form GSTR-1 of July 2021. Further, in some JSON files, the HSN field is coming as blank from the offline tool, along with other errors as mentioned below: –

- Processed with Error, In Progress or Received but pending.

- Duplicate Invoice Number found in payload please correct.

3. To view the detailed advisory on the action to be taken by the taxpayers to resolve above issues, click on:

https://tutorial.gst.gov.in/downloads/news/advisoryonhsnandgstr1.pdf

HARYANA BECOMES MODEL 2 STATE

The State of Haryana has been a pioneer in implementing and adopting tax reforms. It was the first State to implement the VAT Act in 2003. In continuation to its legacy of adopting new and better systems, the State recently decided to switch to Model-2 mode of implementation of GST. The process of transition to the new system has been completed and all officers are now working on the BO-WEB portal developed by GSTN.

The successful transition to the new system was inaugurated by the Hon’ble Deputy Chief Minister, Sh. Dushyant Chautala in Haryana Niwas. It was shared with the Hon’ble Minister, that the new system is more updated, faster and has better data quality than the erstwhile system. It was also observed that few of the functionalities that were not available in the Model system are now available to officers in Model-2 systems. Apart from that the new system provides for intelligence tools such as BIFA and 360-degree taxpayer analysis etc.

The Deputy Chief Minister, Haryana also announced that the State is already at advanced stages of procurement of State-of-the-Art hardware for all its officers. ‘The State believes that only if we provide the best software and hardware to our officers, we will be able to provide the best axpayer services.

– Excise and Taxation Department, Haryana

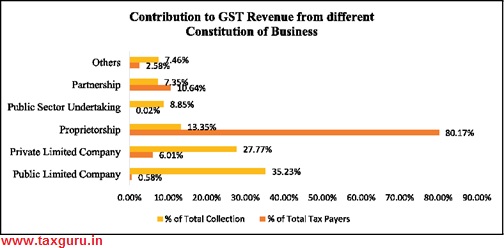

STATISTICAL REPORT ON COMPLETION OF 4 YEARS OF GST

Source : A Statistical Report on Completion of 4 years of GST by GSTN

Note :

- Status as on 1st July 2021; Return period accounted up to March 2021.

- Figures representative of the liability paid by debit made in the Electronic Cash Ledger doesn’t include IGST on imports).

- Others include Govt. Dept., Society/ Club/ Trust/ AOP, LLP, Statutory Body, Foreign Companies, etc.

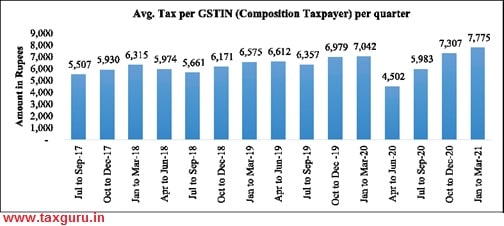

Source : A Statistical Report on Completion of 4 years of GST by GSTN

Note : Average tax payment in cash above is based on those GSTINs who have filed returns and that’s too non-nil returns.

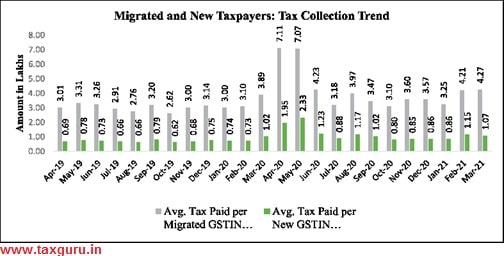

Source: A Statistical Report on Completion of 4 years of GST by GSTN.

Note : The number of Taxpayers above is of those who paid cash i.e., it does not include those who filed NIL return or paid full Liability by Input tax credit. Report Published by GSTN.

******

DISCLAIMER: This newsletter is in-house efforts of the GST Council Secretariat. The contents of this newsletter do not represent the views of GST Council and are for reference purpose only.

Printed & Published by – GST COUNCIL SECRETARIAT | 5th Floor, Tower-II, Jeevan Bharati Building, Connaught Place, |New Delhi 110 001, Ph: 011-23762656, www.gstcouncil.gov.in