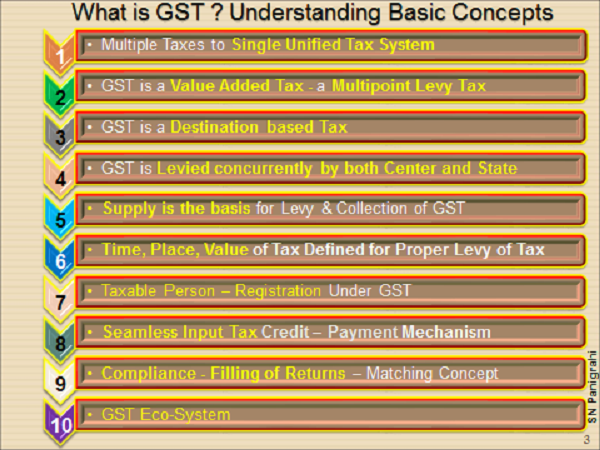

Brief Introduction on GST

Goods and Services Tax (GST) is a Value Added, Multi-Point, Destination Based, Dual Taxation System aim to eliminate Double Taxation / Cascading Effect of several indirect taxes like VAT, CST, Central Excise Duty, Service Tax etc. It is actually a culmination multiple taxes (17 Taxes & 23 Cesses of earlier tax system) to a Unified Tax System. It is fondly described as One Nation, One Tax & One Market – a major Indirect Tax Reform in India.

Supply is the basis for taxation with Time, Place and Values are defined to levy and collect tax. Person who’s turnover crosses Rs 20 Lakhs (Rs 10 Lakhs in case of Special Category states) need to Register and such person become Taxable Person. GST shall facilitate Seamless Credit across the entire supply chain under a common tax base. Periodic filling of Returns and certain Tax Compliance procedures are prescribed for all taxable persons. GST Eco-system is a wide spread Network encompasses central and state governments, taxpayers and other stakeholders

It is expected to result into Ease of Doing Business; Simplified Tax Collection System & Expand Tax Base; Total Digitalization; Transparency in Tax System; Improved Efficiency & Productivity in Supply Chain; Resulting in Business Growth; More Efficient Neutralization of Taxes; Bring about a Macroeconomic Dividend.

Supply Chain & it’s Functions:

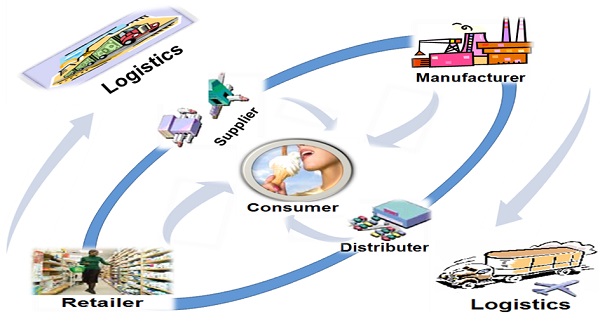

Sourcing, Procurement, Logistics and Supply Management fall under the supply-chain umbrella. Forecasting, production planning and scheduling, order processing, and customer service all are part of the process as well. Activities such as inbound and outbound transportation, warehousing, and inventory control are covered in logistics. The management of all these functions refers to Supply Chain Management.

Supply Chain Management (SCM) can be defined as management of the supply chain as an integrated process of acquisition and management of flow of supply of inputs from point of origin to point of consumption and delivering further value added output to the next level point of consumption (like from supplier to manufacturer to wholesaler to retailer and to final consumer) by balancing supply and demand with optimal management of resources with the objective of establishing relationships for maximising value for mutual benefits on economically, socially and environmentally sustainable basis.

(As defined by the Author in his Article “Value Insights into Supply Chain” Published in Aug’2010 issue of MMR – IIMM)

Supply Chain creates value of Profitable Growth, Working Capital Reduction, Fixed Capital Efficiency, Tax Minimization, Cost Optimization etc through proper strategic choices of Network Design, Warehousing Locations, Sourcing & Vendor Selection, Efficient Negotiations, Asset Management etc.

Supply Chain creates value of Profitable Growth, Working Capital Reduction, Fixed Capital Efficiency, Tax Minimization, Cost Optimization etc through proper strategic choices of Network Design, Warehousing Locations, Sourcing & Vendor Selection, Efficient Negotiations, Asset Management etc.

GST Relevance to Supply Chain & Business Impact:

GST impact can be seen in both inbound and outbound transactions – entire supply chain process, cost of acquisitions, location of facilities, marketing, product pricing, logistics, cash flows, accounting, IT system etc and strategies for these are expected to undergo drastic changes. Areas of Supply Chain to be impacted by GST are Tax Impact, Sourcing / Procurement & Logistic Decisions, Impact on Sales & Distribution, Warehousing Decisions, Manufacturing Facilities & Processes, Impact on Finance, Costs, Budgets & Working Capital, Compliance & Risk Assessment, Change Mgt – Advocacy Assessment, IT Upgradation & Transitional arrangements etc.

Therefore, companies should revisit supply chain strategies; redesigning supply chain networks; redefining sourcing & procurement strategies; manufacturing & locational strategies; re-look into distribution & warehousing strategies etc. to gain benefits from GST implementation.

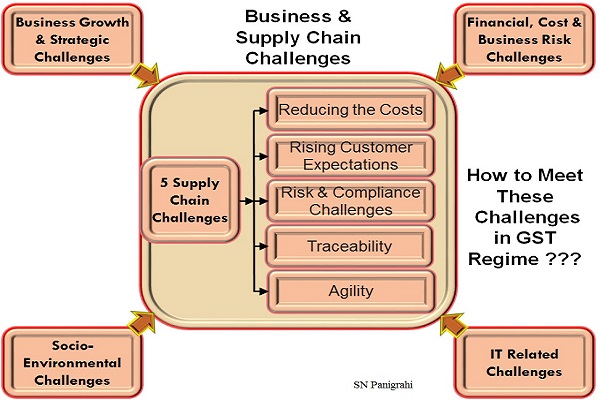

Supply Chain Challenges in GST Regime :

In every business broadly there are Four Challenges – Business Growth & Strategic Challenges for Development & Sustainability of Business; Finance & Cost related Challenges including Business Risks; Socio-Environmental Challenges & Technology related Challenges. Operating within overall business related challenges, within supply chain there are some challenges like Reducing Costs, Raising Customer Expectations, Supply Risks & Compliance Challenges, Traceability and Agility (Responses).

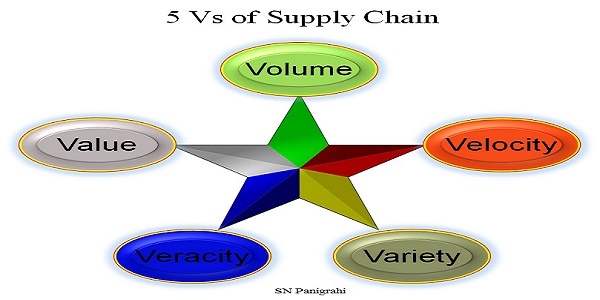

The above supply chain challenges may in other words be described with 5Vs – Value (Customer Value / Satisfaction, Value Addition to Business, Costs); Volume (Business Volume (Finance), Product / Transaction Volumes, Asset Volumes (Warehousing / Stores)); Velocity (Speed of Delivery, Response time, agility); Variety (Product Variety, Transaction Variety, Customer Variety, Preferential Variety, Varying Capacity); Veracity (Authenticity, Traceability, Transaction Evidence)

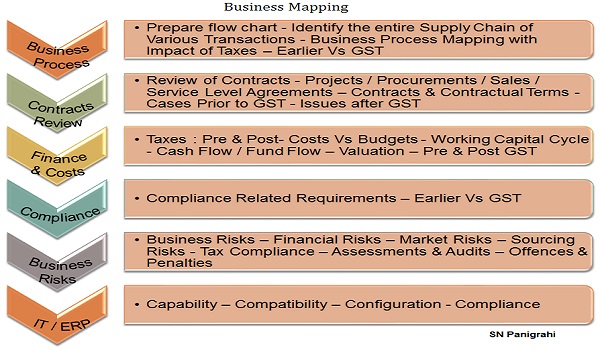

Business & Supply Chain Mapping

This is the first and fundamental step in creating a visibility by juxtaposing current & proposed various aspects of business processes, functions, transactions, capacities etc thereby to find gaps and requirements, value assessments, waste elimination and apply lean principles and develop strategies.

Along with the above reviews also shall be made for contracts review, review of finance & costs, compliances, business risks, IT & other technological assessments. These shall made for pre- GST and post- GST scenarios.

Supply Chain Re-alignment in view of GST

Now industry can leverage the impact of GST. Post-GST the supply chain can be designed purely on sourcing competitiveness, benefits of economies of scale, operational efficiency, logistic cost and customer service considerations and may not compromise on tax effectiveness because of uniform tax structure in place unlike earler multiple taxes of different nature and rate at multiple points. The supply chain strategy in future should look into opportunities to rationalize supply network, redefining sourcing & procurement strategies, redesign manufacturing & locational strategies, re-engineering distribution channels & consolidation of warehousing strategy to derive logistic efficiencies and to reduce levels of inventory holding, strategies to improve service levels required by the customers and achieving responsiveness & speed by taking advantage of uniform tax structure across the country.

Shift to Fewer Facilities:

With the implementation of GST, companies would no longer be required to have warehouses in every state just to facilitate stock transfers and avoid indirect taxes (CST @ 2%). With GST in place, India will become a common market without any difference between interstate or intrastate sales. GST (CGST & SGST) on intra state transactions shall be equal to IGST levied on interstate transaction irrespective of the nature of supply – either sales or stock transfer, thus eliminating the need to operate multiple warehouses across the country in different states. The key advantage for companies will be re- engineering of their business operations to leverage efficiencies of scale, locations, warehouses and routes. GST regime may lead to merging of small and scattered warehouses to one or few larger centralized warehouses clustered in certain parts of the country specifically around consumer centric metropolises.

Leveraging Logistical Efficiency:

Large Centralized Warehouses will be able to attain benefits through improved productivity, centralization of resources, congregation of allied and multidimensionality, better space utilization, adoption of technological sophistication by using state-of-the-art planning and warehouse management systems which are not feasible and used in smaller and scattered warehouses. All these results into revised distribution strategies that lead to minimization of the operating cost of multiple warehouses and reduced transport lead to Increase in responsiveness, faster and better services to the customers. Inventory holding costs also expected to come down.

Transfer of Goods within same GSTIN (GST Identification Number – Registration Number) will not be charged to GST. That is company / entity having operations with in the same state and comes under same business vertical can operate under one GSTIN and therefore need not pay tax while transferring goods / services from one unit to the other of same GSTIN. However in case of any transfer of goods or services between units operating in different states or operating under different business verticals have to pay GST as they need to take different GSTINs

Leveraging Total Supply Chain Lead Times :

With Supply Chain Realignment and re-engineering post-GST, transportation routes may change, vendor location and base may vary, purchasing decisions, lot sizes etc may alter leading requirement of re-calculation of EOQ / Lead Times, Inventory Holdings etc ultimately resulting in improved supply chain performance.

According to nature of industry, location, supply base, purchasing plans and decisions may change. Lead times, EOQ levels, inventory holdings may change. Budgets, cash out flows need to be changed based on impact. Contracts and credit terms also need to be changed. Based on delivery terms (INCOTERMS) the impact of GST on freight forwarding, ocean transport for import shall be worked out.

Leveraging Sourcing / Procurement Decisions:

Post GST scenario may enable Competitive Sourcing as Tax Efficient decisions vanish. Right Vendor Selection is very essential in the new tax regime considering cost and compliance requirements. Dealing with non-compliant vendors should be avoided. The risk of dealing with such vendors is on the buyer as the onus of paying taxes with interest lies with the buyer if the vendor is not made payment of taxes. Vendor performance rating system is available in the proposed GST electronic platform to track vendor compliances in respect of payment of taxes and filling of returns.

In the GST regime small businesses and vendors have to compete with large business houses as tax based advantage or differentiation will go off. Area based tax exemptions may not continue for long. Tax incentives / exemptions by state or central government also may not sustain. That is vendor specific or location specific tax advantages may not exist. In view of the above vendor selection criteria also may change.

Pricing and promotional strategies may change under GST regime. Supply chain and manufacturing strategic alterations may offer to trade-off between customer serviceability and cost associated. With uniform taxation, marketing forecast process may improve. Pricing need to rework based on costs associated with manufacturing, supply chain and new tax structure. Discount strategies may go off as any discounts extended post sales transaction also being captured and adjusted for GST.

Even the existing contracts may be reopened and prices renegotiated. New collaborative associations may be forged taking advantage of re-arrangement of warehousing and supply network. However cost estimation and cost structuring need to be done to gain an advantage of post GST regime. Since the GST impact can’t be generalized with specific activity / function wise transaction mapping and proper sensitivity analysis may be made with various permutations with a range to understand roughly the impact of GST.

Re-Design Business Models :

GST Complimented business blue print shall be prepared considering seamless integration, sales and distribution network, business risk assessment, shareholder profit maximization. This is over all company level broad exercise to leverage benefits of post GST advantage.

Profound Impact on Cash Flow and Working Capital:

Though it can’t be generalised, the GST will impact all types businesses especially in respect of cash flow and working capital requirements. Even though seamless input credit is available in the entire value chain, some sectors are impacted positively and others negatively and accordingly they need to re-evaluate their working capital requirements and make budgets.

Leverage Technology – IT Enabled GST Transformation :

GST is the single biggest driver for the adoption of technology in the tax space in India. Tax automation will lead the way for corporations to be compliant with the dynamic nature of the new tax regime and derive maximum benefit from it.

With implementation of GST, organizations face newer challenges such as alignment of accounting and taxation systems with the new processes, they will need to embrace IT into the entire workflow. GST can provide a major fillip and competitive advantage through creation of transparent and totally digitalized business environment as technology is at the heart of GST. Businesses need to have a reasonable IT infrastructure in place in terms of business process reinforcement, tax configuration, input credit setoff, tax impact assessment & accounting, inventory data storage, document numbering, data amendments, impact analysis on interfaces, reversal of open transactions, many other dynamic changes and so on to align with GST. The proposed e-way bill for moving goods within the country and employing RFID chips and QR codes for containerized cargo movement for exports would rely heavily on high technology interface.

Supply Chain Operational Efficiency – Leveraging GST Complimented Cost Advantage

As discussed above Post-GST possible cost and other strategic, operational and transactional benefits let us summarize these as Improved Lead Times, Reduced Asset Holdings, Consolidation of Facilities, Rationalization of Vendor Base, Shift to Revamped Distribution Channel, Scale Driven Warehousing & Logistics etc.

Though initial hiccups, hitches and hardships are being experiencing, these will be addressed through improvements and course corrections with consensus looking at long term benefit to industry, business, common man and to the nation at large and we may expect GST may bring real transformation to the country.

This is the Extract of Part of the Paper Presented at NATCOM’2017, Annual Convention of IIMM, Bengaluru.

(Author can be reached at snpanigrahi@rediffmail.com or on Mobile : 9515762045)

Author Bio