GST Revenue Collection For January, 2022

Rs 1,38,394 crore Gross GST Revenue collected for January 2022

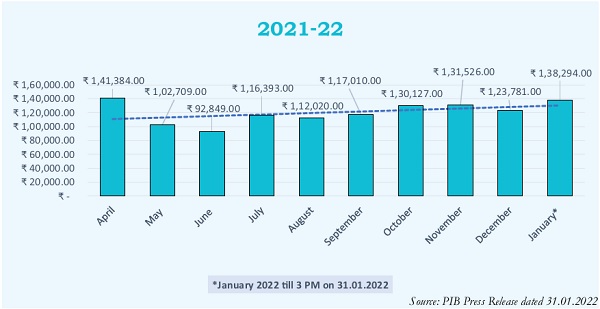

The gross GST revenue collected in the month of January 2022 till 3:00 PM on 31.01.2022 is Rs 1,38,394 crore of which CGST is Rs 24,674 crore, SGST is Rs 32,016 crore, IGST is Rs 72,030 crore (including Rs 35,181 crore collected on import of goods) and cess is Rs 9,674 crore (including Rs 517 crore collected on import of goods). The highest monthly GST collection has been Rs 1,39,708 crore in the month of April 2021. Total number of GSTR-3B returns filed upto 30th January, 2022 is 1.05 crore that includes 36 lakh quarterly returns.

The government has settled Rs 29,726 crore to CGST and Rs 24,180 crore to SGST from IGST as regular settlement. In addition, Centre has also settled Rs. 35,000 crore of IGST on ad-hoc basis in the ratio of 50:50 between Centre and States/UTs in this month. The total revenue of Centre and the States in the month of January 2022 after regular and ad-hoc settlements is Rs 71,900 crore for CGST and Rs 73,696 crore for the SGST. Centre also released GST compensation Rs 18,000 crore in January, 2022 to States/UTs.

The revenues for the month of January, 2022 are 15% higher than the GST revenues in the same month last year and 25% higher than the GST revenues in January, 2020. During the month, revenues from import of goods was 26% higher and the revenues from domestic transaction (including import of services) are 12% higher than the revenues from these sources during the same month last year.

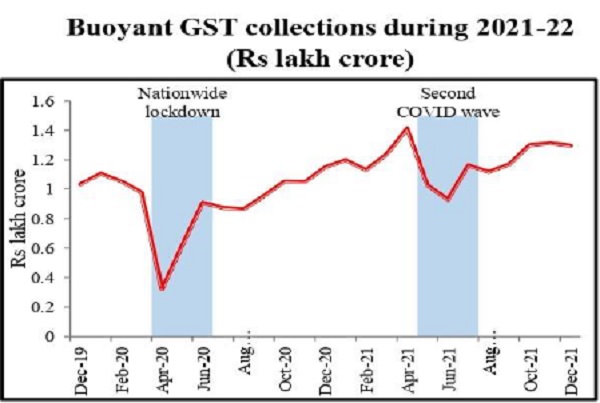

This is for the fourth time GST collection has crossed Rs 1.30 lakh crore mark. 6.7 crore e-way bills were generated in the month of December, 2021 which is 14% higher than 5.8 crore e-way bills generated in the month of November 2021. Coupled with economic recovery, anti-evasion activities, especially action against fake billers have been contributing to the enhanced GST. The improvement in revenue has also been due to various rate rationalization measures undertaken by the Council to correct inverted duty structure. It is expected that the positive trend in the revenues will continue in the coming months as well.

UNION BUDGET 2022-2023 : HIGHLIGHTS

The Hon’ble Finance Minister in her Budget address has said that India is celebrating Azadi ka Amrit Mahotsav and it has entered into Amrit Kaal, the 25-year-long leadup to India @ 100, the government aims to attain the vision of the Prime Minister, outlined in his Independence Day address and they are:

- Complementing the macro-economic level growth focus with a micro-economic level all-inclusive welfare focus,

- Promoting digital economy & fintech, technology enabled development, energy transition, and climate action, and

- Relying on virtuous cycle starting from private investment with public capital investment helping to crowd-in private investment.

The Finance Minister informed that since 2014, the government’s focus has been on empowerment of citizens, especially the poor and the marginalized. Moreover, measures have been taken to provide housing, electricity, cooking gas, and access to water. The government also have programmes for ensuring financial inclusion, direct benefit transfers and a commitment to strengthen the abilities of poor to tap all opportunities.

Smt Nirmala Sitharaman has emphasized that this Budget continues to provide impetus for growth. It lays a parallel track of (1) a blueprint for the Amrit Kaal, which is futuristic and inclusive, which will directly benefit our youth, women, farmers, the Scheduled Castes and the Scheduled Tribes. And (2) big public investment for modern infrastructure, readying for India at 100 and this shall be guided by PM GatiShakti and be benefited by the synergy of multi-modal approach. Moving forward, on this parallel track, she has outlined the following four priorities:

- PM GatiShakti

- Inclusive Development

- Productivity Enhancement & Investment, Sunrise Opportunities, Energy Transition, and Climate Action

- Financing of Investments

On the Indirect tax side, the Union budget says that Customs administration in Special Economic Zones will be fully IT driven. It provides for phasing out of concessional rates in capital goods and project imports gradually and apply a moderate tariff of 7.5%. The budget underlines review of customs exemptions and tariff simplification, with more than 350 exemptions proposed to be gradually phased out. It proposes that customs duty rates will be calibrated to provide a graded structure to facilitate domestic electronics manufacturing. Rationalization of exemptions on implements and tools for agri sector manufactured in India will be undertaken. Customs duty exemption to steel scrap will be extended. Unblended fuel will attract additional differential excise duty.

The budget proposes a new provision permitting taxpayers to file an Updated Return on payment of additional tax. This updated return can be filed within two years from the end of the relevant assessment year. Smt. Sitharaman said that with this proposal, there will be a trust reposed in the taxpayers that will enable the assessee to declare the income that they may have missed out earlier while filing their return. It is an affirmative step in the direction of voluntary tax compliance.

To provide a level playing field between co-operative societies and companies, the budget proposes to reduce Alternate Minimum Tax for the cooperative societies also to fifteen percent.

The Finance Minister also proposed to reduce the surcharge on cooperative societies from present 12 to 7 per cent for those having total income of more than Rs 1 crore and up to Rs 10 crores.

Eligible start-ups established before 31.3.2022 have been provided a tax incentive for three consecutive years out of ten years from incorporation. In view of the Covid pandemic, the budget provides for extending the period of incorporation of the eligible start-up by one more year, that is, up to 31.03.2023 for providing such tax incentive.

In an effort to establish a globally competitive business environment for certain domestic companies, a concessional tax regime of 15 per cent tax was introduced by the government for newly incorporated domestic manufacturing companies. The Union Budget proposes to extend the last date for commencement of manufacturing or production under section 115BAB by one year i.e. to 31st March, 2024.

For the taxation of virtual / digital assets, the budget provides that any income from transfer of any virtual digital asset shall be taxed at the rate of 30 per cent. No deduction in respect of any expenditure or allowance shall be allowed while computing such income except cost of acquisition. Further, loss from transfer of virtual digital asset cannot be set off against any other income. In order to capture the transaction details, a provision has been made for TDS on payment made in relation to transfer of virtual digital asset at the rate of 1 per cent of such consideration above a monetary threshold. Gift of virtual digital asset is also proposed to be taxed in the hands of the recipient.

Taking forward the policy of sound litigation management, the budget provides that, if a question of law in the case of an assessee is identical to a question of law which is pending in appeal before the jurisdictional High Court or the Supreme Court in any case, the filing of further appeal in the case of this assessee by the department shall be deferred till such question of law is decided by the jurisdictional High Court or the Supreme Court.

> Tax Proposals

- Allowing taxpayers to file Updated Return within 2 years for correcting errors.

- Tax relief to persons with disability.

- Reducing Alternate Minimum Tax Rate and Surcharge for Cooperatives.

- Increasing tax deduction limit on employer’s contribution to NPS account of state government employees.

- Extending period of incorporation of eligible start-ups for providing tax incentives.

- Income from transfer of virtual assets to be taxed at 30%.

- Better litigation management to avoid repetitive appeals.

- Customs administration to be fully IT driven in SEZs.

- Phasing out concessional rates in capital goods and project imports gradually and apply a moderate tariff of 7.5%.

- Review of customs exemptions and tariff simplification.

- Customs duty rates are being calibrated to provide a graded rate structure to facilitate domestic electronics manufacturing.

- Rationalisation of exemptions on implements and tools for agri sector manufactured in India.

- Extension of customs duty exemption to steel scrap.

- Reduction of duty on certain inputs required for shrimp aquaculture.

- Unblended fuel shall attract additional differential excise duty.

PRESS RELEASE

Finance Minister Smt. Nirmala Sitharaman authorises release of

advance installment of tax devolution to State Governments

amounting to Rs. 47,541 crore.

Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman has authorised the release of an advance installment of tax devolution to State Governments amounting to Rs. 47,541 crore on 20.02.22. This is in addition to the regular devolution for the month of January 2022.

Thus, States would receive a total of Rs. 95,082 crore or double their respective entitlement during the month of January 2022. State-wise breakup of the amounts being released is appended.

It is pertinent to mention that the Government of India had released the first advance instalment of tax devolution amounting to Rs. 47,541 crore to States on 22nd November 2021. With the release of the second advance installment, the States would have received an additional amount of Rs. 90,082 crore under tax devolution over and above what has been budgeted to be released till January, 2022.

It also needs to be noted that release from Government of India of the back-to-back loan amounting to Rs. 1.59 lakh crore to State Governments in lieu of GST Compensation shortfall in FY 2021-22 was completed by the end of October 2021.

This is in line with the commitment of Government of India to strengthen the hands of States to accelerate their capital and developmental expenditure to ameliorate the deleterious effects of CoVID-19 pandemic.

| STATEMENT SHOWING STATEWISE DISTRIBUTION OF NET PROCEEDS OF UNION TAXES AND DUTIES FOR JANUARY 2022 |

||||

| Sl. No. | State | Regular monthly installment for Jan 2022 |

Advance installment in Jan 2022 |

Total releases in Jan 2022 |

| 1 | Andhra Pradesh | 1,923.98 | 1,923.98 | 3,847.96 |

| 2 | Arunachal Pradesh | 835.29 | 835.29 | 1,670.58 |

| 3 | Assam | 1,487.08 | 1,487.08 | 2,974.16 |

| 4 | Bihar | 4,781.65 | 4,781.65 | 9,563.30 |

| 5 | Chhattisgarh | 1,619.77 | 1,619.77 | 3,239.54 |

| 6 | ||||

| 7 | Gujarat | 1,653.47 | 1,653.47 | 3,306.94 |

| 8 | ||||

| 9 | Himachal Pradesh | 394.58 | 394.58 | 789.16 |

| 10 | ||||

| 11 | Karnataka | 1,733.81 | 1,733.81 | 3,467.62 |

| 12 | ||||

| 13 | Madhya Pradesh | 3,731.96 | 3,731.96 | 7,463.92 |

| 14 | ||||

| 15 | Manipur | 340.40 | 340.40 | 680.80 |

| 16 | ||||

| 17 | Mizoram | 237.71 | 237.71 | 475.42 |

| 18 | ||||

| 19 | Odisha | 2,152.66 | 2,152.66 | 4,305.32 |

| 20 | ||||

| 21 | Rajasthan | 2,864.82 | 2,864.82 | 5,729.64 |

| 22 | ||||

| 23 | Tamil Nadu | 1,939.19 | 1,939.19 | 3,878.38 |

| 24 | ||||

| 25 | Tripura | 336.66 | 336.66 | 673.32 |

| 26 | ||||

| 27 | Uttarakhand | 531.51 | 531.51 | 1,063.02 |

| 28 | ||||

| TOTAL | 47,541.00 | 47,541.00 | 95,082.00 | |

Source: PIB Press Release dated 20.01.2022

GST PORTAL UPDATES

> Deployment Of Interest Calculator In Gstr-3b

1. The new functionality of interest calculator in GSTR-3B is now live on the GST Portal.

2. This functionality will facilitate & assist the taxpayers in doing self-assessment. This functionality will arrive at the system computed interest on the basis of the tax liability values declared by the taxpayers, along with the details about the period to which it pertains. The interest applicable, if any, will be computed after the filing of the said GSTR-3B and will be auto-populated in the Table-5.1 of the GSTR-3B of the next tax-period. The facility would be similar to the collection of Late fees for GSTR-3B, filed after the Due date, posted in the next period’s GSTR-3B. This functionality will inform the taxpayers about the manner of system computed interest for each tax-head and hence will assist the taxpayers in doing correct computation of interest for the tax liability of any past period declared in the GSTR-3B for the current tax period.

3. For more details, please refer to the detailed advisory regarding the functionality, click here

4. For seeing an illustration of interest computation in GSTR-3B by the system with sample values & screenshots, click here

5. This functionality will further improve ease of filing return under GST and is, therefore, in the direction of further reducing the compliance burden for taxpayers.

Portal updated on 26.01.2022

> Advisory On Revamped Search Hsn Code Functionality

The Search HSN functionality was earlier given as a measure of facilitation to the taxpayer to search the Technical Description of any particular HSN code of any goods and/or service used in the Trade, vis-à-vis HSN description in the Customs Tariff Act, 1975. However, there are many instances of goods and services where descriptions commonly used in Trade in common parlance i.e. Trade description differ from the Technical descriptions otherwise provided in the HSN descriptions of the Customs Tariff Act, 1975 and the above said functionality. Thus finding the corresponding HSN codes vis a vis a common description was a bit challenging for the taxpayer. (Note: Technical descriptions imply those descriptions which pertain to each and every HSN Code while Trade descriptions imply those descriptions which are used in common parlance by the trade/ businesses for various goods and services.)

To ameliorate this challenge and to make the functionality user friendly, ‘Search HSN’ functionality has been revamped by linking it with e-invoice database and Artificial Intelligence tools.

A revamped & enhanced version of Search HSN Functionality has been launched on the GST Portal.

Please Click here for details.

Source: PIB Press Release dated 20.01.2022

Portal updated on 06.01.2022

> Module wise new functionalities deployed on the GST Portal for taxpayers

Various new functionalities are implemented on the GST Portal, from time to time, for GST stakeholders. These functionalities pertain to different modules such as Registration, Returns, Advance Ruling, Payment, Refund and other miscellaneous topics. Various webinars are also conducted as well informational videos prepared on these functionalities and posted on GSTNs dedicated YouTube channel for the benefit of the stakeholders.

To view module wise functionalities deployed on the GST Portal and webinars conducted/ Videos posted on our YouTube channel, refer to table below:

| Sl. No | Taxpayer functionalities deployed on the GST Portal during |

Click link below |

| 1. | December, 2021 | https://tutorial.gst.gov.in/downloads/n ews/new_functionalities_compilation_d ecember_2021.pdf |

| 2. | November, 2021 | https://tutorial.gst.gov.in/downloads/ news/new_functionalities_compilation_ november_2021.pdf |

| 3. | July – September, 2021 | https://tutorial.gst.gov.in/downloads/ news/new_functionalities_compilation_ july_september_2021.pdf |

| 4. | April – June, 2021 | https://tutorial.gst.gov.in/downloads/ news/newfunctionalities_compilationa prjun2021.pdf |

| 5. | January – March, 2021 | https://tutorial.gst.gov.in/downloads/ news/newfunctionalitiescompilation_ janmar2021.pdf |

| 6. | October – December, 2020 | https://tutorial.gst.gov.in/downloads/ news/functionalities_released_octtodec 2020.pdf |

| 7. | Compilation of GSTN YouTube Videos posted from January- December, 2020 |

https://tutorial.gst.gov.in/downloads/ news/gstn_youtube_videos_posted_ 2020.pdf |

Portal updated on 05.01.2022

> Reporting of supplies notified under section 9(5) / 5(5) by E-commerce Operator in GSTR-3B

1. As per the GST Council decision to notify “Restaurant Service” under section 9(5) of the CGST Act, 2017 along with other services notified earlier such as motor cabs, accommodation and housekeeping services wherein the tax on such supplies would be paid by electronic commerce operator if such supplies made through it, Notification No. 17/2021- Central Tax (Rate) and 17/2021-Integrated Tax (Rate) dated 18.11.2021 have been issued. Accordingly, the tax on supplies of restaurant service supplied through e-commerce operators, shall be paid by the e-commerce operator with effect from the 1st January, 2022.

2. In light of the above, E-commerce operator and registered person would report taxable supplies notified under section 9(5) of CGST Act, 2017 and similar provisions in IGST/SGST/UTGST Act in the following manner.

| Supplies reported by | Reporting in Form GSTR-3B |

| Supplies under 9(5) reported by ECO | Table 3.1(a) of GSTR–3B |

| Registered person/Restaurant supplying through ECO | Table 3.1(c) along-with nil and exempted supply |

For more details, please refer to CBIC Circular No. 167/23/2021 dated 17.12.2021.

Portal updated on 04.01.2022

> Implementation of Rule-59(6), as amended, on GST Portal

1. As per Notification No. 35/2021 – Central Tax dated 24th September 2021, clause (a) of the sub-rule (6) of Rule 59 of CGST Rules, 2017 was amended. By way of this amendment, for the words “for preceding two months”, the words “for the preceding month” were substituted with effect from 1st January 2022. This means that from 1st January 2022 onwards, if a monthly filer has not filed the GSTR-3B for the preceding month, then such taxpayer will not be allowed to file the GSTR-1 for the subsequent month, till the GSTR-3B for the preceding month is filed.

2. This functionality will be implemented on the GST Portal shortly, after

which the system will check the filing of preceding GSTR-3B before permitting to file GSTR-1 for the subsequent month.

Illustration:

A taxpayer has not filed the monthly GSTR-3B for November 2021. Now, the taxpayer tries to file GSTR-1 for December 2021 on 10th January 2022. The system will not allow filing of GSTR-1 for December 2021, and will allow filing of GSTR-1 for December 2021 only after the filing of GSTR-3B for November 2021.

3. Taxpayers may kindly ensure timely filing of GSTR-1 and GSTR-3B in consonance with Rule 59 of CGST Rules, 2017 to avoid any inconvenience in this regard.

Portal updated on 03.01.2022

*****

Published by GST COUNCIL SECRETARIAT, 5th Floor, Tower-II, Jeevan Bharati Building, Connaught Place, New Delhi 110 001, Ph: 011-23762656, www.gstcouncil.gov.in

DISCLAIMER: This newsletter is in-house efforts of the GST Council Secretariat. The contents of this newsletter do not represent the views of GST Council and are for reference purpose only.

Ok