Government Infra Projects Contractors are caught between the Devil and Deep Sea in GST Platform

Indian real estate is expected to jump over fivefold to USD 650 billion by 2040 and its share in the country’s Gross Domestic Product (GDP) is set to double from the current seven percent.

– Niti Ayog Vice Chairman Rajiv Kumar (22.02.2019)

Real estate sector plays pivotal role in The Nation Building process of any economy in the world due to its spill over effects viz.. it promotes employment, infrastructure, and quality of life of the society. That’s why China has adopted One Belt One Road foreign policy to address slow growth of its economy. Our Indian Government has also taken series of measures to boost real estate sector such as priority sector lending to real estate sector, RERA, Bharath Mala project, Sagar Mala project, Pradhan Mantri Awas Yojana, Pradhan Mantri Krishi Sinchayee Yojana etc.,

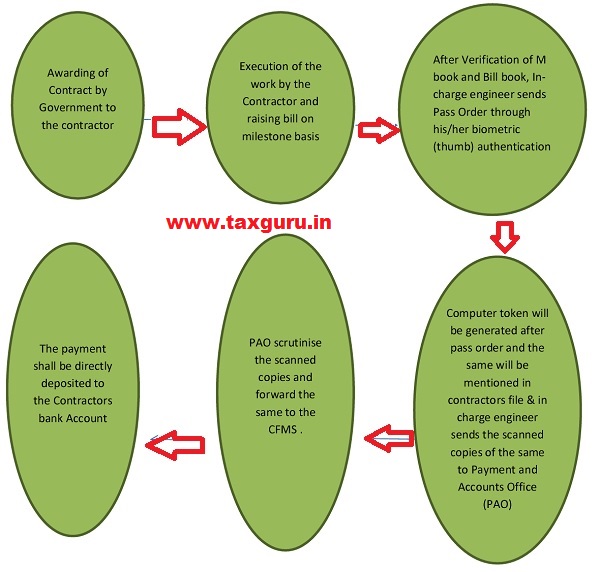

The aforesaid projects are taking at brisk pace across the country promoting growth of real estate sector. For execution of these projects the State Governments have adopted different financial management modules. For example Andhra Pradesh Government adopted Comprehensive Financial Management System (CFMS). It is worthwhile to understand the mode of payment to Government Contractors under CFMS which is presented as under:

It is pertinent to note that the in charge Engineer cannot send pass order through his/her biometric if there are no sufficient funds in his/her designated operating account. For example if incharge engineer has Rs.50 lakhs in his login account he cannot send pass order to the contractor payments beyond Rs.50 lakhs through his account unless and until fresh amount is replenished. So without pass order, there will be no computer token/ processing of payment by PAO office and delivery of payment to the contractor.

Without estimating the available amount, the Government is awarding contracts to get political mileage. This results in fiscal indiscipline and thereby jeopardise contractors interest in GST platform.

During service tax regime; most of the Government Infrastructure projects were exempt from service tax (refer Sl.no 12 to 14A of Mega Exemption Notification 25/2012). However, in GST regime majority of the Government infra works contracts falling under the ambit of GST and thereby they are required to comply with provisions of the GST law.

As per Section 13 of CGST Act, the time of supply of service is the triggering point for levy of Tax. It also indicates when supply is deemed to have been made. The Government Contractors are liable to discharge GST in the month of supply.

As discussed, due to irregular or delayed payments by Government departments, Government Contractors are constrained to delay the payment of GST due to working capital stress. This would result in levy of interest, penalty and denial of Input Tax Credit.

Recently Telangana High Court in the case of M/s. Megha Engineering & Infrastructures Ltd (W.P No 44517 of 2018 delivered on 18-04-2019) has categorically stated that when there is delay in payment of GST, the dealer is liable to pay interest on total tax gross liability under Section 50 of the CGST Act notwithstanding the benefit of eligible Input Tax Credit. Resultantly the dealers are also liable to pay interest on ITC portion as well.

For example, Mr. Abhiram Reddy for the tax period July 2017 has rendered works contract service to Pollavaram project in Andhra Pradesh. For the said work he is having eligible ITC of Rs.50,00,000/-. The output tax liability for the said project amounts to be Rs.60,00,000/-. The net tax liability that needs to be discharged in cash amounts to be Rs.10,00,000/- (Rs.60,00,000-Rs.50,00,000/-).

The total contract amount was received by him in the month of March 2019 wherein GST liability of the said contract was discharged by him in March 2019 GST Return due to delay in receipt of payments from the Government.

In light of the above judgement, Mr.Abhiram Reddy is liable to pay interest @ 18% on total tax liability i.e. Rs.60,00,000/- from due date of filing i.e. July 2017 return to actual payment of GST liability in March 2019 return. Though he is having eligible ITC of Rs.50,00,000/- the same would not come to his rescue as filing of GSTR 3B is a prerequisite for availing and apportioning ITC against output tax liability in terms of Section of 41 read with Section 49(2) of CGST Act.

| Particulars | Output liability | Due date of payment of GST | Actual payment of GST | Delay in number of days | Interest liability |

| Execution of works contract service | 60,00,000/- | 20.08.2017 | 20.04.2019 | 608 | 17,99,014/- |

The above example explains the gravity of the problem faced by Government Contractors where for Rs.10,00,000/- net liability he is slapped with interest liability of Rs.17,99,014/- for no fault of him that too due to delay of payment by the Government itself. The paradox is the Government enjoys its share of cake in form of SGST/CGST/IGST as the case may be through one window and enjoys free credit of working capital by delay of payments to poor contractors.

This scenario can be applied Pan India where there are huge outstanding dues for works executed to Government. On an average the payments are being delayed for six months to one year putting pressure on the cash flows of the contractors.

Look at the following news paper clipping on burning problems of delays in Government contracts bills dues.

Many State Governments, without looking into their financial purses are awarding various construction projects to the Government contractors wherein the work executed but payment was kept in abeyance. Further Government Contractors were also forced to undertake Government projects in order to engage their workers and to avoid their machinery idleness.

In light of the above judgment and practical problems faced by the contractors, there is a need to relook into the provisions of CGST Act and suitably amend Section 50 to incorporate net liability rather than Gross liability for calculation of interest such amendment should be on retrospective basis which gives great solace to the aggrieved party. Further all the persons from the Government side should also be made accountable and responsible for creating this impasse, otherwise it hampers ease of doing business and delay in Nation building process.

(The author of the article can reached at prudhvitadepalli@gmail.com)

Very good article by CA Prudhvi