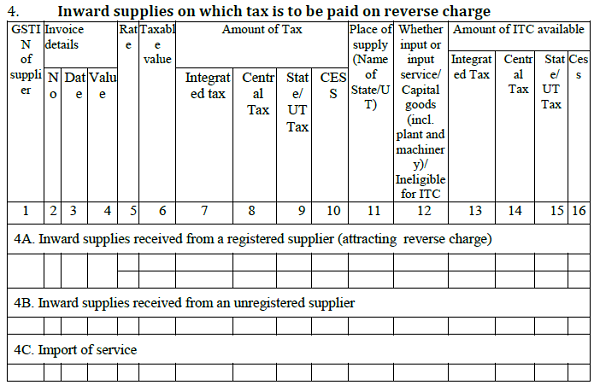

Q 1: Paid GST Tax as RCM on Foreign Company invoices. Kindly let us know where we need to show invoice wise details in GSTR2 Return ?

Ans: In table 4 of FORM GSTR-2 –

4A. Under this head, all purchases on which reverse charge specifically applies by law must be mentioned. For example, purchasing cashew nuts from an agriculturist.

4B. This head will list the purchases from unregistered dealer which exceed Rs. 5,000 per day from an unregistered dealer

4C. Under this head, reverse charge GST paid on import of service will be reported.

Q 2: If a dealer does not charge GST in bill in UP where to complain ?

Ans: Please inform the jurisdictional Division office. Notification No. 2/2017-Central Tax dated 28.06.2017 may be referred to.

Q 3: Which section declares GST paid on ‘deemed export’ as eligible for refund? …… can’t be 54. Please advise

Ans: Refund on deemed exports becomes eligible under section 54 of CGST Act read with rule 89 of the CGST Rules.

Q 4: What is the impact for freelancer (export of services), payment receiving through paypal or upwork into local bank transfer??

Ans: For qualifying as export of service, all conditions under section 2 (6) of the IGST Act must be satisfied that is, consideration must be received in foreign convertible currency. If not, it is an inter-state supply on which IGST must be paid.

Extract of Section 2(6) of Integrated Goods and Services Tax Act, 2017 is as follows :-

2(6) “export of services” means the supply of any service when,––

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service in convertible foreign exchange; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8;

Extract of Explanation 1 in section 8 of Integrated Goods and Services Tax Act, 2017 is as follows :

Explanation 1.––For the purposes of this Act, where a person has,––

(i) an establishment in India and any other establishment outside India;

(ii) an establishment in a State or Union territory and any other establishment outside that State or Union territory; or

(iii) an establishment in a State or Union territory and any other establishment being a business vertical registered within that State or Union territory,

then such establishments shall be treated as establishments of distinct persons.

Q 5: Late fees for GSTR 1,2 & 3 for July, Aug & Sept has also been waived?? Or 3B Late fees only waived?

Ans: Late fee for delayed filing of FORM GSTR-3B and GST TRAN-1 only has been waived so far.

ITC-04 due date extension 3 Hour before the expiry of time to file

FORM GST TRAN – 1 due date extended to 30th November 2017

Q 6: What is Effective date of notification no 38/2017 Central tax (Rate) for suspension of RCM ?

Ans: 13th October, 2017