Place of Supply of Goods

GST is a destination based tax, i.e., the goods/services will be taxed at the place where they are consumed and not at the origin. So, the state where they are consumed will have the right to collect GST.

This, in turn, makes the concept of place of supply crucial under GST as all the provisions of GST revolves around it.

Place of supply of goods under GST defines whether the transaction will be counted as intra-state or inter-state, and accordingly levy of SGST, CGST & IGST will be determined.

Browse by topics:

- Movement of goods

- No movement of goods

- Goods supplied on a vessel/conveyance

- Imports & exports

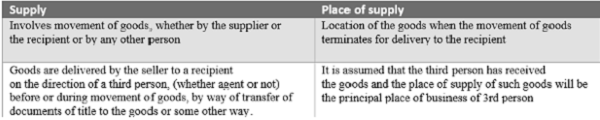

Place of Supply When There is Movement of Goods

Example 1- Intra-state sales

Mr. Raj of Mumbai, Maharashtra sells 10 TV sets to Mr. Vijay of Nagpur, Maharashtra

The place of supply is Nagpur in Maharashtra. Since it is the same state CGST & SGST will be charged.

Example 2-Inter-State sales

Mr. Raj of Mumbai, Maharashtra sells 30 TV sets to Mr. Vinod of Bangalore, Karnataka

The place of supply is Bangalore in Karnataka. Since it is a different state IGST will be charged.

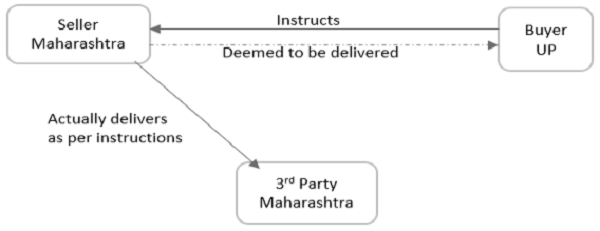

Example 3- Deliver to a 3rd party as per instructions

Anand in Lucknow buys goods from Mr. Raj in Mumbai (Maharashtra). The buyer requests the seller to send the goods to Nagpur (Maharashtra)

In this case, it will be assumed that the buyer in Lucknow has received the goods & IGST will be charged.

Place of supply: Lucknow (UP)

GST: IGST

Example 4- Receiver takes the goods ex-factory

Mr. Raj of Mumbai, Maharashtra gets an order of 100 TV sets from Sales Heaven Ltd. of Chennai, Tamil Nadu. Sales Heaven mentions that it will arrange its own transportation and take TV sets from Mr. Raj ex-factory

Place of supply: Chennai, Tamil Nadu

GST: IGST

Although the goods are received ex-factory i.e in Maharashtra by the recipient, the movement of the goods terminates for delivery to the recipient only at Chennai, Tamil Nadu. Irrespective of whether the supplier or the recipient is actually undertaking the movement of goods, the place of supply is the location of goods where movement of goods terminates for delivery to the recipient which is at Chennai. Hence, IGST is applicable.

Example 5 – E-commerce sale

Mr. Raj of Mumbai, Maharashtra orders a mobile from Amazon to be delivered to his mother in Lucknow (UP) as a gift. M/s ABC (online seller registered in Gujarat) processes the order and sends the mobile accordingly and Mr. Raj is billed by Amazon.

Similar to example 3, it will be assumed that the buyer in Mumbai has received the goods & IGST will be charged.

Place of supply: Mumbai, Maharashtra

GST: IGST

No Movement of Goods

Example 1- No movement of goods

Sales Heaven Ltd. (Chennai) opens a new showroom in Bangalore. It purchases a building for showroom from ABC Realtors (Bangalore) along with pre-installed workstations

Place of supply: Bangalore

GST: CGST& SGST

There is no movement of goods (work stations), so the place of supply will be the location of such goods at the time of delivery (handing over) to the receiver.

Note: There is no GST on purchase of building or part thereof. RENT of commercial space attracts GST

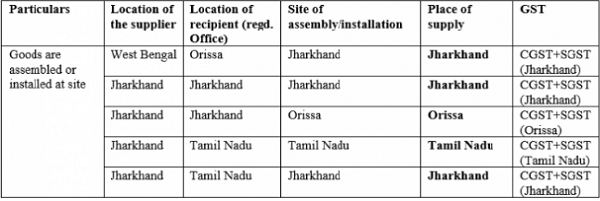

Example 2- Installing goods

Strong Iron & Steel Ltd. (Jharkhand) asks M/s SAAS Constructions (West Bengal) to build a blast furnace in their Jharkhand steel plant

Place of supply: Jharkhand

GST: CGST & SGST

Although M/s SAAS is in West Bengal, the goods (blast furnace) is being installed at site in Jharkhand which will be the place of supply.

Note: M/s SAAS will have to be registered in Jharkhand to take up this contract. They can opt to register as a casual taxable person which will be valid for 90 days (extendable by 90 days more, on basis of a reasonable cause).

Goods Supplied on a Vessel/Conveyance

Example 1- Plane

Mr. Ajay is travelling from Mumbai to Delhi by air. He purchases coffee and snacks while on the plane. The airlines is registered in both Mumbai and Delhi.

Place of supply: Mumbai

GST: CGST& SGST

The food items were loaded into the plane at Mumbai. So, place of supply becomes Mumbai.

Example 2- Plane- Business travel

Mr. Ajay is travelling from Mumbai to Chennai by air on behalf of his company Ram Gopal and Sons (registered in Bangalore). In the plane he purchases lunch. The airlines is registered in Mumbai & Chennai.

Place of supply: Mumbai

GST: CGST & SGST

The food items were loaded into the plane at Mumbai. So, place of supply becomes Mumbai. It does not matter where the buyer is registered.

In most cases CGST & SGST is charged because most airlines have a pan-India presence and will be registered in all states.

Example 3- Train

Mr. Vinod is travelling to Mumbai via train. The train starts at Delhi and stops at certain stations before Mumbai. Vinod boards the train at Vadodara (Gujarat) and promptly purchases lunch on board. The lunch had been boarded in Delhi.

Place of supply: Delhi

GST: CGST & UTGST

The food items were loaded into the train at Delhi. So, place of supply becomes Delhi.

CGST & SGST is charged because Indian railways has a pan-India presence and will be registered in all states. It does not matter where the buyer is registered.

Imports & Exports

The place of supply of goods:

- imported into India will be the location of the importer.

- exported from India shall be the location outside India.

Example 1- Import

Ms. Malini imports school bags from China for her shop (registered in Mumbai)

Place of supply: Mumbai

GST: IGST

Example 2- Export

Ms. Anita (Kolkata) exports Indian perfumes to UK

Place of supply: Kolkata

GST: Exempted

Very useful information. thank you.,

What about in case of hotel room

Explained place of supply rule in a simple and understanding language with proper example,chart. Thank you very much.

Overall very beautiful article. However in last example POS should be UK instead of Kolkata.

Mr.Junaid

it is very informative – thanks for it

I have a doubt my querry is this

webhosting charges – The co . is in Kerala paid for webhosting charges – ( import ) to Japan for their website situated in Japan

can you explain in this case where is the place of supply ?