Introduction: Recent modifications to the GSTR-1 form on the GST Portal have sparked concerns among taxpayers and legal consultants. The alterations, particularly in the descriptions of Table 11A and 11B, raise questions about the accuracy of reporting refund vouchers and the potential implications for users.

On GST Portal, one may refer to the GSTR-1 form. First, one should check the PDF of GSTR-1 downloaded from the portal at the time of filing GSTR-1 of Q-1 FY 2023-24 (which must have been downloaded at the time of filing that form. i.e. by 11.07.2023 / 13.07.2023). Now see the description against Table No. 11A(1), 11A(2) as well description against Table No. 11B(1), 11B(2) and you will find it as shown in the following screenshot.

Here you can see that the refund of payments received (refund voucher amounts) are to be shown in Table 11A and not in Table 11B.

Now if you again download the same Q-1 (or any other quarter also) FY 2023-24 GSTR-1 PDF from the GST Portal at present, you will find a very serious change in it as under in the description of Table 11A and Table 11B as under.

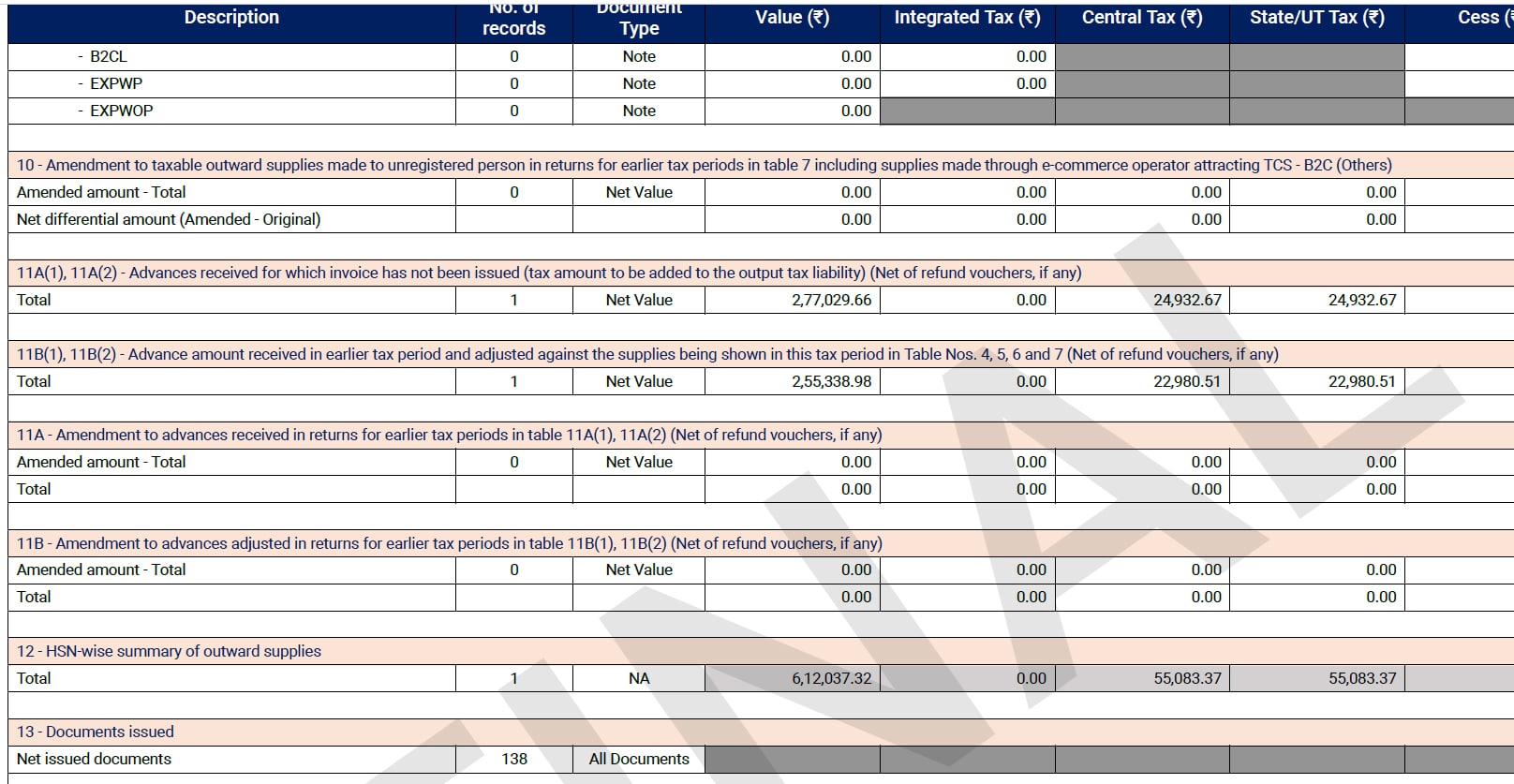

GSTR-1 – Table 11A and Table 11B

So,

Now you can note that the wording in brackets “Net of Refund Vouchers” are getting reflected in descriptions of both Table No. 11A and 11B!!!!! Following are the questions which arises in the mind of a Taxpayers and Legal Consultants against this change.

1. Where is the official notification of this change in the Form GSTR-1?

2. How can there be a liberty to the GST Portal Operators to make such changes themselves?

3. Does it mean that the Return Filers has a liberty to show the amount of refund vouchers at their choice either against Table 11A or against Table 11B or to put the partial amounts in both the tables?

4. When it is written very clearly in Table 11B “Advance amount received in earlier tax period and adjusted against the supplies being shown in this tax period in Table Nos. 4, 5, 6 and 7”, how the refund amount which is refunded due to not making a supply can be shown in Table 11B as an “Adjustment against Supply”??!!

This mistake is being followed by the well-known Accounting Softwares also. Now consider a following scenario to understand it.

| Sr. No. | Date | Nature of Transaction | Taxable Amount (Rs.) | CGST Amount (Rs.) | SGST Amount (Rs.) | Total (Rs.) |

| 1 | 31/03/2023 | Advance received for Service Booking | 100 | 9 | 9 | 118 |

| 2 | 25/04/2023 | Advance received for Service Booking | 50 | 4.5 | 4.5 | 59 |

| 3 | 01/06/2023 | Bill is raised for the actual service provided | 50 | 4.5 | 4.5 | 59 |

| 4 | 02/06/2023 | Balance Amount Repayment | 118 |

Enter the above transactions in some accounting software you are using. I have entered the same in one of the well-known accounting software. And found a following absurd result.

Here one can observe that the amount of adjustment in Table – 11B is much more than the amount of Supply as per Table No. 7. This is due to erroneous inclusion of refund voucher amount in Table – 11B instead of its inclusion in Table – 11A. (I have already drawn attention of this software developers towards this serious mistake on 17.01.2024 and the issue is under process and I have also drawn attention of CBIC, GST Council and Infosys to this matter on 20.01.2024 through tweeter but still no reply is received).

If such higher adjustment amounts (means in excess of supply amounts) are shown in Table – 11B instead of Table – 11A, there is a huge probability of getting notices from the GST department for the explanation which will cause wasting of precious time of Government, Taxpayers and Legal Consultants.

So, immediate change in this matter should be implemented on GST Portal and also by the concerned software developers.

Conclusion: The critical issue demands immediate attention from the GST Portal administrators and concerned software developers. The risk of receiving notices from the GST department due to incorrect reporting could result in wasted time for both the government and taxpayers. Swift action is necessary to rectify this discrepancy, ensuring accurate and compliant reporting on the GST Portal. Taxpayers and consultants are anxiously awaiting a resolution to this matter, urging stakeholders to address this issue promptly.

Author Bio