Hemanta Kumar Behera,

B.Com, ACA, ACMA

What is an e-way bill

* E-way bill is an electronic way bill for movement of goods which can be generated on the GSTN (common portal) =http://ewaybill.nic.in

* When an e-way bill is generated a unique e-way bill number (EBN) is or Service allocated and is available to the supplier, recipient, and the transporter.

* E-way bill will also be allowed to be generated or canceled through SMS

* The information furnished while generating e-Way Bill shall be made available to the registered supplier on the common portal who may

When an e-way Bill Generated

For every Inter-state / Intra –state movement of goods beyond 10 kms which have a value of Rs 50,000 and above, e-way bill is mandatory.

E-way bill has to be generated when there is a movement of goods: In relation to a ‘supply’.

the term ‘supply’ usually means a Sale- Branch Transfer- Sales Return- Barter/Exchange– where the payment is by goods instead of in money.

Therefore, e-Way Bills must be generated on the common portal for all these types of movements

Who should generate the e-way bill and why?

Registered Person– E-way bill must be generated when there is a movement of goods of more than Rs 50,000 in value to or from a Registered Person. A Registered person or the transporter may choose to generate and carry e-way bill even if the value of goods is less than Rs 50,000.

Unregistered Persons– Unregistered persons are also required to generate or e- Way Bill. However, where a supply is made by an unregistered person to a registered person, the receiver will have to ensure all the compliances are met as if they were the supplier.

Transporter– Transporters carrying goods by road, air, rail, etc. also need to generate e-Way Bill, if the supplier has not generated an e-Way Bill.

Further, it has been provided that where goods are sent by a principal located in one State to a job worker located in any other State, the e-way bill shall be generated by the principal irrespective of the value of the consignment.

E-WAY BILL IN CASE OF MOVEMENT BY REGISTERED PERSON

In case the movement of goods is caused by the registered person as a consignor (i.e. seller) or the recipient of supply as a consignee (i.e. buyer),whether in his own conveyance or a hired one or by railways or by air or by vessel, the registered person or the recipient may generate the e-way bill in Form GST EWB 01 electronically on the common portal after furnishing information in Part B of Form GST EWB 01.

In case the movement of goods is caused by the registered person and handed over to the transporter for transportation by road, but the e-way bill has not been generated – it would be the responsibility of the transporter to generate the e-way bill.

The registered person shall first furnish the information relating to the transporter in Part B of Form GST EWB 01 and then, the e-way bill shall be generated by the transporter on the basis of the information furnished by the registered person in Part A of Form GST EWB 01.

E-WAY BILL IN CASE OF SALE BY UNREGISTERED PERSON

In case the movement of goods is done by a person who is not registered under GST, either in his own conveyance or through a hired conveyance or through a transporter, the e-way bill in such a case shall be generated by the unregistered person himself or by the Transporter.

In other words, even if a person who is transporting the goods is unregistered, he would be the e-way bill generated either himself or through the transporter who is transporting the goods. The e-way bill shall be generated in Form GST EWB-01. An e-way bill can be generated by the unregistered himself as well on the Portal even if he is not registered.

E-way Bill in case of Sale by Unregistered Person to Registered Person

If the goods are supplied by an unregistered person to a registered person and the registered person is known at the time of commencement of movement of goods, it would be deemed that the movement of goods is caused by the registered person.

In such a case, the registered person or the transporter shall complete the formalities of the eway bill.

TRANSPORTER RESPONSIBILITIES

In case the consignor (seller) or the consignee (buyer) has not generated the e-way bill and the value of the consignment is more than Rs. 50,000, the transporter shall generate Form GST EWB 01 on the basis of invoice or bill of supply or delivery challan.

Any transporter transferring goods from one conveyance to another in the course of transit shall before such transfer and further movement of goods, update the details of the conveyance in the e-way bill .

On case where multiple consignments are intended to be trensported in one conveyance, the traspotrer shall indicate the serial number of each individually generated e-way bill in respect of each such consignment electronically on the common platform and a consolidated e-way bill in Form GST EWB 02 maybe generated by him on the GST Website prior to the movement of goods

INTIMATION & VALIDITY OF E-WAY BILL

1. Upon generation of the e-way bill, a unique e-way bill number (EBN) shall be made available to the supplier, the recipient and the transporter on the GST Website who may utilize the same for furnishing the details in Form GSTR 1.

2. The recipient shall communicate his acceptance or rejection of the consignment covered by the e-way bill within 72 hours.

3. In case the recipient does not communicate his acceptance or rejection within 72 hours of the details being made available on the GST Website, it shall be deemed that he has accepted the said details.

Cases when e-Way bill is Not Required

The mode of transport is non-motor vehicle.

Goods transported from port, airport, air cargo complex or land customs station to Inland Container Depot (ICD) or Container Freight Station (CFS) for clearance by Customs.

The distance between the consigner or consignee and the transporter is less than 10 Kms and transport is within the same state.

Transport of specified goods ( List of Goods prescribe by GST councile).

Registering and Enrolling for e-Way Bill Systems

http://ewaybill.nic.in

Registering and Enrolling for e–Way Bill Systems

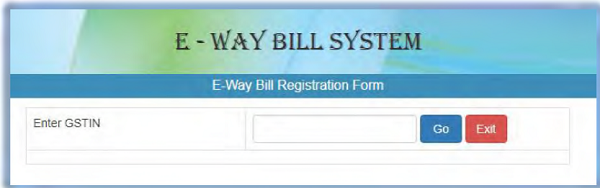

On the e-Way Bill portal, a first time GSTIN can register by clicking on the re-way bill Registration’ link. Then the user will be redirected to the `e-Way Bill Registration Form’. The registration form is shown below.

The user needs to enter his/her GSTIN number and shall click ‘Go’ to submit the request. Once the request is submitted the user will be redirected to the following page.

Registering and Enrolling for e–Way Bill Systems

Registering and Enrolling for e-Way Bill Systems

Logging into e-Way Bill System

On the left hand side, the system shows the main options. They are:

- e-Way bill — It has sub-options for generating, updating, cancelling and printing the e-Way Bill.

- Consolidated e-Way Bill — It has sub-options to consolidate the e-Way Bills, updating and cancelling them.

- Reject — It has the option to reject the e-Way Bill generated by others, if it does not belong to the user.

- Reports — It has sub-options for generating various kinds of reports.

- Masters —It has sub-options to create the users’ masters like customers, suppliers, products, transporters.

- User Management —It has sub-options for the users to create, modify and freeze the sub-users to his business.

- Registration — It has sub-options to register for SMS, Android App and API facilities to use.

Generating new e-Way Bill

e-Way Bill

Cancelling E-way bill

Generating Bulk e-Way Bills

SMS e-Way Bill Systems

SMS e-Way Bill

Consequences of non-conformance to E-way bill rules

If e-way bills, wherever required, are not issued in accordance with the provisions contained in Rule 138 of the CGST Rules, 2017, the same will be considered as contravention of rules.

As per Section 122 of the CGST Act, 2017, a taxable person who transports any taxable goods without the cover of specified documents (e-way bill is one of the specified documents) shall be liable to a penalty of Rs.10,000/- or tax sought to be evaded (wherever applicable) whichever is greater.

As per Section 129 of CGST Act, 2017, where any person transports any goods or stores any goods while they are in transit in contravention of the provisions of this Act or the rules made there under, all such goods and conveyance used as a means of transport for carrying the said goods and documents relating to such goods and conveyance shall be liable to detention or seizure.

(The author can be reached at cacwahemanta@gmail.com)