PART A-Composition Scheme

- What is the composition scheme

- Who is eligible to avail composition scheme

- Category of persons excluded from the Scheme

- Composition rates and computation of tax

- Procedure to be followed

Part B- Accounts and records

- Accounts and records to be maintained

- Period for which to be retained

- Composition levy is an option for specified categories of small taxpayers to pay GST at a very low rate on the basis of turnover

Advantages

√ Low rate of tax

√ Hassel free simple procedures for such taxpayers

√ Simple calculation of tax based on turnover

√ A very simple quarterly return

The composition scheme is for

√ Manufacturers (other than few notified goods)

√ Traders of goods

√ Restaurants

having aggregate turnover of Rs 75 lakh in the previous financial year subject to certain conditions and restrictions

The aggregate turnover limit is Rs 50 lakh for following 9 states

| Assam | Meghalaya | Manipur | Arunachal Pradesh | Mizoron |

| Tripura | Nagaland | Sikkim | Himachal Pradesh |

Two special category states, Uttrakhand and J & K have opted for keeping the turnover limit as Rs 75 lakh

Composition Scheme

- Aggregate turnover for determination of eligibility:

- Total all India turnover of all units under same PAN.

- It includes the value of exempt supplies and exports.

- It does not include the GST paid and the value of supplies received by a person on which he pays tax on reverse charge basis.

- Composition Scheme if availed shall include all registered persons having same PAN

- Composition scheme availability to a person shall lapse with effect from the date of his reaching the threshold turnover of seventy five lakh rupees.

Tax computation illustrated

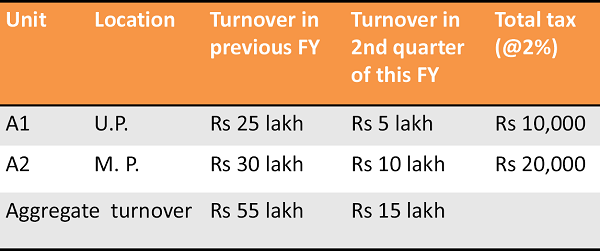

Taxpayer ‘A’ is a manufacturer having one unit in U P and another in M P. Total turnover of two units in last FY was Rs 55 lakh. Total turnover of two units in the first quarter of this year was Rs 20 Lakh

- Supplier of services except restaurants

- Any person who

- makes (i) a supply of non-GST goods; or (ii) an inter-state supply; or (iii) a supply that attract TCS

- is engaged in manufacture of goods, namely, ice cream, pan masala or tobacco and manufactured tobacco substitutes

- Is a casual or a non-resident taxable person

Composition Scheme- Conditions & restrictions

- If at the time of opting for scheme he has stock of goods purchased from unregistered person he will pay the tax on such goods

- Not entitled to take ITC on inputs

- Pay tax on inward supply from unregistered dealers

- Pay tax on supply attracting reverse charge

- Shall not collect any amount as tax

- Shall mention on bill of supply “Composition taxable person, not eligible to collect tax on supplies”

- Shall mention “composition taxable person” on notice or sign board displayed at a prominent place at his place of businesses

Composition Schemes- Procedure

Opting for composition scheme

- Return filing

√ Quarterly- by the 18th of the month after the quarter

- Opting out of composition scheme- Anytime at option

√ File an application if Form CMP-04

Part B: Accounts and Records

- Register person is required to maintain records and accounts of

- Production or manufacture of goods Supplies (inward/outward supply, supplier and recipient details, invoice, credit/debit note, delivery challan)

- Stock ( receipt, used, lost, balance and location where goods are stored including in transit etc)

- Input tax credit and use of inputs/input service

Output tax payable - Advance payments received and adjusted

Accounts and Records

- Composition person to maintain simpler records

- Warehouse/godown operator/transporter (even if not registered), to maintain record of consignor, consignee, movement, delivery, storage

- Agent to maintain records receipt and supply on behalf principal and records of authorization by the principal

- A C&F agent or a carrier having custody of goods on behalf of a registered person shall maintain details of goods handled by him.

Accounts and Records-requirements

- It is sufficient (but not necessary) to maintain accounts and records in electronic form

- Records can also be maintained manually – Such records are to be kept and be accessible at related place of business.

- Required to retained for six years from the due date of annual return

- Commissioner may for a class of taxable persons

- notify maintenance of additional documents

- prescribes alternative documents, if such class is not able to maintain records as per the provisions of the Act.

- Separate records for works contract ( receipt /supply /payments etc.)

- Production of records on demand

- Every taxable person having turnover exceeding prescribed limit shall get his account audited by a chartered accountant or cost accountant (Prescribed limit at present is two crore rupees)

- He shall submit the copy of audited annual account and a reconciliation statement.

Maintaining electronic records:

√ Are to be authenticated by digital signature

√ Maintained and preserved in the manner that these can be restored within reasonable period in any circumstances

√ On demand to provide details, password, and explanation of codes used.

i am running footwear showroom in partnership in punjab.All the purchasing is from haryana.i opted in composition scheme due to decrease in sale with annual sale less than six lac.Is the firm need audit and to maintain books.showroom is seven years old.please suggest what to do .

sir i am a c&f of pharmaceutical company and i take gst composition scheme. i want to ask one thing that i supplies product to the stockist without gst amount as i am composition levy but tell me sir if stockist want to supplies product to the chemist then he add gst amount in the bill or not.

Contact for new registration, GST retrun and other GST related service

what are the provisions with respect to Invoices to be made by vendor under composition scheme. Does he have to make self invoice recording his daily sale and does he have to raise invoice in excess of a certain amount?

I am running a pharmacy shop in Punjab. Can I register with the Gst composition scheme? What are the documents required to be registered and what will be the tax rate

One of my clients have inter-state purchased stock as on 30.06.2017. However, his turnover is less than 50 lakh. Can he opt for migration in the new regime for this year? How will he disburse his old stock?