Let us do this by establishing a core Principle…

♦ Core principle of any indirect taxation model has to be…

Input Tax Credit will be provided only on “matched” invoices

♦ By “matched” we mean legitimate invoices where the supplier has admitted tax liability by uploading the invoice on the portal

♦ This means either deny or automatically reverse credit on unmatched invoices

Failure Criteria : There are some models that are doomed to fail

1. Any solution that increases the burden on the taxpayer to correct mismatches is guaranteed to fail

– There will be severe resistance from the taxpayers to bear the additional burden

2. Any solution that relies on tax official’s intervention to reduce the mismatch is also doomed to fail

– Especially in the GST regime where there will division of administrative authority b/w Center & State

– Introduces subjectivity of assessments & audits and potentially perceived as tools of harassment

3. Any solution that permits higher levels of mismatch in the first place will also fail

– High levels of mismatch means there can be no automatic reversal. Paves way for failure causes 1 & 2 i.e. greater burden of correction and Tax official intervention

Let us take a look at the GSTR – 1-2A-2-1A model

♦ The model “attempted” to solve the some of the failure scenarios by introducing an acceptance workflow for invoice matching. As a principle – a step in the right direction.

♦ While GSTR-1 was reasonably successful, GSTR-2A and & 2 did not work as planned

♦ It has been presumed that comparing Supplier provided invoice with Purchase books was too much a burden. But is it?

Comparing Supplier provided Invoice with own purchase books

♦ Let’s not forget…

Every business large or small, automated or manual routinely compares Supplier invoice with the purchase books!

– It is a necessary step before releasing payment. No business says – comparing is hard – so let me pay whatever supplier claims!

But then why was GSTR2 perceived as a burden?

♦ Comparing Supplier invoice with Purchase books all over again for tax credit claim purposes is a burden

♦ Comparing Supplier invoice that is not at the same granularity as their books is a burden

♦ Comparing & correcting Supplier invoice 2 months after the transaction is a burden

♦ Comparing all Supplier invoices in a span of 5 days that too by a professional is a burden

In summary, GSTR-2 model was burdensome because…

♦ By modeling “Invoice Upload” and “Acceptance” as Tax “Returns” (GSTR-1 & GSTR-2), the model created a perception that there are 3 returns per month.

– People perceived them as a tax function creating a dependence on a tax professional when upload & acceptance is patently a business reporting function

♦ Structure of forms was also too complex which required a tax professionals help

– Concepts like Tax on Advance, its utilization to offset liability, separate reporting of different type of invoices made GSTR-1 & 2 look more like a return form than a statement

♦ Reporting of invoices at rate-level instead of line-item level created more work to the supplier

– It also made matching and acceptance unacceptably tedious

What then is a Successful Model

♦ A successful model is one which achieves the agreed goal without the failure characteristics of increased tax payer burden or intervention of tax official.

♦ In other words one which…

…aligns with the natural business cycle of verification & payment of supplier invoices

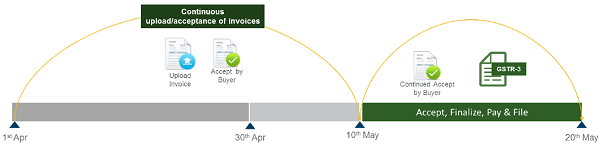

Highlights of the proposed solution – Invoice Upload

♦ Suppliers “upload” sales invoices on the GST System which automatically calculates his/her liability. Invoice is also made available to Buyer for acceptance

♦ Key Contrasts from GSTR-1

– It is simply an Invoice “Upload” – not “filing” of return

– Invoice format and data granularity to exactly match the actual invoice submitted by supplier for payment viz. Invoice Item Level right from day one – not rolled up at tax rate or commodity levels

– Upload happens on a continuous basis. It means the verification and acceptance coincides with the actual business transaction. Invoices uploaded after the 10th is automatically included in next return

– Market forces will evolve a model where invoice is paid only after upload on GST System

Highlights of the proposed solution – Invoice Acceptance

♦ Buyer “accepts” supplier invoices on the GST System which automatically determines the input tax credit (ITC)

♦ Key Contrasts from GSTR-2 and pure System Matching Model

– It is simply an Invoice “acceptance” – not “filing” of return. Acceptance can happen on continuous basis – not waiting for all the GSTR-1 to be filed.

– In the case of pure System matching model the correction and acceptance will be at least 20-50 days after the transaction

– Invoice once accepted is “locked” cannot be modified by the supplier. Brings finality to the transaction

– System to provide robust tools to facilitate smooth acceptance – including offline matching of supplier invoices with purchase books, auto-acceptance capabilities and improved support to GSP/ASPs for tighter integration with accounting packages.

Highlights of the proposed solution – Handling Missed Invoices

♦ We propose to eliminate concept of “Provisional Credit” – However Buyers can “notify” supplier through the system to upload any missed invoice – but cannot upload or modify it themselves

♦ Key Contrasts from GSTR-2

– Buyer is simply declaring the invoices missed by his/her supplier

– System will notify the supplier – reminding them to upload the same

– When supplier uploads such invoice, System will match and remove it from the missed invoice list

– Missed invoice statistics will be retained and used to compute performance scores of the tax payers

Highlights of the proposed solution – Handling non-Payment

♦ In the proposed model, there will be no “Mismatch” in the traditional sense – hence no question of reversal. But there is still the possibility of non-payment of taxes by the supplier

♦ The current law penalizes the buyer by denying or reversing credit – but this is widely perceived as unfair to buyer. We understand courts have also ruled against it

♦ It is therefore recommended that the new law…

– Re-Define the criteria of a legitimate invoice as one where Supplier has admitted liability by uploading into the portal

– Makes provisions to recover dues from the Supplier rather than penalizing buyer

Highlights of the proposed solution – Channels of reporting

♦ GST System will offer multiple channels for upload and acceptance of invoices and filing of returns

– Small taxpayers with no automated accounting systems can view and accept pending invoices directly on the portal

– Small-Medium Taxpayers with some level of automation can use Excel based offline tool to download, compare and accept pending invoices

– Large tax payers with fully automated accounting will do the reconciliation and acceptance directly in their accounting system and upload results directly through APIs

Proposed Solution

♦ Continuous invoice upload/acceptance with counter parties – No cut-offs

♦ Remove concept of provisional ITC

- No uploading of missed invoice or modify supplier invoice.

- Consequently, no mismatch or ITC reversals

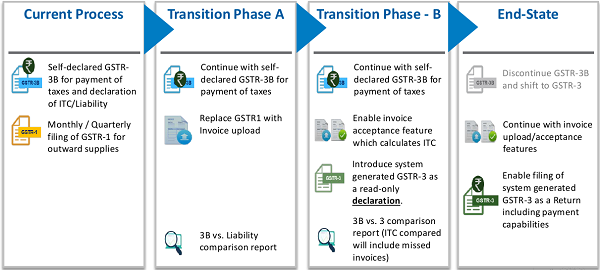

We further propose a Gradual Transition so that it …

♦ Eliminate risk of adoption issues impacting tax collection

♦ Provide sufficient time to stabilize the system including enhancements to improvements to user experience based on industry feedback

♦ Provide sufficient time to taxpayers to adapt to the new model – understand counter-party behavior & data quality and implement corrective measures as required

♦ Provide sufficient time to enable eco-system to develop tools/applications for automated upload of sales invoice and reconciliation of purchase invoice

Gradual Transition to the New Model

Key Benefits of the proposed model

♦ Simplicity: Dramatically simplifies the process and reduces burden

– As established earlier, every business routinely compares supplier invoices with their purchase books before release of payment. This model simply integrates with this natural business process

– Compliance is as simple as “reporting” their business transaction regularly and making payment against a system generated return

– In contrast, a pure System matching model with high levels of mismatch actually increases the burden – comparing & correcting stale transactions is lot harder than doing it as part of business cycle

♦ Incentive Aligned : Natural alignment of incentives to both supplier and buyer

– Supplier has to report invoices on-time – otherwise will not get paid or end-up paying interest

– Buyer has to accept invoices on-time – otherwise will not get his/her input credit

♦ High Data Quality: Cleaner data with low level of initial “mismatch”

– As the model integrates with the natural business process between supplier and buyer, one can expect significant improvement in data quality

– Experience from VAT shows that majority mismatch is due to difference in Invoice No. and Date. This happens due to dual version of same data flowing from both parties. Having a single version of data will reduce initial mismatch levels to a great extent

– Since incentives are aligned to business interest, there will be greater focus to upload correct data

In conclusion…

♦ We must agree on the core principle of…

Input Tax Credit will be provided only on “matched” invoices

♦ Any model that increases tax payer burden, or relies on tax officer intervention is likely to fail.

♦ A successful model is one which aligns with the natural business process and not make Tax return preparation a separate function

♦ The proposed model will result in lower compliance burden to the tax payer, higher revenue collection and reduced administrative burden to the officials

Download Nandan Nilekani Presentation on Simplification of GST Compliance

Basicaly the problem is , the option of Revise return is not Available…So if its made Available , than the there will be relief from tension . So from my perspective revise return should be made available in all the respective returns.

Secondly , return should be made Quarterly. No matter how much robust software or system you have , if you have to upload return after every 5 – 10 days , it means your social life is over , peace is over. so it should be made quarterly.

if more simple approach can be adopted by uploding excel file containing all details related to sale in standard format by a supplier on daily /weekly basis or any fixed date solve the entire issue . if a software automatically credit the input GST on the basis of supplier information to buyers a/c and same can be made available for adjustment against Output GST most of the problem automatically resolved . If Buyers were made responsible for any mismatch without any government intervention he can check his ITC credit before making the payment to supplier.

Rather then do the things in simple way Govt. functionaries always try to make it very complicated for aam janta for reason known to most of us . Just an approach with an aim to simplify the things is needed .

life is going to be more miserable … Mr.Modi and his advisors have made it a HAVOC ..

Can’t u make it simple and precise……?

What are u guys trying to prove and establish by matching invoices….

Good suggestion Govt. Should also make Standard Perfoma for Invoice for all pesons to implement this .

This simplification of invoice matching will be accepted by everybody. No extra compliance burden should be imposed on the small taxpayers.

Excellent suggestions by the Infosys .

Czar. GST present regime will take at least one more year to get stabilized.

GST becomes user friendly on following his suggestion.

Badrappa – Smilax Laboratories limited, Hyd

Success of any scientific formula depends on certain terms and conditions fulfillment without fail otherwise that formula will not work, like, if you want to make hydrogen, which laboratory equipment’s should be used and which ingredients in specific quantity should be used is necessary to be known otherwise as a result, it will blast and if big mistake it can destroy the laboratory as well.

Mr. Nandan Nilekani, being a computer master and to improve his business he can justify his products, utilities and it’s terms and conditions but being an Accountancy professional and having an experience of more than two decades, I can say that implementation of GST through software utilization at all India level considering that every business man is having all the required hardware’s, software’s, training and perfect knowledge level to give input in the software, to give perfect output as desired by software community and the Government but the ground realities are different and even awareness level at the grassroots cannot be assumed at perfection level to give perfect input as the basic condition of the success of any software. Rule of the software is “GARBAGE IN, GARBAGE OUT.” Even in a small business it is very difficult to get perfect result from the software because at the input level lot of practical problems remain then how anybody can assume that at all India level all different businesses/services/manufacturing units/social organisations, different level of knowledge, different behavior of people, language barriers, etc. will dance at the tune of *******************.

BEST OF LUCK TO INDIAN ECONOMY.

Yes, its a good proposal, continuous upload & acceptance of invoices will reduce fear of loss of input credit by buyer.& liability of supplier get locked.

work load & mistakes will get reduced.

In built check can be developed in system itself,Supplier should first declare his different types of invoice series , system should store this series & check sr nos of invoices from beginning, system should allow to declare number as cancelled . so when invoice number 5 is uploaded 7 should not come for uploading unless invoice no 6 is uploaded or declared as cancelled. This will create discipline at suppliers end .

Also supplier should able to correct invoice before receiver accepts it anytime , once receiver accepts it should get locked. not only when uploaded .

liability of supplier & input credit of receiver should be always cumulative on date .

At the end of 6 months reconciliation of taxes paid with liability should be done.

Excellent suggestions by Nilekaniji

It is people like him to be given Padma bhushan and the like.

He will make GST work

If the government is committed let it show the same by adopting the suggestions.