India’s beleaguered power sector’s financial problems have been making the headlines of late. On February 12, 2018, the RBI in its revised guidelines for resolution of stressed assets mandated banks to complete insolvency resolution proceedings within 180 days of default, classifying the loan as a “special mention account” with even a one-day delay in repayment. This deadline for the 34 stressed power companies concluded at the end of August 2018 creating fear among market participants of the potential loss it could impinge on the banking system and also the companies.

Several of these power companies had filed petitions against the RBI ruling but these were turned down by the high courts. However, on 11 September 2018, the Supreme Court issued an order staying further moves against the distressed power sector by its creditors. It also transferred all the pleas in various courts to itself directing the RBI to maintain the status quo until the plea is next heard in November. This provides some relief especially to the power producers which are near to a resolution and provides some leeway to others to come up with their resolution plans.

In our view, while these judicial interventions may ease some of the stress in the sector (as a few of these stressed companies might hopefully find potential buyers or get their debt restructured), these will not address the enduring complexities plaguing the sector, doing little for the ultimate sustainability of the sector.

Why did this happen?

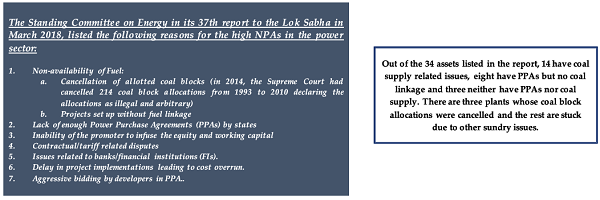

Despite a plethora of government interventions and bail-out schemes, the power sector situation remains grim —plagued by shortages, logistics bottlenecks, lack of coordination among various stakeholders and policy inconsistency. While its woes have been long standing, their growing drag on banks is a major source of concern. Around a fifth of non-performing assets, currently estimated at Rs 10.25 lakh crore, involve some 34 stressed power project (32 belong to private companies while 2 are from the public sector), totalling 40 GW in generation capacity.

Looming NPA crisis: While banks and the government are trying to come up with possible resolutions such as the Pariwartan scheme (an ARC floated by state-owned Rural Electrification Corporation) or the Samadhan scheme (an initiative by banks led by SBI to try and resolve projects which were complete or near complete), these efforts will amount to a possible resolution for only 9-10 projects outside the NCLT (~Rs 70,000 crore). For the remaining Rs 1 lakh crore, the recovery is likely to be meagre and banks may have to take a higher haircut. Tentative estimates show that around 40% of the projects are incomplete and will thus find it hard to attract buyers.

The “Genco – Discoms – States” nexus

While the government, RBI, banking system and the judiciary are trying to cope with the stressed power projects, the electricity distribution companies (Discoms) are adding to the latter’s woes. Distribution companies’ unpaid dues to 23 power producers stood at Rs 38,462 crore at June’18-end, up 30% from the level a year earlier. Irregular and delayed payments by discoms have been cited as the primary reason behind private generation assets becoming stressed. The much touted statistics of the Discoms having cut their financial losses by Rs 17,352 crore or 50% on an annual basis by March-end 2018 (under the scheme Ujwal Discom Assurance Yojana) masks these dues that are yet to paid to the Gencos (power generation companies.

States too must bear their share of the blame. Their unwillingness to carry out tariff revisions in line with the UDAY stipulations and heavy cross subsidization among users (lower tariffs for agricultural consumers at the cost of industrial ones) have led to Discoms’ huge dependence on state subsides, which usually get disbursed with a delay leading to working capital shortage for discoms (states’ dues to the power discoms are estimated at around Rs 39,442 crore1). This, in turn, makes it difficult for the power distributors to implement infrastructure reforms to reduce losses, thereby, turning the wheels of the precarious and peculiar vicious cycle.

Estimates show that the Discoms’ interest outgo on the working capital loans (on account of delayed subsidy payment by the states) amount to around Rs 4,000 cr annually. This translates into one percentage point of AT&C losses.

To be fair to the government, the scheme UDAY (introduced in November 2015) was introduced with the right intentions, wherein the government created a mechanism to shift the high-cost debt of state power utilities on to the state budgets and pushed for operational reforms that were to keep the incremental losses in check. Admittedly, the cost of debt and losses did come down post the scheme. But the Discoms in conjunction with the state governments were also supposed to tighten their belts, increase tariffs and reduce incremental losses. However, the progress of the UDAY in terms of hard reforms has failed to impress. As a result, the DISCOM woes continue.

To put things into perspective, in May 2018, 22% of the power generated was lost with estimates of each per cent lost costing about Rs 4,146 crore.

On top of it, the power sector, going forward, will have to cope with the government’s clean energy mandates. By next year the DISCOMs will have to purchase nearly 17-20% of their power from renewables (solar and wind). 2This will be an added cost for the DISCOMs because they will anyway have to purchase coal-based power (whose cost has also increased because of higher coal cess) for their customers. As a spillover effect, power producers will have to cut down on their production and work with a sub-optimum plant load factor (PLF), which increases their cost. And with this, we come back to the square one.

How does all of this stack up for states?

As a natural outcome, state governments are increasingly becoming fiscally strapped. Their combined fiscal deficit to GDP ratio for the year ending March 2018, came out at 3.1% against a budget of 2.7% with as many as 19 states exceeding the 3% FRBM norm. While pressures on the revenue side and expenditure side from farm loan waivers and pay hikes under the 7th CPC have dented states’ finances as well, rising power sector costs on account of higher power subsidies and obligations under the UDAY scheme are pressures that are likely to persist going forward.

2 Indian Express article “The coal and power Tango“ dated 30th July 2018 Until now interest costs on servicing of UDAY bonds were the principal power-sector expense for the states but unless the discoms manage to turn around (technical parameters like AT&C loss reduction are still not met by most states), their losses would turn out to be increasingly onerous. Under the UDAY scheme, the states are expected to take over previous year’s discoms’ losses in a graded manner from FY18:(5% of FY17 losses in FY18, 10% FY18 losses in FY19, 25% FY19 losses in FY20 and 50% of FY20 losses in FY21). On top of it, costs will multiply once the principal repayment (on UDAY bonds) starts to begin in the next couple of years.

The overall interest expenditure of the states rose 16.5% in FY18 and is projected to rise 8% in FY19, largely due to the taking over of the discoms’ debts. For instance, UDAY costs of Rajasthan (top issuer of Uday bonds – Rs 72,090 cr) was a substantial 0.74% of its GSDP in FY18.

Special Focus: UDAY’s report card remains unimpressive

With the threat of bad loans looming large, UDAY scheme’s efficacy is being increasingly questioned. The general belief that UDAY is a panacea for power sector woes has now clearly been shelved.

Our analysis on the progress on the scheme shows that while an improvement in performance is witnessed in some states (particularly in Discoms’ losses), inadequate progress on other key parameters such as reduction in AT&C losses continue to plague the sector with large variation among states.

- Uday mandates discoms to bring down their aggregate technical and commercial (AT&C) losses to 15% by the end of 2019. Interestingly, only Himachal Pradesh, Andhra Pradesh, Gujarat, Telangana and Tamil Nadu have achieved the 15% threshold. Most states fall in the +20% bracket.

- Failure to attain 15% AT&C loss levels would mean additional woes for the discoms especially the ones with higher AT&Cs (for example, Jharkhand at 36.9% and Bihar at 39.1%), as the power ministry has decided to compute tariffs assuming AT&C losses of 15% – whereas the actuals are way higher; the national average is around 23%.

- With an overall gap of 0.28 units (on a pan India level), the scheme warrants bringing down the difference between the average cost of supply (ACS) per unit of power and per unit average realized (ARR) to zero by the end of FY19. While some states have reduced the gap below 0.5, more than ten states have a gap exceeding 0.5. The situation remains dismal in states like J&K, Jharkhand and North Eastern states (except Tripura) with unit gaps in excess of 1.

The major reason attributed to the below par achievements in the reduction of AT&C losses and ACS – ARR gap is less than 70% achievement in five of the 10 crucial operational parameters. For instance, while the performance of feeder metering both in rural and urban areas is 100%, the same for smart metering stands dismal.

Another reason often cited as contributing to high AT&C losses in some states is constant delays in disbursal of subsidies by the state governments (as discussed above). High level of cross subsidization in some states (for instance 40% in UP) owing to political compulsions has been the prime cause for the ever growing subsidy burden on states’ finances. Given the current status, government’s target of capping cross subsidy at 20% effective January 2019 clearly looks unattainable.

On paper, UDAY appears to have impacted discoms’ finances favourably. Overall losses of discoms under UDAY have decreased from around Rs 51,590 crore in FY16 to Rs 17,352 crore at the end of FY18. Specifically, electricity distribution companies (discoms) in states such as Maharashtra, Rajasthan, Haryana and Andhra Pradesh — that posted operational losses in 2015 turned profitable by the end of March 2018. States like Rajasthan UP, which were saddled with humungous debt in 2015 (inception year for UDAY) have also seen their losses coming down from Rs 5,208 crore and Rs 6,619 crore in FY17 to around Rs 1,930 crore and Rs 4,845 crore in FY18 respectively.

This apparent disconnect between actual performance and their financial score needs to explained.

1) A lot of the reduction in losses are because of lower interest outgo (because of the UDAY), therefore, it’s important to see how the Discoms perform on incremental losses, moving ahead. The lower interest outgo is the result of a reclassification of Discom loans from banks (that entailed a higher rate of interest) to state government bonds that have lower yields and thus translate into lower interest costs.

2) As we mentioned earlier in the report, the reduction in losses masks the unpaid dues that several Discoms owe to the power generation companies, which might be artificially deflating the losses for the time being.

Notes:-

1 Financial Express article “UDAY Targets: Discoms hit by payment delay” dated 25 May 2018

Disclaimer: This document has been prepared for your information only and does not constitute any offer/commitment to transact. Such an offer would be subject to contractual confirmations, satisfactory documentation and prevailing market conditions. Reasonable care has been taken to prepare this document. HDFC Bank and its employees do not accept any responsibility for action taken on the basis of this document

*Mr. Abheek Barua, Chief Economist, HDFC Bank. Mr. Barua tweets at @AbheekHDFCBank.