MEANING OF IMPAIRMENT OF ASSETS

In conformity with AS-28 impairment of assets means reduction in value of assets due to any market factors or performance of assets. It is applied to fixed assets including intangible assets. As per the provisions, the following assets are specifically excluded out of coverage of Impairment Rules:-

- Inventories (valuation as per AS-2)

- Investments (valuation as per AS-13,AS-30,AS-31,AS-32)

- Deferred tax assets(DTA)(Valuation as per AS-22)

- Investment in Lease Agreements(AS-19)

- Investment in Retirement Benefit Plans(AS-15)

- Valuation of Construction Contracts(AS-7)

IMPORTANT DEFINITIONS:

Ø CARRYING AMOUNT:

It means the book value of an asset after depreciation and after any revaluation which is carried by an enterprise in its balance sheet.

Carrying amount of fixed assets: Gross book value less accumulated depreciation

Carrying amount of Intangible assets: Original cost less total amortisation till date.

Ø RECOVERABLE AMOUNT:

Recoverable amount =net selling amount or value in use Whichever is higher

Net selling price =Expected selling price – Expected cost of Disposal

Value in use = Future cash inflow x Pvf

Ø MEANING OF IMPAIRMENT LOSS :

Carrying amount of an asset –Recoverable amount

Impairment loss to be recognised:

- As an expense in the P&L Account, immediately, otherwise

- As a revaluation decrease (if carried at revalued amount)

ACCOUNTING TREATMENT:

To Assets

To Impairment Loss a/c/

|

Ø Cash Generating Units (CGU):

The smallest identifiable group of assets that generates Cash flows from continuing use that is largely independent from other assets or groups of assets. Estimate recoverable amount for the individual asset. If this is not possible, then estimate recoverable amount of the asset’s cash generating unit.

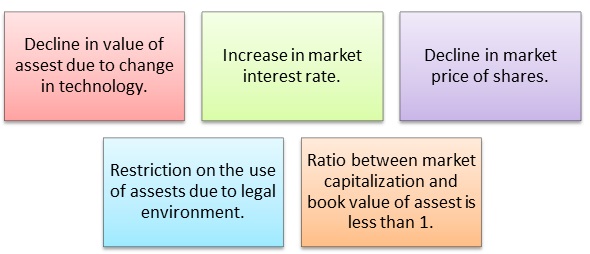

In addition to applicability of AS -28 is based on indicators which are as follows:

EXTERNAL INDICATORS

INTERNAL INDICATOR

Recognition and Measurement of Loss:

- Adjust depreciation (amortization) charge for the asset in future periods.

- Allocate the asset’s revised carrying amount less its residual value on a systematic basis over its remaining useful life.

Bottom-Up’ Test – Goodwill and Corporate Assets

Perform this test if goodwill or corporate asset can be allocated on a reasonable and consistent basis to the CGU under review. Compare recoverable amount of cash generating unit (CGU) to its CA (including goodwill or corporate asset) and recognise impairment loss.

Top-Down’ Test – Goodwill and Corporate Assets

If goodwill cannot be allocated on a reasonable basis then perform ‘top down’ test. Identify smallest CGU that includes the CGU under review and to which goodwill or corporate asset can be allocated on a reasonable basis. Then compare RA of the above CGU to its CA (including goodwill or corporate asset) and recognise impairment loss.

Treatment of Impairment Loss for a CGU

The carrying amount of an asset (which is part of CGU) should not be

reduced below the highest of:

(a) Net selling price.

(b) Value in use.

Unabsorbed impairment loss allocated to other assets in CGU.

REVERSAL OF IMPAIREMENT LOSS:-

An enterprise should, at each balance sheet date review whether the previously recognized impairment loss has ceased to exist or has decreased. If there is any external or internal indication to this effect, the recoverable amount of that asset should be estimated. If the recoverable amount exceeds the carrying amount then the impairment loss can be reversed and such reversal is to be treated as income.

The reversal of impairment loss previously recognized for a cash generating unit is to be allocated first to assets, and then to goodwill. Impairment loss for goodwill should not be reversed unless proved that impairment was caused by external event of exceptional nature and subsequent events have reversed the first event that caused the impairment loss.

Reversal of impairment loss is lower of the following:

(a)Intangible loss already recognised less saving in depreciation.

(b)Recoverable amount less carrying amount.

DIFFERENCE BETWEEN AS-28 AND IND AS 36

| AS-28 | INDAS-36 |

| 1.It provides for partial exemption to small – medium companies or enterprises.

|

1. It does not provide for any exemptions. |

| 2. It requires that the impairment loss recognised for goodwill should be reversed in a subsequent period when it was caused by a specific external event of an exceptional nature that is not expected to recur and subsequent external events that have occurred that reverse the effect of that event.

|

2. It prohibits the reversal of impairment loss of goodwill. |

| 3.In this goodwill is allocated to CGUs only when the allocation can be done on a reasonable and consistent basis. If that requirement is not met for a specific CGU under review, the smallest CGU to which the carrying amount of goodwill can be allocated on a reasonable and consistent basis must be identified and the impairment test carried out at this level. Thus, when all or a portion of goodwill cannot be allocated reasonably and consistently to the CGU being tested for impairment, two levels of impairment tests are carried out, viz., bottom-up test and top-down test.

|

3. In this goodwill is allocated to cash-generating units (CGUs) or groups of CGUs that are expected to benefit from the synergies of the business combination from which it arose. There is no bottom-up or top-down approach for allocation of goodwill. |

| 4. It does not require the annual impairment testing for the goodwill unless there is an indication of impairment. | 4. It requires annual impairment testing for an intangible asset with an indefinite useful life or not yet available for use and goodwill acquired in a business combination.

|

| 5.It does not specifically exclude biological assets.

|

5. It specifically excludes biological assets related to Agricultural activity |

| 6.It does not apply to subsidiaries, joint ventures and associates | 6.It is applied to financial assets which include subsidiaries, joint ventures and associates.

|

Disclosures

- Impairment loss recognized and reversed for each class of asset

- Amount of impairment loss set off against revaluation reserve and amount of reversal of impairment loss credited to revaluation reserve segment reporting – AS 17)

- Mode of arriving at recoverable amount supported by evidences for net selling price or discount rate in case of value in use.

- Events leading to recognition of impairment or reversal

- Nature of asset and the reportable segment to which it belongs for primary format as per AS 17

- Description of cash generating unit

- Key assumptions used in the determination of recoverable amount of asset.

Compiled By:-

Shrutika Kohli

B.COM (H), MBA (FINANCE), CA FINAL STUDENT

Email id: – kohlishrutika12@gmail.com

What is the treatment of Asset Impairment under Income Tax Act? Is it an Allowable Expense?

As per companies act 2013 impairment loss treatmentafter asset been devalued, whether impairment loss will be setoff against revaluation reserve? Do reply