It has been observed that imports under Free Trade Agreements (FTA) are on the rise. Undue claims of FTA benefits have posed a threat to domestic industry. It is sometimes flouted by importers to wrongly claim that a particular import is originating from an FTA partner country so as to pocket the benefits. Such imports require stringent checks to curb misuse of FTA Provisions. Accordingly, steps are being taken to crack down on frauds, re-work Rules of Origin (RoO) provisions. RoO determine whether enough value addition took place in the FTA partner country for the import to qualify as originating from there.

The government has come out with norms for the enforcement of ‘Rules of Origin‘ provisions for allowing Preferential Rate of Customs Duties on Products Imported under Free Trade Agreements aiming at striking a delicate balance in its efforts to check misuse of FTAs by unscrupulous importers and ensuring that their use by legitimate businesses is not discouraged.

The Department of Revenue has notified the ‘Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020’ which would “come into force on September 21, 2020”.

Purpose of “Rules of Origin”

RoOs are meant to define the ‘nationality’ of imports and to make PTAs preferential. Countries enter into Free Trade Agreements with each other in order to provide enhanced, Preferential Market Access Opportunities to one another. But in order to put these into practice, it is necessary to have Criteria that tell us when products come from the partner country to whom such preferential access is given, and are not Re-Exported from another source (Country).

“Rules of Origin” are the criteria needed to determine the national origin of a product. Countries which offer zero or reduced duty access to imports from certain trade partners often apply a set of preferential rules of origin to determine the eligibility of products to receive preferential access.

The new norms have been framed with a view to put in place greater scrutiny of imports and checking inbound shipments of low-quality products and dumping of goods by a third country routed through an FTA partner country.

The ‘’Rules of Origin” provision prescribes for the minimal processing that should happen in the FTA country so that the final manufactured product may be called originating goods in that country.

Under this provision, a country that has inked an FTA with India cannot dump goods from some third country in the Indian market by just putting a label on it. It has to undertake a prescribed value addition in that product to export to India. Rules of origin norms help contain dumping of goods.

India has inked FTAs with several countries, including Japan, South Korea, Singapore, and ASEAN members. Under such agreements, two trading partners significantly reduce or eliminate import / customs duties on the maximum number of goods traded between them.

Where are Rules of Origin Used?

Rules of origin are used:

> to implement measures and instruments of commercial policy such as anti-dumping duties and safeguard measures;

> to determine whether imported products shall receive most-favoured-nation (MFN) treatment or preferential treatment;

> for the purpose of trade statistics;

> for the application of labelling and marking requirements; and

> for government procurement.

Industry Concerns

There have been many incidents, where certain players have imported products with an origin of certificate that does not accurately reflect the country where these products have been actually manufactured.

The TV industry has been one of the key sectors that has been raising concerns about misuse of FTAs, as there is surge of import of televisions from Vietnam (which is part of the India-ASEAN FTA).

India’s imports of copper, RBD (refined, bleached and de-odorized) palm-olein, paper and paperboard are mostly effected due to flouting of ‘Rules of Origin’ and dumping of these commodities under Free Trade Agreements (FTAs) from non-producing countries. Import of paper and paperboards from non-producing countries is a matter of great concerns for Indian manufacturers.

Import of RBD (refined, bleached and deodorised) Palm-olein from Nepal is feared to have originated from Malaysia. While direct import of Palm-olein attracts customs duty of 44.5 per cent, import through Nepal could be possible at ‘Nil’ duty under the South Asian Free Trade Area (SAFTA).

The government had levied MIP after pepper traders and exporters complained that Vietnamese pepper was coming to India via Sri Lanka with certificate of origin issued by the latter. Currently, India levies zero duty import on 2,500 tonnes of pepper from Sri Lanka annually under the Indo-Sri Lanka Free Trade Agreement. Any export above the limit is subjected to 8 per cent duty under South Asia Free Trade Agreement, as against the usual customs duty of 70 per cent on pepper import into India.

Each Trade Agreement, has its own set of Rules of Origin. Say under the FTA, 35 per cent value addition by the exporting country on free-on-board (FOB) value of goods is a required, then exporters adding shipping and other miscellaneous costs including handling, loading and unloading to achieve the mandatory norms of 35 per cent value addition.

“Value addition of 35 per cent is impossible in the case of copper. Huge quantities of refined copper bars that were being imported from Sri Lanka and Vietnam until recently, got curbed automatically after the Indian government removed copper bar from the FTA commodities list. Similarly, import of copper from other FTA countries can also be restricted for the benefit of local producers,”

Likewise, there are many instances of misuse of FTA provisions detected and evidences from recent FTAs suggest un-favourable gains to our trade partners.

Customs (Administration of Rules of Origin under Trade Agreements) Rules, 2020 (CAROTAR, 2020)

Notification No. 81/2020-Customs (N.T.) dated 21st August, 2020.

Circular No. 38/2020-Customs; Dated 21st August, 2020

The Salient Features of the “CAROTAR, 2020”

Preferential Tariff Claim – Filling of Bill of Entry:

According to the notification, to claim preferential rate of duty under a trade agreement, the importer or his agent, at the time of filing bill of entry, has to make a declaration in the bill that the imported products qualify as originating goods for preferential rate of duty under that agreement; and produce Certificate of Origin covering each item on which preferential rate of duty is claimed.

Denial by the Proper Officer

The claim of preferential rate of duty may be denied by the proper officer without verification if the certificate of origin is incomplete or has any alteration not authenticated by the issuing authority or the certificate is produced after its validity period has expired.

Origin Related Information to be Possessed by Importer :

The importer, also has to possess all relevant information related to country of origin criteria, including the regional value content as per as indicated in Form I of the Notification, and submit the same to the proper officer on request. The Importer shall keep all supporting documents related to Form I for at least five years from date of filing of bill of entry and submit the same to the proper officer on request. The Importer shall exercise reasonable care to ensure the accuracy and truthfulness of the aforesaid information and documents.

Requisition of information from the importer

Where, during the course of customs clearance or thereafter, the proper officer has reason to believe that origin criteria prescribed in the respective Rules of Origin have not been met, he may seek information and supporting documents, as may be deemed necessary, from the importer in terms of rule 4 to ascertain correctness of the claim.

Where the importer is asked to furnish information or documents, he shall provide the same to the proper officer within ten working days from the date of such information or documents being sought.

Verification could also be undertaken on random basis as a measure of due diligence.

Verification Request

An officer may, during the course of customs clearance or thereafter, request for verification of certificate of origin from verification authority (the authority in exporting country or country of origin, designated to respond to verification request under a trade agreement) where there is a doubt regarding genuineness or authenticity of the certificate for reasons such as mismatch of signatures or seal when compared with specimens of seals and signatures received from the exporting country.

Identical Goods from the Same Exporter or Producer – Reject of other Claims of Preferential Rate of Duty

Where it is determined that goods originating from an exporter or producer do not meet the origin criteria prescribed in the Rules of Origin, the Principal Commissioner of Customs or the Commissioner of Customs may, without further verification, reject other claims of preferential rate of duty, filed prior to or after such determination, for identical goods imported from the same exporter or producer.

Compulsory Verification of Assessment

Where an importer fails to provide requisite information and documents by the due date prescribed under rule 5, or where it is established that he has failed to exercise reasonable care to ensure the accuracy and truthfulness of the information furnished under these rules, the proper officer shall, notwithstanding any other action required to be taken under these rules and the Act, verify assessment of all subsequent bills of entry filed with the claim of preferential rate of duty by the importer, in terms of sub-section (2) of section 17 of the Act, in order to prevent any possible misuse of a trade agreement. The system of compulsory verification of assessment shall be discontinued once the importer demonstrates that he is taking reasonable care, as required under section 28DA of the Act, through adequate record-based controls.

Wilful Mis-statement or Collusion with the Seller

Where it is established that an importer has suppressed the facts, made wilful mis-statement or colluded with the seller or any other person, with the intention to avail undue benefit of a trade agreement, his claim of preferential rate of duty shall be disallowed and he shall be liable to penal action under the Act or any other law for the time being in force.

Authorized Signatories

The Rules of Origin under various trade agreements lay down the format of the certificate of origin, the period of validity, manner of obtaining the certificate and the procedure for verification of origin. One of the usual conditions for accepting the certificate is that it should be signed by the authorized signatories whose name, signature and seal have been communicated by the partner country through agreed channels. At present, the signatures and seals are received by the Board, either directly from the government of the partner country or through the Department of Commerce.

The Directorate General of Systems has built an online repository on ICES for storing the signatures/seals to facilitate comparison by the assessing officers. DRI has been tasked with uploading the data in the database.

The CAROTAR 2020 shall come into force on 21st September, 2020, to provide sufficient time for transition and to ensure that the prescribed conditions in terms of rule 4 are compiled with. Necessary modifications in bill of entry format are being made to allow declaration in terms of rule 3(a) and 3(d) of CAROTAR, 2020.

Technical Terms Used

Each trade agreement, however, has its own set of Rules of Origin, and precise definition of each of the term listed below may vary. Importers are, therefore, advised to refer to the respective Rules of Origin also, as notified in terms of sub-section (1) of section 5 of the Customs Tariff Act, 1975.

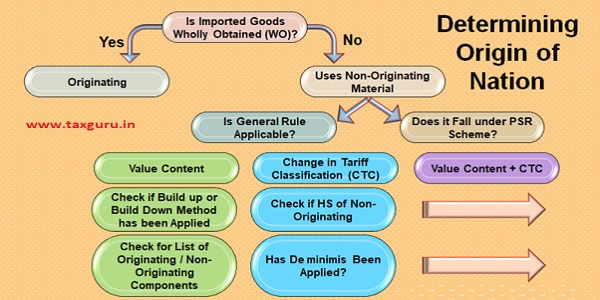

i. Goods Wholly Obtained (WO):Goods produced or obtained without any non-originating input material incorporated.

ii. Goods that are produced using non-originating materials,i.e. not Wholly Obtained, are required to undergo substantial transformation in a country for the good to be qualified as originating. This criterion can be met using following method in combination or standalone, depending upon the criteria assigned for a good,-

(a) Change in Tariff Classification (CTC);

(b) Regional or Domestic Value Content (RVC/DVC); and

(c) Process rule.

iii. Value Content Method: This rule requires that a certain minimum percentage of the good’s value originates in a country for the good to be considered as originating. The components of value and formula for calculating such value addition may vary from agreement to agreement.

iv. Change in Tariff Classification (CTC) Method: To qualify under this origin criterion, non-originating materials that are used in the production of the good must not have the same HS classification (e.g. Chapter level, Heading level or Sub Heading Level as may be required in the Rules of Origin) as the final good. Depending on the Trade Agreement requirements, the good would have to undergo either a change in Chapter (CC), Heading (CTH) or Sub Heading level (CTSH) in order to qualify for preferential treatment under the FTA. Producers and/or exporters should know the HS classification of the final good and the non-originating raw materials.

v. Process Rule Method: This rule requires the good which is being considered as originating, to be produced through specific chemical process in the originating country.

Note: Same good may be assigned different originating criteria in different trade agreements.

vi. General Rule vs Product Specific Rule (PSR): Many trade agreements have a single rule for all goods that are produced using non-originating materials. In some agreements, for some or all tariff headings there are Product Specific Rules (PSRs). Depending on the HS classification of the good, it needs to be seen which criteria has been used to claim origin.

vii. De minimis: This provision allows that non-originating materials that do not satisfy an applicable rule may be disregarded, provided that the totality of such materials does not exceed specific percentages in value or weight of the good. This provision may or may not be there in an agreement and the percentage also varies from agreement to agreement.

viii. Cumulation/ Accumulation: The concept of “accumulation”/”cumulation” allows countries which are part of a preferential trade agreement to share production and jointly comply with the relevant rules of origin provisions, i.e. a producer of one participating country of a trade agreement is allowed to use input materials from another participating country without losing the originating status of that input for the purpose of the applicable rules of origin. Otherwise said, the concept of accumulation/cumulation or cumulative rules of origin allows products of one participating country to be further processed or added to products in another participating country of that agreement. The nature and extent of such cumulation is defined in an agreement and may vary from agreement to agreement. Cumulation can be bilateral, regional, diagonal, etc.

ix. Indirect/Neutral elements refer to material used in the production, testing or inspection of goods but not physically incorporated into the goods, or material used in the maintenance of buildings or the operation of equipment associated with the production of goods. For example, energy and fuel, plant and equipment, goods which do not enter into the final composition of the product, etc. Depending upon the trade agreement, these elements may be treated as originating or non-originating.

x. Rule on treatment of packages and packing materials for retail sale: Such rule provides the manner in which such material will be treated while calculating qualifying value content or tariff shift.

xi. Direct Consignment: Most agreements lay down the condition that good claiming originating status of a country should be directly transported from that country to the importing country. Certain relaxation may be provided in a trade agreement, subject to presentation of certain documents.

Criterion for Rules Origin

There is wide variation in the practice of governments with regard to the rules of origin.

While the requirement of substantial transformation is universally recognized, some governments apply the criterion of change of tariff classification, others the ad valorem percentage criterion and yet others the criterion of manufacturing or processing operation.

Comments :

These Rules are much awaited to establish clear, transparent, and fair administration of Rules of Origin under various bilateral trade agreements signed by India with world economies. These rules would make it clear for the businesses in India and abroad to know the exact procedures that would be adopted by the proper officer while evaluating the preferential rate of duty under trade agreements and the process for verification of certificate of origin. The rules of origin also to ensure that only goods originating in partner countries enjoy tariff or other preferences and also other Tariff related measures like Anti-Dumping Duty and Safeguard Duty are effectively Implemented.

As per the New Provisions origin related information like country of origin criteria, regional value content and product specific criteria etc. must be possessed by the importer and measures are also built in for Counter Verification and Penal Provisions to check the wrong practice of availing concessional customs duty on goods actually originated from Non-Preferential Country and routing such exports to India through preferential trade countries.

Though practically it may be very difficult for genuine importers to comply with these requirements to avail the benefits, in the overall interests of the Nation, it is very Essential to Protect Domestic Industry to encourage Atmanirbar Abhiyan.

*****

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST & Foreign Trade Consultant, Practitioner, International Corporate Trainer & Author.

Available for Corporate Trainings & Consultancy

Can be reached @ snpanigrahi1963@gmail.com

Author Bio

FTA CERTIFICATE MENTIONE THE HSN CODE FIRST 6 DIGIT ARE CORRECT OANOTHER 2 DIGIT WRONGLY MENTIOONED FROM THE FOREGIN SUPPLIER. THIS IS ELIGIBLITY OF COO BENEFIT OR NOT.. IF ANY PUPLIC NOTICE OR CIRUCLARE ISSUED ANY CUSTOMS AUTHORITIES…. PLS CLARIFY…

Sir,

I am importing a finshed plastic product from Malaysia, wherein the raw material i.e. PP and / or HDPE obtained from Singapore and Thailand.

The FOB price comprises of 40-45% raw material and balance is the process +labour+overheads +profits so about 55–60 %.

HS code of raw material is 390120 and 390210 and that of the finshed goods is 392390.

My querry is :

Do we come under Originating or Non Originating Materials,

Is Deminimus applicable to us ?

Is Cumulation applicable to us. If Yes then in waht manner and exent ?

Is CTC applicable to us

is PSR appliable to us . if Yes then whcih rule ?

Is Orgigin criteria based on value content ?

Please advise.

Prashant, Pune.