OVERVIEW OF THE INSOLVENCY AND BANKRUPTCY CODE (AMENDMENT) ORDINANCE 2018

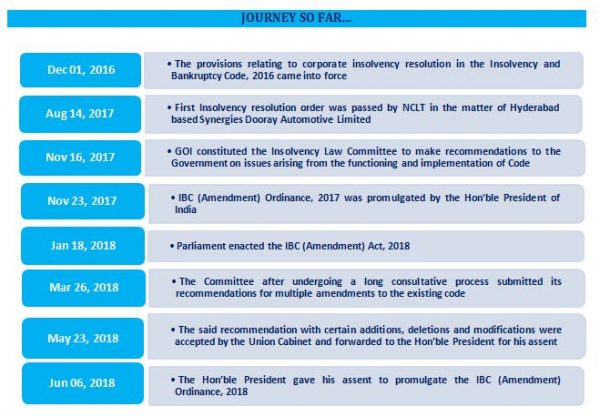

In furtherance of the Government of India’s continuous efforts in facilitating “ease of resolving insolvency in India”, maximising value of assets locked up in NPAs, protecting the interest of various Creditors, the Hon’ble President on June 06, 2018 gave his assent to promulgate the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2018. These Sections shall come into force with immediate effect. An attempt has been made in this document to shed light on the key changes in the insolvency legislation.

A BIRD’S EYE VIEW OF THE NOTIFIED AMENDMENTS

| SECTION NO. & TITLE | AMENDMENTS/CHANGES | ||||||

| Sec 3 – Definitions | 1. In the definition of term ‘default’ the word ‘repaid’ shall be substituted with the word ‘paid’.

• The meaning of the term ‘repay’ is narrow in scope meaning “to pay back” or “refund” and the term ‘repayment’ means “the act of repaying. Whereas, the word ‘payment’ is a wider term which may include even other dues to banks like taxes and cesses. |

||||||

| Sec 5 – Definitions | 1. ‘Corporate Guarantor’ has now been defined to mean a corporate person who is the surety in a contract of guarantee to a corporate debtor.

2. Definition of ‘Financial Debt’ has been amended. Now, any amount raised from allottees under a real estate project shall be deemed to be an amount having commercial effect of a borrowing and hence allottees under a real estate project will now be treated as ‘financial creditors’ under the Code. • Earlier, non-inclusion of home buyers within either the definition of ‘financial’ or ‘operational’ creditors was a cause of worry since it deprived them of: a) the right to initiate the Corporate Insolvency Resolution Process (“CIRP”) b) the right to be on the Committee of Creditors (“CoC”) and the guarantee of receiving at least the liquidation value under the resolution plan. • Amounts so raised under home buyer contracts are a significant amount, and used as a means of financing the real estate project. • Also, the amount of money given by home buyers as advances for their purchase is usually very high, and frequent delays in delivery of possession may thus, have a huge impact. • In Chitra Sharma v. Union of India the amount of debts owed to home buyers, which was paid by them as advances, was claimed to be Rs. 15,000 Crore, more than what was due to banks. Despite this, banks are in a more favorable position under the Code since they are financial creditors. • Similar judgments in Anil Mahindroo & Anr v. Earth Organics Infrastructure and Nikhil Mehta and Sons (HUF) v. AMR Infrastructure Ltd paved way for this amendment. 3. In the definition of operation debt the word ‘repayment’ has been substituted with the word ‘payment’ for the reasons mentioned above. 4. The term ‘related party’ in relation to an individual has now been specifically defined. • Several Sections of the code and regulations use the term ‘related party’ w.r.t an individual but the same was not defined. Hence, this amendment. |

||||||

| Sec 7 – Initiation of CIRP by financial creditor | 1. Now, even a guardian of a financial creditor, administrator or executor of estate of a financial creditor or debenture trustee and the like may trigger insolvency of a corporate debtor, and be a part of the CoC. | ||||||

| Sec 8 – Insolvency resolution by operational creditor

|

1. The definition of the term ‘dispute’ has been amended to even include such disputes which are not pending in a suit or arbitration proceedings.

• Earlier, the definition had an anomaly which implied that there must be existence of dispute + a pending suit / arbitration before triggering of the insolvency process. • The Hon’ble Supreme Court in the matter of Mobilox Innovations Private Limited v. Kirusa Software Private Limited held that the dispute must be existing prior to the receipt of the notice but need not be pending in a suit or arbitration proceeding. |

||||||

| Sec 9 – Application for initiation of corporate insolvency resolution process by operational creditor | 1. The requirement for operational creditors to submit a certificate from a financial institution has been made optional.

• The Hon’ble Supreme Court in Macquarie Bank Limited v. Shilpi Cable Technologies Ltd held that Section 9(3)(c) of the Code is an optional requirement and an alternate understanding would make it discriminatory. • The definition of ‘financial institution’ under Section 3(14) does not include foreign banks and non-scheduled banks, thus creating a void for filing of applications by creditors with such banks. • The process of availing such certification may be cumbersome if the creditor has multiple bank accounts. • Banks presently do not have a format for providing such certification which may lead to denial of such certification by banks. • Most importantly, certificate is not a conclusive proof of the relevant operational debt having been satisfied, as the financial institution may not have the details to map whether the entry in their records is in relation to the payment of the particular debt in question. 2. Now operational creditor shall submit as proof of its debt, available records with an Information Utility or such other proof confirming that there is no payment of an unpaid operational debt by the corporate debtor. |

||||||

| Sec 10 – Initiation of Corporate Insolvency Resolution process by Corporate applicant | 1. Corporate Debtor shall now get special resolution passed by its shareholders or a resolution passed by at least 3/4th of the total number of its partners, as the case may be, for filing of the CIRP application.

• It appeared that many CIRP applications filed on behalf of the Corporate Debtor under the Code were made without an underlying shareholders/partners approval. • Commencement of CIRP is a major decision for the corporate debtor and may have a huge impact on its functioning or even lead to its liquidation. Hence, this amendment. 2. The presence or absence of pending disciplinary proceedings against the proposed Resolution Professional shall now be a ground for acceptance or rejection of application for CIRP filed by the corporate applicant. • Earlier such condition was there only when CIRP applications were filed by financial or operational creditors. |

||||||

| Sec 12 – Time-limit for completion of insolvency resolution process | 1. For extension of CIRP period the COC voting threshold is reduced from 75% to 66% of voting share.

• The high threshold of 75% of voting share was proving to be a road-block. Hence, a suitable amendment has been made to reduce the same to 66% of voting share. |

||||||

| Sec 12A – Withdrawal of application admitted under Section 7, 9 or 10 | 1. The Adjudicating Authority (referred to as ‘AA’ in rest of the Article) may allow withdrawal of CIRP application post admission with the approval of 90% voting share of CoC

• Prior to this, there was no provision in the Code or the CIRP Rules in relation to permissibility of withdrawal post admission of a CIRP application. However, a consistent pattern that emerged in many CIRP cases was that for a settlement between applicant creditor and the debtor leading to withdrawal of CIRP post admission, consensus was also required amongst all creditors and the debtor. |

||||||

| Sec 14 – Moratorium | 1. The scope of the moratorium may be restricted to the assets of the Corporate Debtor only and Moratorium shall not be applicable to a surety in a contract of guarantee to a corporate debtor.

• Since many guarantees for loans of corporates are given by its promoters in the form of personal guarantees, if there is a stay on actions against their assets during a CIRP, such promoters (who are also corporate applicants) may file frivolous applications to merely take advantage of the stay and guard their assets.

|

||||||

| Sec 15 – Public announcement of corporate insolvency resolution process | 1. Now, IBBI is vested with the power to specify the last date for submission of claims.

• Different Sections and CIRP regulations have provided for different period for submission of claims. Since the nuances regarding submission of claims, constitution of the CoC, verification of claims, etc. are captured in the CIRP Regulations, it is now decided to vest such powers with IBBI to provide for flexibility |

||||||

| Sec 16 – Appointment and tenure of interim resolution professional

|

1. Now, IRP to continue till the appointment of the RP.

• Section 16(5) of the Code provided that the term of the IRP shall not exceed 30 days from the date of his appointment and Regulation 17(1) of CIRP Regulations states that the IRP is required to file a report certifying the constitution of CoC on or before the expiry of 30 days from the date of his appointment. • Whereas, Regulation 17(2) requires a meeting of the CoC to be convened within 7 days of filing the report. • This had led to an anomaly whereby the term of the IRP ends on the 30th day from the date of his appointment and the meeting may not be called till the 37th day, leading to a period during the CIRP where a professional is absent. Hence, this amendment. |

||||||

| Sec 17 – Management of the affairs of the corporate debtor by IRP | 1. The IRP will also be responsible for complying with the statutory requirements under applicable laws while managing the affairs of the corporate debtor during CIRP.

• To avoid any ambiguity, ‘management of corporate affairs’ also includes responsibility for statutory compliances. |

||||||

| Sec 21- Committee of Creditors (CoC) | 1. Authorised Representatives of financial creditors who are related parties to the corporate debtor are now disqualified from participating in the CoC.

2. However, a carve out has been provided for financial creditors that are regulated by a financial sector regulator and have become a related party of the corporate debtor solely on account of conversion or substitution of debt into equity shares of the corporate debtor, prior to the insolvency commencement date. • There might be a situation where the financial creditor holding a large portion of financial debt in the corporate debtor was excluded from the CoC on account of equity or preference shares of the corporate debtor held by it pursuant to a previous debt restructuring for sustainable structuring of stressed assets which enabled financial creditors such as banks to convert part of their debt into equity in the borrower. Therefore, it would be unfair to deny such pure play financial creditors representation or voting rights in the CoC formed under the Code on account of equity held by them pursuant to debt restructuring schemes implemented in the past. 3. Persons other than the financial creditors shall not be a part of the CoC for the purposes of representation and voting • Earlier it was provided that creditors in respect of certain debts issued as securities, may choose to be present in the meetings themselves or appoint a single trustee, agent, to act and vote on their behalf. 4. Manner of participation and voting in the CoC provided for, where the financial debt- (i) is in the form of securities and deposits (ii) is owed to a class of creditors (other than under consortium arrangement or syndicated facility) exceeding the specified number; (iii) is represented by a guardian, executor or administrator. • There was a need of mechanism for providing mode of representation in meetings of security holders, deposit holders, and all other classes of financial creditors which exceed a certain number, through an authorised representative. Hence, this amendment. 5. The decisions of routine nature shall require approval from 51% of voting share of CoC instead of present provision requiring approval from 75% of voting share. |

||||||

| Sec 22 – Appointment of resolution professional | 1. Voting threshold for obtaining the approval of the CoC for appointment of RP reduced from 75% to 66% of voting share.

• The high threshold of 75 percent of voting share of financial creditors for decisions of the CoC was proving to be a road-block in the resolution process. Effectively, as a result of the high threshold, blocking the resolution plan and other decisions of the CoC, was easier than approving these. 2. Now, it is required to obtain consent of an IRP to continue as RP or for appointment of RP. |

||||||

| Sec 23 – Resolution professional to conduct the corporate insolvency resolution process | 1. RP shall continue to manage the operations of the corporate debtor after the expiry of the CIRP period post submission of the resolution plan, until an order is passed by the AA.

• Currently, the RP is responsible to manage the Corporate Debtor only during the CIRP i.e., 180/270 days as the case may be. However, there was no guidance in the Code regarding the responsibility management after the CIRP process until an order was passed by the AA. |

||||||

| Sec 25A – Rights and duties of authorised representative of financial creditors | 1. The new Section provides for the rights and duties of the authorised representatives of financial creditors.

Few salient features of the provision are as follows: a) The authorised representative shall have the right to participate and vote in the meeting of the CoC on behalf of the financial creditors it represents. b) It shall be the duty of the authorised representative to circulate the agenda and minutes of the meeting of the CoC to the financial creditors it represents c) The authorised representative shall not act against the interest of the financial creditors it represents. |

||||||

| Sec 27 – Replacement of resolution professional by committee of creditors | 1. The threshold for replacing the existing RP appointed with another RP has been reduced from 75% to 51% of voting share, subject to a written consent from the latter. | ||||||

| Sec 28 – Approval of committee of creditors for certain actions | 1. The threshold for voting for all actions under this Section such as raising of interim finance, create any security interest over the assets of corporate debtor, undertake any RPT etc. has been reduced from 75% to 51% of voting share. | ||||||

| Sec 29A – Persons not eligible to submit resolution plan | 1. Account must be Non performing asset (“NPA”) at the time of submission of the resolution plan.

2. Financial creditor which is not a related party to the corporate debtor and holding convertible securities therein not to be disqualified from submitting resolution plan. • Taking into consideration the nature of business of financial entities such as ARCs, AIF, FII, FVCI etc. they are likely to be related to Companies that are classified as NPA and consequently be disqualified. Hence these pure play financial entities have been exempted from disqualification u/s 29A(c). 3. No disqualification under this section for resolution applicants with an NPA account, if such account was acquired pursuant to a prior resolution plan approved under this Code for a period of 3 years from the date of approval of such prior resolution plan by the AA. • In order to ensure that the underlying objective of the Code to promote resolution is furthered, resolution applicants who hold NPA accounts solely due to acquisition of corporate debtors under the CIRP, must be given some time to revive the corporate debtor without being disqualified from bidding for other corporate debtors if they fulfill all other criteria. In this regard, a period of Three (3) years has been provided for suspending the disqualification under section 29A(c). 4. A Person is disqualified from filing resolution plan for a period of Two (2) years from the date of his release from imprisonment if he has been convicted for Two (2) years or more for offences under the Acts listed in the Schedule XII or for Seven (7) years or more under any other law for the time being in force. • Earlier disqualification norms were of a very wide criterion which may cast within its net offences which have no nexus with the ability to run a corporate debtor successfully. 5. Exemption from disqualification has been provided to a connected person of a disqualified Director. • Keeping in mind that the disqualification based on extant criterion also extends to connected persons of the resolution applicant, a need was felt to narrow down the scope of this clause. 6. No disqualification for a resolution applicant who has acquired a corporate debtor in which a preferential, undervalued, extortionate credit transaction or fraudulent transaction has taken place prior to the acquisition of the corporate debtor pursuant to a resolution plan approved under the Code or pursuant to a scheme or plan approved by a financial sector regulator or a court of law and has not otherwise contributed to such transaction/s. • The probable reasons is that a person must not be punished for acts of its predecessors if it had no nexus with such past acts that led to the preferential, undervalue, fraudulent or extortionate credit transaction. 7. It is specified that the disqualification is applicable only if the guarantee has been invoked by the creditor and dishonoured by the guarantor. • Intent of the provision could not have been to disqualify every guarantor only for the reason of issuing an enforceable guarantee as that would be discriminatory. Hence, the suitable amendment. |

||||||

| Sec 30 – Submission of resolution plan

|

1. The resolution plan submitted by RP deemed posses shareholder approval required under the Companies Act, 2013 or any other law for the time being in force

2. The voting threshold for approving the resolution plan has been reduced from 75% to 66% of voting share. • Earlier, owing to higher threshold, only 9 out of 30 cases went into liquidation on account of rejection by the CoC. 3. Clarification has been provided that the eligibility criteria in section 29A as amended by this Ordinance, shall be applicable to resolution applicants that have not submitted resolution plans on the date of coming into force of this Ordinance. |

||||||

| Sec 31 – Approval of the resolution plan | 1. The AA shall, before passing an order of approval of resolution plan, ensure that the resolution plan has a satisfactory implementation plan.

2. Specifically provided that necessary approvals required under any law for the time being in force, may be obtained within a period of One (1) year from the date of approval of the resolution plan or such time as is specified in the relevant law for obtaining such approvals, whichever is later. |

||||||

| Sec 33 – Initiation of liquidation | 1. The threshold for obtaining the approval of the CoC for making an application to the AA to pass a liquidation order has been reduced from 75% to 66% of voting share. | ||||||

| Sec 34 – Appointment of liquidator and fee to be paid | 1. There is now a requirement to obtain consent of an RP to continue as a liquidator.

2. The AA shall by order replace the RP if the RP fails to submit written consent. 3. There is now a requirement to obtain consent of an Insolvency Professional to act as the liquidator. |

||||||

| Sec 42 – Appeal against the decision of Liquidator | 1. Now, even those claims which have been accepted by the liquidator may be appealed.

• Earlier, only those Creditors whose claims have been rejected by liquidator had right of appeal to AA under Section 42. However, there was no scope for appeal based on disputes in accepted claims, say, in terms of valuation or any other ground. • Providing a right to a creditor to challenge such accepted claims may be essential, especially since liquidation may be the last resort for recovery of debt. |

||||||

| Sec 60 – Adjudicating Authority for corporate persons | 1. If any application for CIRP or liquidation of a corporate debtor is pending before an AA, then an application for insolvency resolution or liquidation or bankruptcy, as the case may be, of a corporate guarantor or personal guarantor of such corporate debtor must be filed before the same AA.

2. The proceeding for insolvency resolution, liquidation or bankruptcy, as the case may be, of a corporate guarantor or personal guarantor of a corporate debtor pending in any court or tribunal shall stand transferred to the AA dealing with the insolvency resolution process or liquidation proceeding of such corporate debtor. • Section 60 provides a link between corporate debtor and personal guarantor but no such link is present between the insolvency resolution or liquidation processes of the corporate debtor and the corporate guarantor. Hence, this amendment. |

||||||

| Sec 238A – Limitation | 1. The provisions of the Limitation Act, 1963 shall, as far as may be, apply to proceedings or appeals under the Code before the AA or the NCLAT, as the case may be.

• The intent was not to package the Code as a fresh opportunity for creditors and claimants who did not exercise their remedy under existing laws within the prescribed limitation period. Hence a specific section applying the Limitation Act to the Code. |

||||||

| Sec 240A – Application of this code to micro, small and medium enterprises | 1. Central Government has been empowered to exempt or vary application of provisions of the Code for MSMEs.

• The introduction of such a Section will be beneficial for MSMEs, in public interest while preserving the overall scheme and objective of the Code. |

Disclaimer: This material and the information contained herein is prepared by Corporate Updates Team of RANJ & Associates, Company Secretaries, Hyderabad. The above information is only indicative and solely for informational purpose and private circulation. RANJ & Associates, Company Secretaries intend to, but do not guarantee or promise that it is correct, complete / up to date. We expressly disclaim any liability to any person in respect of anything, and of consequences of anything done, or omitted to be done by any such person in reliance upon the contents of this document.

Author CS Rahul Jain is Partner with ‘RANJ & Associates’ and CS Prafful Jain is Associate with RANJ & Associates and can be reached at consult@ranjcs.com .