The concept of LLP, introduced in India through the Limited Liability Partnership Act, 2008 has become a popular form of business entity in India owing to its simplified procedures for registration and maintenance. LLPs allow many of the small and medium-sized to enjoy a separate legal entity, improve transferability and provide its promoters with limited liability protection. Therefore, there is tremendous interest among small business owners and service providers to register their business as an LLP.

With the Indian population currently spread across the globe and growing interest among foreigners to get a foothold into the Indian market, there is a lot of interest for Foreign Direct Investment (FDI) in LLP. Similar to FDI in Private Limited Company, it determines the policy for FDI in LLP by the yearly FDI Circular issued by the Department of Industrial Policy and Promotion (DIPP), Ministry of Commerce and Industry.

FDI policy on LLPs was amended in 2015 to provide that investments in LLPs will not require Government approval. 100% FDI is now permitted under the automatic route in LLPs operating in sectors/activities where 100% FDI is allowed, through the automatic route and there are no FDI-linked performance conditions (i.e., sector specific conditions for investee company).

Eligible Form of FDI

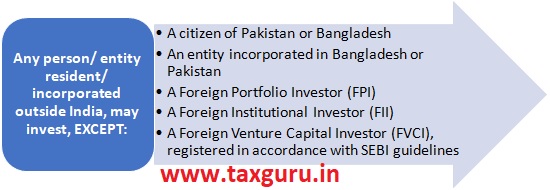

A person resident outside India or an entity incorporated outside India, may invest, either by way of capital contribution or by way of acquisition/ transfer of profit shares in the capital structure of an LLP.

Eligible Investors

Eligibility of an LLP

FDI in LLPs is permitted under automatic route, subject to the following conditions:

- LLPs must be operating in sectors/ activities where 100% FDI is allowed through the automatic route and there are no FDI linked performance conditions.

For ascertaining such sectors, reference shall be made to Annex B to Schedule 1 of Foreign Exchange Management (Transfer or Issue of Security by a Person Resident outside India) Regulations, 2000.

- FDI in LLP is subject to the compliance of the conditions of Limited Liability Partnership Act, 2008.

Downstream Investment in LLP

Downstream investment means indirect foreign investment, by an eligible Indian entity (which is owned and controlled by persons resident outside India), into another Indian company/LLP, by way of subscription or acquisition.

An Indian company or an LLP, having foreign investment, shall be permitted to make downstream investment in an LLP engaged in sectors in which 100% FDI is allowed under the automatic route and there are no FDI linked performance conditions.

Onus of compliance shall be on the LLP accepting downstream investment to ensure compliance with the above conditions.

Conversion

Conversion of an LLP having foreign investment and operating in sectors/activities where 100% FDI is allowed through the automatic route and there are no FDI-linked performance conditions, into a company is permitted under automatic route.

Further, a company having foreign investment can be converted into an LLP under the automatic route only if it is engaged in a sector where foreign investment up to 100 percent is permitted under automatic route and there are no FDI linked performance conditions.

Pricing of Investment

- FDI in a LLP either by way of capital contribution or by way of acquisition/ transfer of profit shares, would have to be more than or equal to the fair price as worked out with any valuation norm which is internationally accepted/ adopted as per market practice (hereinafter referred to as “fair price of capital contribution/ profit share of an LLP”) and a valuation certificate to that effect shall be issued by the Chartered Accountant or by a practicing Cost Accountant or by an approved valuer from the panel maintained by the Central Government.

- In case of transfer of capital contribution/ profit share from a resident to a non-resident, the transfer shall be for a consideration equal to or more than the fair price of capital contribution/ profit share of an LLP. Further, in case of transfer of capital contribution/ profit share from a non-resident to resident, the transfer shall be for a consideration which is less than or equal to the fair price of the capital contribution/ profit share of an LLP.

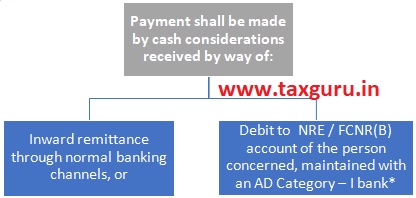

Mode of payment

[* in accordance with Foreign Exchange Management (Deposit) Regulations, 2016, as amended from time to time].

Remittance of Disinvestment proceeds

The disinvestment proceeds may be remitted outside India or may be credited to NRE or FCNR(B) account of the person concerned.

Reporting of FDI

- Single Master Form: With effect from September 01, 2018, an LLP receiving foreign investment for capital contribution and acquisition of profit shares shall submit Single Master Form (SMF) online on https://firms.rbi.org.in/ within 30 days from the date of receipt of the amount of consideration. Prior to introduction of SMF, the reporting was required to be made in Form LLP(I).

- Annual Return on Foreign Liabilities and Assets:LLP which has received investment by way of capital contribution in the previous year(s) including the current year, shall submit form FLA to the Reserve Bank on or before the 15th day of July of each year.

Also, the disinvestment/ transfer of capital contribution or profit share between a resident and a non-resident (or vice versa) shall be reported in SMF within 60 days from the date of receipt of funds, earlier such reporting was required to be made in Form LLP(II).

Conclusion

LLP structures have long been in use globally and have proven to be specifically advantageous for professionals to come together under its umbrella and work seamlessly without being burdened with the compliance requirements of a company or the personal exposure involved in a partnership firm. By allowing FDI investments into LLPs, India has taken a bold step in the right direction as it would provide foreign investors an alternate form of business other than the company and would entitle them to benefit with inherent flexibility & tax efficient LLP structure. This move will boost the number of joint ventures in the country, with their corresponding benefits as employment opportunities, and improved technologies.

About the Author

Author is Neeraj Bhagat, FCA helping foreign companies in setting up and closure of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. He is also founder of Neeraj Bhagat & Co. Chartered Accountants; a Chartered Accountancy firm established in the year 1997 with its head office at New Delhi.

Author is Neeraj Bhagat, FCA helping foreign companies in setting up and closure of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. He is also founder of Neeraj Bhagat & Co. Chartered Accountants; a Chartered Accountancy firm established in the year 1997 with its head office at New Delhi.