Introduction

A contract of Guarantee is the undertaking of a promise by the promisor to perform the promise of a third person in order to discharge them of their liability, in case of the latter’s default. The “surety” gives the guarantee in case the “principal-debtor” defaults , to indemnify or to make the “creditor” whole again. It is important to note that a Contract of Guarantee is an independent contract with respect to the primary contract between the creditor and the principal debtor as specified under Section 126 of the Indian Contract Act, 1872. It is a contract of strictissimi juri.

Who is a Financial Creditor ?

The Insolvency Bankruptcy Code, 2016 (‘Code’) distinguishes a financial creditor from other types of creditors. Section 5(7) of the Code defines Financial Creditors as “any person to whom a financial debt is owed and includes a person to whom such debt has been legally assigned or transferred to.” The voting rights of a financial creditor is also based purely on the proportion of the financial debt, mentioned under Section 5(28) of the Code.

Creditors usually favor the status of a “financial creditor” because in the case of a default, the financial creditor gets voting rights on all key decisions during the corporate insolvency resolution process (‘CIRP’) and liquidation of an insolvent company. That is why third-party secured creditors have filed petitions in various judicial forums which have reportedly been handled on a case-by-case basis, with a dearth of evidence on the general threshold for such decisions.

Section 172 of the Indian Contract Act implies that a pledge is defined through the objective of the contract. Where the object of the delivery of goods is to provide a security for a loan or for the fulfillment of an obligation, that kind of bailment is called pledge. Pledge is a bailment of personal property as a security for some debt or engagement. The ‘pledgor’ refers to the party providing the pledge which in this case is he third party security provider. The ‘pledgee’ is referred to the party to which the pledge is granted also known as the ‘Lender’. Finally the ‘secured obligations’ refers to the obligations that are to be secured by the pledge.

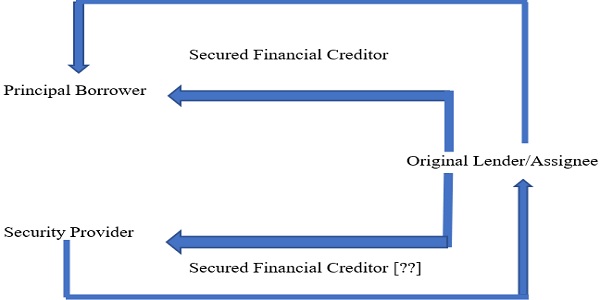

Third Party Security : Secured Creditor or Financial Creditor ?

Grerard McCormack in his book ‘Secured Credit under English and American Law’ states that when a company is undergoing CIRP, there is by definition, an insufficient pool of money in the corporate purse to provide satisfaction, and the fundamental principle of insolvency is ‘equality of misery’ or equal treatment for all creditors – pari passu distribution of available assets among all the creditors.

In the case of Phoenix ARC Pivate Limited v Ketulbhai Ramubhai Patel, the Resolution Professional of Doshion Water Solutions Private Limited, Doshion Water Solution pledged certain number of shares of Gondwana Engineers Limited (‘GEL’) , in favor of Phoenix ARC Private Limited (Assignee of the loan) for the loan advanced by the pledgee to Doshion Limited. When The Supreme Court was called upon to assess whether the pledgee would be a financial creditor of the pledgor firm, which was the corporate debtor. In other words, whether the corporate debtor owed any financial debt to the appellant so as to treat the appellant as a financial creditor. The National Company Tribunal held that pledge under the definition of ‘financial debt’ in the Code, will not be analogous to “disbursement of any amount against the consideration for the time value of money”. The Court held that , Phoenix Arc Limited cannot be considered as a ‘financial creditor’ of Doshion Limited in this case.

The Supreme Court rejected the Appellants’ present appeal on two grounds –

a. the Corporate Debtor did not enter a contract of guarantee as defined in Section 126 of the Indian Contract Act. The reasoning that followed was that the debtor never promised to perform or discharge the liability of the borrower in the case of a default. The Pledge Agreement executed between Doshion Limited and GEL was only limited to the pledge of 40,160 shares of GEL, as security. Hence, a pledge agreement never surfaced to exist.

b. The court further echoed their observation in Jaypee Infratech Limited v Axis Bank Limited , where this Court was faced with a similar question related to the status of the lenders of respondent – Jayprakash Associates Ltd. (‘JAL’) and if they could be considered as financial creditors of the corporate debtor – Jaypee Infratech Ltd. (‘JIL’). This question was splayed over the mortgages created by corporate debtor as collateral securities of its holding company – JIL. Therefore, it held that if an individual has only security interest over the assets of the borrower or even if the person falls within the definition of a ‘secured creditor’ due to the collateral pledged in their favour by the borrower, as opposed to merely relying on the borrower’s ability to generate cashflows to discharge their liability, they would not be considered as ‘financial creditors’ by sub-section (7) and (8) of Section 5 of the Code.

Earlier in 2018, the National Company Law Tribunal (‘NCLT’), Allahabad, refused to address the issue of the status of a third-party security holder to a corporate debtor under the Code, in the case of ICICI Bank Limited v. Anuj Jain (Resolution Professional of Jaypee Infratech Limited). The NCLT negated ICICI Bank Limited’s contention that it should be considered a financial creditor to its corporate debtor, Jaypee Infratech Limited. So if a third-party mortgagee is considered a financial creditor of a corporate debtor, then the third party mortgagee will have the benefit of being considered as a creditor in the committee of creditors upon the filing of a claim, which will provide all the protections available to such creditors. It would also allow creditors to reach a comprehensive agreement because the resolution plan would be binding on the third-party mortgagee as they would be included in the committee of creditors and considered a stakeholder. Subsequently implying that a resolution plan could recommend modifying the mortgage or releasing the mortgage and satisfying the creditor’s payment obligations.

Third Party Security not a Financial Creditor: An Anomaly

Despite the fact that the ruling in both the cases affirms that a third-party mortgagee or a third-party pledgee is not a financial creditor, we believe that the third-party mortgagee would be entitled to the rights of a secured creditor in the event of the corporate debtor’s liquidation. A secured creditor is entitled to a distribution during the liquidation process under Section 53 of the Code. A secured creditor also has the option of enforcing its security separately under Section 52 read with Section 141 of the Indian Contract Act which gives the surety the right to the benefit of any security which the creditor has against the principal debtor at the time when the contract emerges into existence. More aptly explained in the Illustration (a) of Section 141. Fundamentally, a Secured Creditor is a creditor in whose favour a security interest is created, not as a creditor securing only “financial debt” as defined by the Code.

The verdict in Jaypee Infratech which deliberated whether third-party security holders can be considered as “financial creditors” was obiter dicta. The judgement produced in Phoenix Arc then seems to be a simple re-iteration of the Jaypee Infratech case, however, since the Phoenix Arc case was decided by a larger bench , its ruling will carry more precedential value under the principles of stare decisis. The Supreme Court’s determination of the third-party security holder’s status through the above mentioned case laws has had important implications in the banking, credit and security fields. In the event that the supplier of the security goes into insolvency under the Code, an independent third-party security is not ideal for the holder of such security. A feasible alternative solution is that the third-party security can be constructed in such a way that it supports a guarantee. For example , party A must first provide a guarantee in favour of B to ensure that party C fulfils his duties to B. Party B can secure its guarantee by establishing a mortgage (as in the case of Jaypee Infratech) or pledging shares (as in the case of Phoenix Arc)or any other form of security. Even if there is no disbursement of funds from party B to party A that come within the ambit of the definition of “financial debt” under section 5(8) of the Code. It would categorise such transactions as a guarantee under sub-section (i) of section 5(8), which reads as the following –

“Section 5(8) “financial debt” means a debt along with interest, if any, which is disbursed against the consideration for the time value of money and includes –

…

(i) the amount of any liability in respect of any of the guarantee or indemnity for any of the items referred to in sub-clauses (a) to (h) of this clause.”

Courts have unequivocally stated that they will not presume the implication of a guarantee in a third-party security agreement. The parties’ next best alternative is to make such guarantees explicit in nature , even though Section 126 of the Indian Contract Act clearly remarks that the contract of guarantee is created when it confers on a person the obligation of performing the promise, or discharging the liability, of a third person in case of default, even if not expressly stated in the contract.

The CIRP vests control of the insolvency process in the hands of a resolution professional, who is answerable to the Committee of Creditors (‘CoC’). The voting membership is restricted to the CoC which is constituted by financial creditors. While the Supreme Court has delegated that the CoC should treat all creditors equitably, the recent judgements concerning the status of third party creditors as financial creditors not only creates different classes of creditors but also gives way to an anomaly by not allowing third parties a say in the resolution plan. It may come to pass that the Committee of Creditors decide to modify or completely eradicate the security interests of a third party. Such a resolution plan would be vulnerable and unfair because it would take away the assets that are secured in favor of the third party pledgee or mortgagee. This creates an unilateral power among the CoC , which leads to decisions that are only in the interests of financial creditors over the interests of third party secured creditors. Such a strong hand in the CIRP only goes to make a bigger comment on the significant perception of the flaw in the “creditor-in-control” model.

Conclusion

Perceptions of the truth are as important as the truth itself. In conclusion, the perception that CoC’s are dominated by financial creditors and as a result other secured creditors are being treated inequitably because they lack the status of a “financial creditor” may hold true as an example. If such a perception becomes widespread then it may undermine the coveted authority and the trust in the CIRP and even the Insolvency Bankruptcy Code as a whole. This may squander the recent progress that India has made in the World Bank’s “Ease of Doing Business Index”.