Introduction

This Article aims to bring clarity on new Section 90 of Companies Act, 2013 (‘the Act) introduced by the Companies (Amendment) Act, 2017 and the Companies (Significant Beneficial Owner) Rules, 2018 (‘the Rules’), notified on 13th June, 2018.

Section 90 had introduced concept of “Significant Beneficial Interest (‘SBI’)” and goes on to talks about “Filing of Return by the Significant Beneficial Owners (‘SBO’) of the Company”, “Maintenance of Register of Interest declared by individuals”, and also specifies fines and penalties for non-compliance.

Important Terms under the Act and Rules

Before understanding the provisions of the Act and the Rules, the following are the Basic Terms to understand the Concept of Ownership Rules:

i. Registered Owner (RO): means a person whose name is entered in the register of members of the company as holder of shares in that company but who does not hold beneficial interest in such shares;

In simple words, such persons are not actual owners of shares. Only their name is entered in the register of members. RO enjoy the following rights, voting rights in the Company, Vote on poll, name shall be entered in register of members, entitled to sign proxy form, shall be counted for the purpose of quorum etc.

ii. Beneficial Owner (BO):Every person holding or acquiring a beneficial interest in shares of a company not registered in his name.

In simple words, BO is the actual owner of the shares. Only his name is not entered in register of members. He is entitled a) To exercise any or all the rights attached to the shares. b) Receive and participate in the dividends and other distributions like Right offer, Bonus Shares, etc.

iii. Beneficial Interest (BI): Beneficial interest in a share includes, directly or indirectly, through any contract, arrangement or otherwise, the right or entitlement of a person alone or together with any other person to;

(i) Exercise or cause to be exercised any or all of the rights attached to such share; or

(ii) Receive or participate in any dividend or other distribution in respect of such share.

(In view of the absence of a definition of beneficial interest in a share in a company, the above stated provision has been newly inserted as subsection 10 of Section 89 of the Companies Act, 2013)

iv. Significant Beneficial Owner (SBO):Every individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holds ultimate beneficial interests of not less than 10%, in shares of the company or the right to exercise, or the actual exercising of significant influence or control over the company.

(Note: For the purpose of calculation of 10% of beneficial interest in shares, shares also Includes, instrument in form of Global Depository Receipts, Compulsorily Convertible Preference Shares or Compulsory convertible debentures.)

Further, for the purpose of Significant Beneficial Owner, in case of ‘person other than individuals or natural person’, shall be determined as under:

| S. No. | Where Member is | Particulars | Percentage |

| 1. | Company | Significant beneficial owner is the natural person, who,

– Whether acting alone or – together with other natural persons, or – through one or more other persons or trust |

Hold atleast 10% of share capital of the Company or Who exercises significant influence or control in the company through other means. |

| 2. | Partnership Firm | Significant beneficial owner is the natural person, who,

– Whether acting alone or – together with other natural persons, or – through one or more other persons or trust |

Hold atleast 10% of capital or Has entitled to not less than 10% of profits of the firm.

|

| 3. | Where no natural person is identified under (A) and (B) mentioned above? | In this case, the SBO is the relevant natural person who holds the position of senior managing official. | – |

| 4. | Trust | The beneficial owner shall includes,

– identification of the author of the trust, – the trustee, – the beneficiaries with not less than 10% interest in the trust and – any other natural person exercising ultimate effective control over the trust through a chain of control or ownership. |

|

The difference between Beneficial Owner (BO) and Significant Beneficial Owner (SBO)

| Beneficial Owner (Sec. 89) | Significant Beneficial Owner (Sec. 90) |

| Every person holding or acquiring a beneficial interest in shares of a company not registered in his name. | SBO means an individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holding ultimate beneficial interest of not less than 10% and whose name is not entered in the register of members of a Company. |

| Beneficial owner is required to make disclosures as per Section 89 even if interest is more than or less than 10%. | Disclosures requirement of SBO shall occur only if interest is at least 10%. |

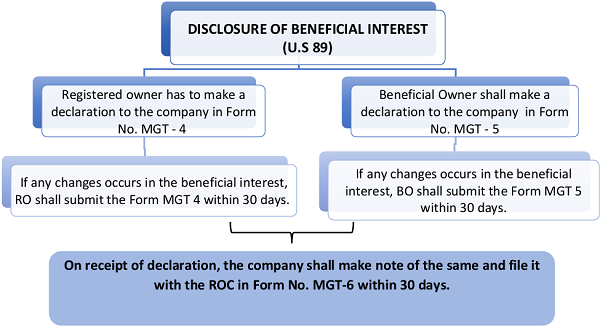

Disclosure of Beneficial Interest under Section 89 of the Act

Section 89 deals with “Declaration in respect of Beneficial Interest in any Share”, As per the Section read with the Companies (Management and Administration) Rules, 2014,

(1) The Registered owner shall make a declaration to the company in Form No. MGT – 4. (Compliance by Registered owner)

(2) Beneficial Owner shall make a declaration to the company in Form No. MGT – 5. (Compliance by Beneficial Owner)

(3) If any change occurs in the Beneficial Interest in such shares, within a period of 30 days of such change, the RO shall make a declaration of the changes to the company in Form No. MGT – 4 and BO to the company in Form No. MGT – 5.

(4) If any person fails to make the above said declaration, without any reasonable cause, they shall be punishable with fine which may extend to Rs. 50,000/-. In case the failure is continuing one, they will face a further fine which may extend to Rs. 1,000/- for every day after the first failure.

(5) The company shall make note of the above declarations and file the same with the ROC in Form No. MGT-6 within 30 days from the date of receipt of such declaration. If the company fails to do so, the company and the officer who is in default shall be punishable with fine not less than Rs. 500/- and can extend up to Rs. 1000/-. In case the failure is continuing one, they will face a further fine which may extend to Rs. 1000/- for every day after the first failure. Also, the Companies are exempted from filing beneficial ownership details with ROC (in Form No. MGT – 6) in respect of a trust which is created, to set up a Mutual Fund or Venture Capital Fund or such other fund as may be approved by the SEBI. (Compliance by the Company)

(6) The rights in relation to shares shall not be enforceable by BO or by any person claiming through him, if the declaration as aforesaid is not made by the BO.

Diagrammatic presentation of Compliances under Sec. 89 and MGT Rules, 2014

Disclosure of Significant Beneficial Interest (SBI) under Section 90 of the Act

Section 90 is applicable to every individual Significant Beneficial Owners holding the SBI as defined above. As per the Section 90 read with the Companies (SBO) Rules, 2018,

(1) SBO shall file a declaration in Form No. BEN-I to the company in which he holds the SBI as on 13.06.2018, within 90 days from the commencement date (i.e by 12.09.2018) and within 30 days in case of any change in the SBI.

(2) Every individual who acquires SBI after 13.06.2018, shall file a declaration in Form No. BEN-I to the company within 30 days of acquiring the SBI or in case of any change in such ownership.

(3) Every company shall file a return of SBO of the company and the changes therein in Form No. BEN-2 with the Registrar (ROC) within a period of 30 days from the date of receipt of declaration by it.

(4) Every company shall maintain a register of interest declared by individuals and changes therein in Form No. BEN-3. The Register shall be open for inspection by any member of the company on payment of fees not exceeding Rs. 50/- for not less than 2 hours during business hours on every working day as the Board may decide.

(5) The Company has the power to give notice in Form No. BEN-4 to any person, whether or not a member, whom the company knows or has reasonable cause to believe –

i. to be a Significant Beneficial Owner of the company;

ii. to be having knowledge of the identity of a Significant Beneficial Owner or another person likely to have such knowledge; or

iii. to have been a Significant Beneficial Owner of the company at any time during the 3 years immediately preceding the date on which the notice is issued, and who is not registered as a Significant Beneficial Owner with the company as required under this section.

(6) The information required by the notice shall be given by the concerned person within a period of 30 days from the date of the notice. If a person fails to give the information required by the notice or where the information given is not satisfactory, within a period of 15 days of the expiry of the period specified in the notice, the Company shall apply to the Tribunal . The company can seek an order from the Tribunal, directing:

a. restrictions on the transfer of interest attached to the shares in question;

b. suspension of the right to receive dividend in relation to the shares in question;

c. suspension of voting rights in relation to the shares in question;

d. any other restriction on all or any of the rights attached with the shares in question

(7) The Tribunal may, after giving an opportunity of being heard, make an order restricting the rights attached with the shares within a period of 60 days of the receipt of application.

(8) If any person fails to make a declaration, he shall be punishable with fine which shall not be less than 1 lakh rupees but which may extend to 10 lakh rupees. In case the failure is continuing one, a further fine which may extend to 1 thousand rupees for every day after first during which failure continues.

(9) If a company fails to maintain a Register or fails to file a return or denies inspection as per this section, the company and every officer of the company who is in default shall be punishable with the fine which shall not be less than 10 lakh rupees. In case the failure is continuing one, a further fine which may extend to 1 thousand rupees for every day after first during which failure continues.

(10) If any person wilfully furnishes any false or incorrect information or suppresses any material information of which he is aware in the declaration made under this section, he shall be liable to action under section 447.

Exemptions from Declaring BI (MCA Notification & Rule 8 of SBO Rules)

First thing to note, Notification GSR 463(E) dated 5th June, 2015 completely exempts government companies from applicability of Sec. 89 and Sec. 90 of the Act. Further, these SBO rules are not applicable for the Holding of Shares of Companies/Body Corporates by pooled Investment Vehicles/Investment Funds such as Mutual Funds, Alternative investment Funds, Real Estate Investment Trusts and Infrastructure Investment Trusts regulated under SEBI Act.

E.g: Alternative investment Funds holds 50% of shares in Zing Ltd and Mr. Anil holds 25% in AIF. In this case, there is a clear exemption to pooled investments under Rule 8 and hence, concept of SBO and disclosures are not applicable.

Diagrammatic presentation of Compliances under Sec. 90 and SBO Rules, 2018

Some Practical Examples for better understanding

Some Practical Examples for better understanding

Problem: Company ‘ABC Ltd’ holding 60% in Subsidiary Company (XYZ Ltd). Mr. Arun, Mr. Bijo and Mrs. Chandra hold 10%, 25% and 40% of shares of Company ‘ABC Ltd’ i.e Holding Company. Whether Mr. Arun, Mr. Bijo and Mrs. Chandra have to declare SBO to the Company XYZ Ltd?

Solution: SBO of Mr. Arun, Mr. Bijo and Mrs. Chandra in ‘XYZ Ltd’ shall be as follow:

| S. No. | Shareholders | Holdings | Actual Interest in XYZ Ltd | BEN-1 |

| 1. | Mr. Arun | 10% | (60*10%) = 6% | No |

| 2. | Mr. Bijo | 25% | (60*25%) = 15% | Yes |

| 3. | Mrs Chandra | 40% | (60*40%) = 24% | Yes |

Problem: What if the Company ‘ABC Ltd’ holds 25% shareholding of Company ‘XYZ Ltd’ and Mr. Arun, Mr. Bijo and Mrs. Chandra holds 50%, 30% and 5% shares of Company ‘ABC Ltd’.

Solution: Interest of Mr. Arun, Mr. Bijo and Mrs. Chandra in ‘XYZ Ltd’ shall be as follow:

| S. No. | Shareholders | Holdings | Actual Interest in XYZ Ltd | BEN-1 |

| 1. | Mr. Arun | 50% | (25*50%) = 12.5% | Yes |

| 2. | Mr. Bijo | 30% | (25*30%) = 7.5% | No |

| 3. | Mrs Chandra | 5% | (25*5%) = 1.25% | No |

Problem: Mr. Anil is the registered owner of 5,000 shares (Constituting 25% of the share capital) of Viata Ltd whose beneficial holder is M/s XYZ & Co., a Partnership Firm. Mr. Anil transfers 500 shares to Mr. Bijo whose beneficial interest shall lie with M/s BBC & Co., a Partnership Firm in which Mr. X and Mr. Y are partners sharing profits equally.

Solution: In the instant case there is change in the beneficial interest of the shares held by Mr. Anil, therefore, declaration as prescribed u/s 89 shall be given by Mr. Bijo in MGT 4 and M/s BBC & Co., a Partnership Firm in MGT 5 and thereafter by Viata Ltd in MGT 6. Also, there is a SBO of more than 10% by the partners Mr. X and Mr. Y and hence, declaration as prescribed u/s 90 shall be given by Mr. X and Mr. Y in BEN 1 and thereafter by M/s. Viata Ltd., in BEN 2. Also, M/s. Viata Ltd shall maintain a register of interest declared by Mr. X and Mr. Y and changes therein in Form No. BEN-3.

Problem: Mr. Anil is the registered owner of 9,000 shares (Constituting 90% of the share capital) of Vista Ltd whose beneficial holder is M/s XYZ & Co., a Partnership Firm in which Mr. X and Mr. Y are partners sharing profits equally. Again Mr. Bijo is the registered owner of 1,000 shares of Vista Ltd whose beneficial holder is M/s XYZ & Co, a Partnership Firm. Now, Mr. Anil transfers 5000 shares to Mr. Bijo.

Solution: As there is no change in the beneficial ownership, no declaration is required to be given u.s 89. However, the Share Transfer deed is to be executed and thereafter form SH-4 needs to be sent to the Company which is sufficient to show the change of registered owners in the register of members. In the instance, as there is SBO, the initial disclosure as required under Sec. 90 (BEN 1 by Mr. X and Mr. Y, BEN 2 by M/s. Vista Ltd) is required.

Problem: Mr. Anil beneficially holds Rs. 55,000/- equity in Viata Ltd (Capital Structure of the Company: Equity Rs. 2,00,000/-; CCPS Rs. 3,00,000/- & CCDs Rs. 1,00,000/-). Viata Ltd holds 50% of Equity shares in Zing Ltd. Whether Mr. Anil can be regarded as SBO for Zing Ltd?

Solution: Mr. Anil’s % of share capital held in Viata Ltd will be as follows

As per Explanation II of Rule 2 (e) of SBO Rules, instruments in the form of GDRs, CCDs, CCPs shall be treated as shares. Accordingly,

= Rs. 55,000 / (Equity Rs. 2,00,000/-; CCPS Rs. 3,00,000/- & CCDs Rs. 1,00,000/-)*100

= Rs. 55,000 / 6,00,000*100

= 9.17% and therefore, Mr. Anil will not be regarded as SBO of Zing Ltd.

Conclusion

A giant step has been taken by the Ministry of Corporate Affairs (MCA) by, notifying the Companies (SBO) Rules, 2018 along with Section 90 of the Companies Act, 2013. The main objective behind this step is to eradicate money laundering and the objective of aforesaid disclosure is to identify the true individual owners of a company, in case of complex layered structure. As the implications of the amended section and newly notified rules are quite wide, the companies have to take utmost care and the compliances of the same has to be ensured in true letter and sprit.

DISCLAIMER: The information given in this document has been made on the basis of the provisions stated in the Companies (Amendment) Act, 2017 and Companies Act, 2013. It is based on the analysis and interpretation of applicable laws as on date. The information in this document is for general informational purposes only and is not a legal advice or a legal opinion. You should seek the advice of legal counsel of your choice before acting upon any of the information in this document. Under no circumstances whatsoever, we are not responsible for any loss, claim, liability, damage(s) resulting from the use, omission or inability to use the information provided in the document.

When there is change in holding and Form BEN 2 to be filed for the change, whether the company has to send Form BEN-4 or a letter is enough asking for the details. As i feel in the format of BEN 4 it is relevant to know the SBO and no point in sending again when the person is already SBO. Kindly clarify.

Facts: 1. Natural individual is beneficial owner of 99% shares of company A and is registered as owner

2. Same natural individual holds 1% shares of company A through company B.

Query 1: Is BEN-1 (and 2 and 3) required in respect of his 99% holding?

Query 2: Is BEN-1 (and 2 and 3) required in respect of his 1% holding since he is already a direct 99% holder?

Whether it is applicable in case of wholly owned foreign subsidiaries as well?