WHAT IS SOCIAL AUDIT ?

A social audit is a formal review of a company’s endeavors, procedures, and code of conduct regarding social responsibility and the company’s impact on society. A social audit is an assessment of how well the company is achieving its goals or benchmarks for social responsibility.

Social audit is a process of assessing and evaluating an organization’s social and environmental performance. It involves examining the organization’s activities, policies, and impacts on various stakeholders, including employees, customers, communities, and the environment.

The purpose of a social audit is to measure and report on an organization’s social responsibility, ethical practices, and sustainability efforts. It helps identify areas where the organization is performing well and areas that need improvement. The audit typically involves gathering data, conducting interviews, reviewing documentation, and analyzing the organization’s performance against relevant standards, guidelines, and societal expectations.

Social audits may cover a wide range of topics, including labor practices, human rights, community engagement, environmental impact, product safety, diversity and inclusion, and ethical sourcing. The results of a social audit are often presented in a report that highlights the organization’s strengths, weaknesses, and recommendations for improvement.

By conducting social audits, organizations can demonstrate their commitment to social responsibility, enhance transparency and accountability, and identify opportunities to align their business practices with sustainable development goals. It helps organizations monitor and manage their social impact, engage stakeholders, and work towards continuous improvement in their social and environmental performance.

GLOBAL HISTORY OF SOCIAL AUDIT

The concept of social audit emerged in the 1960s as a response to growing concerns about corporate social responsibility and the impact of business activities on society. It gained prominence as a tool for assessing and reporting on the social performance of organizations.

One of the early pioneers of social audit was Robert John Davis, an American sociologist who introduced the concept in his book “The Social Audit: A Management Tool for Cooperative Business” published in 1967. Davis proposed social audit as a means to evaluate the social performance of cooperatives, focusing on their adherence to cooperative principles, democratic governance, and social impact.

In the 1970s, social audit expanded beyond cooperatives and began to be applied to other types of organizations, including corporations, government agencies, and nonprofit entities. The idea gained traction as a way to hold organizations accountable for their social and environmental practices.

Over the years, various organizations, academic institutions, and social activists have contributed to the development and promotion of social audit methodologies and frameworks. These efforts aimed to provide standardized approaches and guidelines for conducting social audits.

Additionally, the rise of corporate social responsibility movements, sustainability reporting frameworks (such as the Global Reporting Initiative), and increased stakeholder expectations for transparency and accountability have further propelled the adoption of social audit practices.

Today, social audit has evolved into a recognized tool for assessing and improving an organization’s social and environmental performance. It continues to evolve with the changing landscape of corporate social responsibility, sustainability, and stakeholder engagement.

SOCIAL AUDIT IN INDIA

Social audit was introduced in India as a means to promote transparency, accountability, and citizen participation in the governance and implementation of social welfare programs. The concept gained prominence with the passage of the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) in 2005.

MGNREGA is a flagship social welfare program in India that guarantees 100 days of employment per year to rural households. As part of the Act, provisions were made for conducting social audits to ensure the effective implementation of the program and prevent corruption and mismanagement.

The introduction of social audit in India was supported by civil society organizations, grassroots movements, and activists advocating for increased transparency and accountability in public programs. These groups highlighted the importance of involving local communities and beneficiaries in monitoring and evaluating the implementation of social welfare schemes.

The government of India recognized the value of social audit and included it as an integral component of MGNREGA. The Ministry of Rural Development, along with state governments, developed guidelines and procedures for conducting social audits under the program.

In a social audit, local communities, beneficiaries, and civil society organizations participate in the process of verifying and assessing the implementation of MGNREGA works, including expenditure, quality of assets created, and adherence to prescribed guidelines. The findings of the social audit are documented and shared with relevant authorities for corrective action, if needed.

Since the introduction of social audit in MGNREGA, the concept has been extended to other social welfare programs and initiatives in India. It has become an important tool for ensuring transparency, empowering communities, and improving the delivery of social benefits. Several states in India have also implemented their own social audit frameworks to monitor the implementation of various government schemes and programs.

SOCIAL AUDIT-NEW PROFESSIONAL AVENUE

SEBI vide its notification dated 25th July, 2022 has made amendments in the SEBI (ICDR) Regulations, 2018, and SEBI (LODR) Regulations, 2015. These amendments have been made to provide Social Enterprises with additional avenues to raise funds through the Social Stock Exchange (SSE), which is a novel concept in India. It provides eligibility of organizations to raise funds through Social Stock Exchange, eligibility of entities to be classified as “Not for Profit Organization”, eligibility of entities to be classified as “For Profit” Social Enterprises, means through which Social Enterprises can raise funds, and obligations of Social Enterprises. Furthermore, to strengthen the governance framework in these entities, & provide better confidence to such investors, SEBI has introduced the concept of Annual Impact Report by a Social Auditor. The purpose of this Social Audit is to ascertain the impact made by the Social Enterprise through its activities, intervention, programs or projects implemented during the reporting period. The annual impact report shall be audited by a Social Auditor. ICMAI Social Auditors Organization (ICMAI SAO) To enrol & regulate the Social Auditors and also to prescribe the Social Audit Standards, the Institute of Cost Accountants of India, in compliance with SEBI Regulations, has incorporated a section 8 company titled ICMAI Social Auditors Organization. The ICMAI SAO will enrol eligible CMAs & others as Social Auditors and focus on their capacity building through continuous professional advancement with emphasis on adherence to the highest ethical standards and compliance with the Social Stock Exchange requirements.

Professional Opportunity

It is expected that large number of Social Enterprises, both not for profit and for profit, will take advantage of the newly created architecture for raising funds through the mechanism of Social Stock Exchange (SSE). Each such Social Enterprise would be required to submit an Annual Impact Report to the SSE duly audited by a Social Auditor. Hence, there would be huge opportunities for the CMAs to practice as Social Auditors.

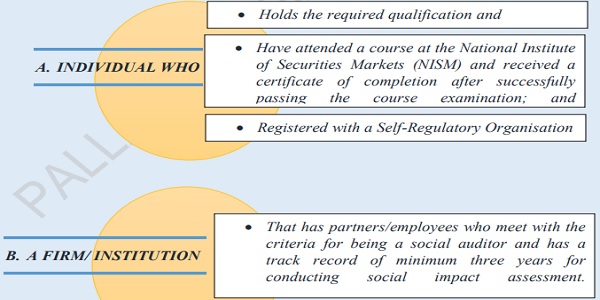

Eligibility Criteria for Social Auditor

Eligibility Qualification & Experience for Social Auditor

♦ Post-graduates from universities recognized by University Grants Commission (UGC) with a minimum of 3 years of experience in the development sector, or

♦ Graduates from universities recognized by the UGC with a minimum of 6 years of experience in the development sector, or

♦ Cost and Management Accountant, Chartered Accountant, or Company Secretary holding valid Certificate of Practice.

NISM Social Auditors Certification Examination

As mandated by SEBI, NISM Social Auditors Certification Examination aims to create a pool of social auditors who would assess the impact of social interventions of various social enterprises who raise funds through the Social Stock Exchange platform.

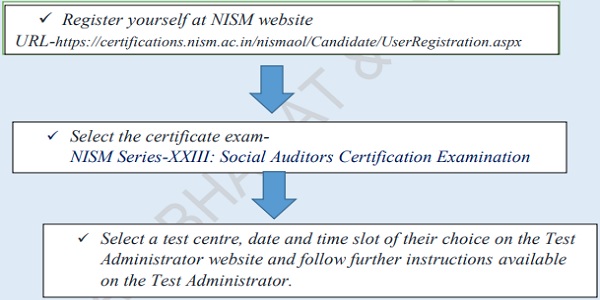

How to register for NISM-Series-XXIII: Social Auditors Certification Examination?

♦ Fee structure: The fees for “NISM-Series-VIII: Social Auditors Certification Examination” is Rupees One Thousand Five Hundred only (Rs.1500/-) plus applicable GST @ 18%

♦ Test details & Assessment structure: The examination will have 85 multiple-choice and 3 case-based questions (each case having 5 questions) totaling to 100 marks. Exam should be completed in 2 hours. There will be negative marking of 25% of the marks assigned to a question. The passing score for the examination is 60%.

♦ Study material for preparing for this examination: You will receive a soft copy of the workbook/study material after enrolment for the examination. For non-receipt of a soft copy of the workbook/study material, you may contact NISM

♦ Validity of Certificate: The Certificate is valid for 3 years which can be renewed after giving exam again

EMPANELMENT OF SOCIAL AUDITORS WITH ICSI INSTITUTE OF SOCIAL AUDITORS:

The ICSI has set up the Institute of Social Auditors (ICSI-ISA) to empanel the Social Auditors. Further, the Institute has issued the ICSI Social Audit Standards (ICSI SAS 1 – ICSI SAS 16) to provide guidance to conduct Social Audit of Social Enterprises engaged in any of the activities as enumerated under Regulation 292E(2)(a) of SEBI (ICDR) Regulations, 2018. The same can be accessed at: https://www.icsi.edu/media/webmodules/ICSI Social Audit Standards .pdf

In this regard, The ICSI has made submission to the SEBI to specify the ICSI-ISA as SRO to empanel the Social Auditors with the ICSI-ISA. Further, upon receiving the approval from SEBI for the same, ICSI-ISA would start the empanelment process. ICSI-ISA invites expression of interest for initial empanelment of Social Auditors, in prescribed format, from experienced Social Auditors for conducting Social Audit of the Social Enterprises as prescribed by SEBI. It may be noted that, regular empanelment will be as per the regulations of SEBI and the norms for the same will be notified. Interested applicants may submit the following google form for the purpose of Initial empanelment: https://forms.gle/H14URjmuBT5NJaHh7

ICSI also wants its esteemed members to encourage the Not for Profit Organizations (NPOs) within the meaning of Regulation 292A(e) of SEBI (ICDR) Regulations, 2018 to get themselves registered on the Social Stock Exchange as Social Enterprises in order to avail the benefits of raising funds and executing any of the purposes under Regulation 292E(2)(a) of SEBI (ICDR) Regulations, 2018 successfully for which they have been established.

REFERENCE-

https://www.caclubindia.com/articles/social-auditor-new-professional-avenue-49300.asp.

Author Bio

Excellent Learning👍