CA Preksha Choraria

Indian Accounting Standard (IND AS) 10 Events after The Reporting Period

Indian Accounting Standard (IND AS) 10 Events after The Reporting Period

Before going through the aforementioned Ind AS, it is very crucial to understand its nomenclature and reason for its existence.

Ideally, transactions relating to relevant Reporting Period are recorded in the relevant Financial Statements. However, there are several events which happen after Reporting date but are significant for respective Reporting Period to show true and fair view and for the purpose of stakeholder’s decision making. Thus, reporting of significant events, occurring post reporting date, are required to maintain transparency of financial statement.

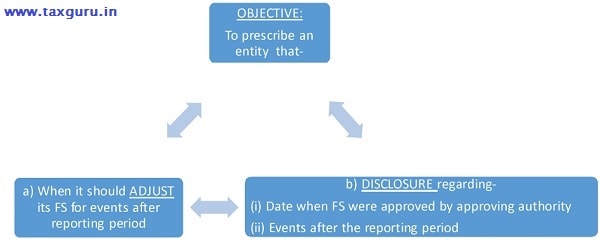

OBJECTIVE:

Additional Requirement:

An entity should not prepare its FS on GOING CONCERN assumption if the very existence of the assumption is inappropriate or non-tenable.

Eg. ALtd. was manufacturing cardboxes. It has finalised its FS for the year ended 31/03/2016. On 05/04/2016 a massive fire broke out in its factory leading to destruction of all machinery and raw-material. Thus no more production could be undertaken in the factory. This event has significantly endangered the Going Concern assumption of the entity. Now the company is required to re-instate its FS without assuming the Going Concern assumption.

Opinion: The Company may record all assets at their Realisable value.

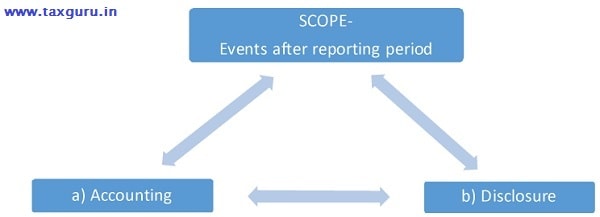

SCOPE:

DEFINITIONS:

Exception to above definition:-

Where there is a material breach of terms & conditions in a long term loan arrangement making the loan repayable on demand and any subsequent agreement with the lender after reporting date to not demand loan as a consequence of breach of terms & conditions will result in an Adjusting Event.

Examples-

| Adjusting events- | Non-Adjusting events- |

| 1. A law suit regarding insolvency was pending on reporting date against a significant customer and after reporting date he is declared insolvent by court. Thus, relevant changes in Customers balance should be made in his account on reporting date. | 1. Announcement to discontinue an operation of the entity or announcement regarding merger/acquisition of an entity. i.e. Maruti motors announces, after reporting date, to take over Japan based company Suzuki to form Maruti Suzuki |

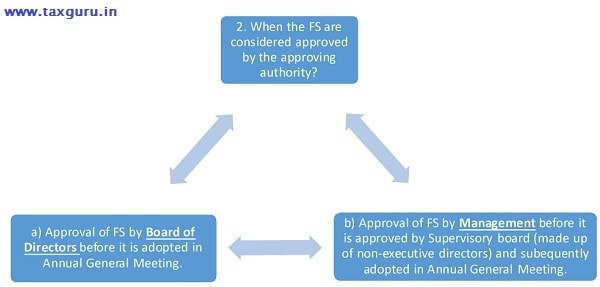

Summary Note: – Events after reporting period are business activities that happen after balance sheet date but before approval of FS by approving authority which may affect the FS favourably or unfavourably.

RECOGNITION & MEASUREMENT:

DIVIDENDS:

Normally, Dividends are PROPOSED by Board of Directors and it is subsequently APPROVED by shareholders in Annual General Meeting. The following entry was passed earlier for recognising proposed dividend-

Profit & Loss A/c Dr.

To Proposed Dividend

Now, as per this IND AS NO PROVISION FOR PROPOSED DIVIDEND is to be recognised in FS. The logic behind such change is-

No liability exists on Reporting Date and liability occurs only when shareholders approve the proposal of dividend of board. Thus, the liability comes into existence after AGM is conducted.

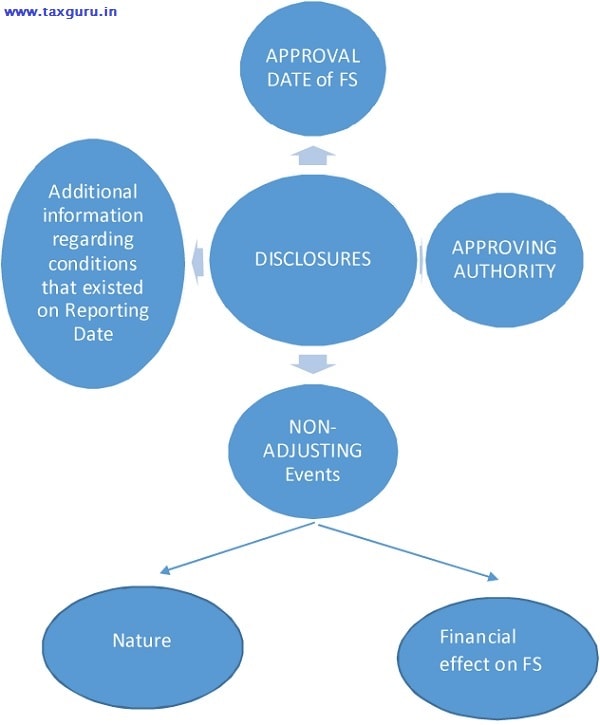

DISCLOSURE:

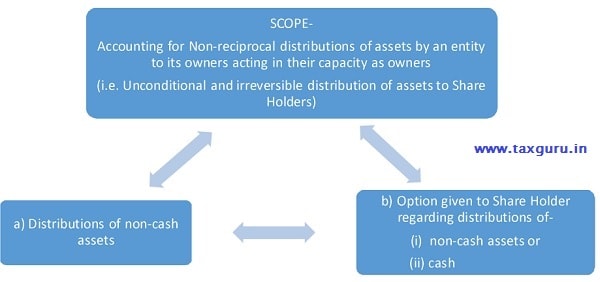

APPENDIX A: DISTRIBUTION OF NON-CASH ASSETS TO OWNERS

(This Appendix is an integral part of Ind AS 10.)

This appendix deals with when to realise dividend payable, in cash or by way distribution of non-cash asset, to Share Holder.

SCOPE:

1. Appendix applies only to distributions in which all owners of the same class of equity instruments are treated equally g. A Ltd. is controlled by public at large. No single individual has power to control the entity or no group of shareholders is bound by a contractual agreement to act together to control the entity. If A Ltd. distributes its Fixed Assets or any other asset among Share Holders on proportionate (pro-rata) basis then this appendix is applicable.

2. Appendix does not apply when the non-cash asset is ultimately controlled (as defined in Ind AS 103 Business Combinations) by the same parties both before and after the distribution.

3. This Appendix does not apply when an entity distributes some of its ownership interests in a subsidiary (non-cash asset) but retains control of the subsidiary.

When to recognise a dividend payable?

As discussed earlier, dividend payable will be recognised when it is approved and authorised to be paid unconditionally.

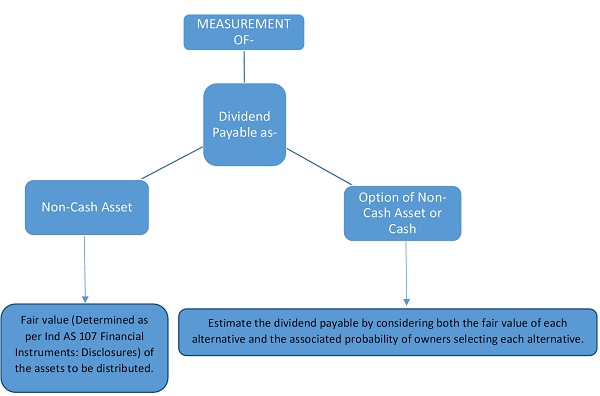

Measurement of a dividend payable

- When an entity settles the dividend payable, it shall recognise the difference, if any, between the carrying amounts of the assets distributed and the carrying amount of the dividend payable in profit or loss.

PRESENTATION & DISCLOSURES:

Opinion- The applicability of above Appendix-A is questionable as Section 123(5) of Companies Act, 2013 prohibits payment of dividend in any manner other than cash. Thus, distribution of Non-cash asset to owners as dividend is prohibited.

Note: The views expressed in the Article may not match with the views of others. Before accepting & applying, take the expert opinion.