> Earlier, there were many IAS and guidance notes (IFRIC) dealing with revenue recognition but this IFRS brought all IAS & guidance notes at one place to deal with revenue recognition including customer loyalty point which was earlier dealt by IFRIC.

| Before new IFRS – 15 | After IFRS -15 | |

| IAS 18 | Revenue from Sale of goods and services | Only IFRS -15 |

| IAS 11 | Revenue from Sale of goods and services | |

| IFRIC 13 | Construction contract | |

| IFRIC 12 | Customer Loyality programmes | |

| IFRIC 15 | Agreements for the construction of Real Estate | |

| IFRIC 18 | Transfer of assets from customers |

> Non Applicability of this IFRS –

- Leases – IFRS-16

- Financial Instruments – IFRS-9, IFRS-10, IFRS-11, IAS-27 & IAS-28

- Insurance contracts – IFRS-4

- Non- monetary exchanges between entities within the same business to facilitate sales. For Example – A contract between two oil companies that agree to an exchange of oil to fulfill demand from their customers in different specified locations on a timely basis. (Because this transaction lacks the commercial substance. Hence, excluded)

> Who is customer?

- If you have a contract with the party other than a customer, then IFRS -15 does not

A customer is a party that has contracted with an entity to obtain goods or services that are an output of the entity’s ordinary activities in exchange for consideration. [But not IFRS -11/IAS 28 (Joint Arrangements)]

> Core Principles of IFRS -15

IFRS – 15 is based on a core principle that requires an entity to recognize revenue –

- In a manner that depicts the transfer of goods and services to

- At an amount that reflects the consideration the entity expects to be entitled to exchange for those goods or services.

⇓

To achieve the core principle, an entity should apply the following five step model –

- Identify contract with the customer

- Identify performance obligation in the contract

- Determine the Transaction Price

- Allocate Transfer Price to the Performance Obligation

- Recognize Revenue when (or as) an entity satisfies a Performance Obligation

Identify contract with the customer

> What is Contract?

Agreement between two or more parties that creates enforceable rights and obligation,

> A contract comes under the purview of IFRS 15 only when it meets all the given criteria.

> Following criteria required to be fulfilled to be categorized as contract –

- Both the parties should have approved the

- Terms and conditions of Contract should be clearly identified regarding –

Pricing

Obligation

Delivery

Credit terms

Statement of work

- Each Party’s right can be

- Contract has a commercial

- It is probable that the entity will collect substantially all the consideration to which it will be entitled.(Ex -1)

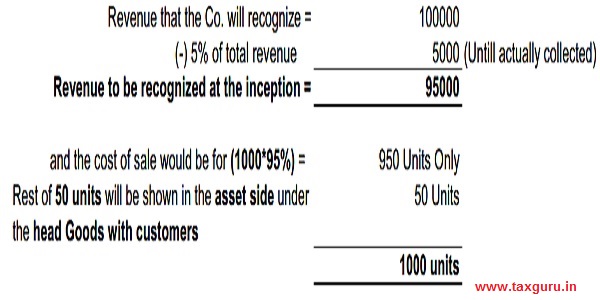

Example-1:

Suppose Company is selling 1000 units to customers @ 100/unit and it is probable that the company will not receive 5% of revenue.

– In that case Co will recognize only 95% of revenue at the inception and rest 5% at the time of actual receipt of the amount.

– Suppose we have recognized revenue but at the yearend customer is in bad condition or has been declared bankrupt. This will lead to the doubtful debt which is dealt by Financial Instrument that is Expected Credit

> Identify combined contracts i.e whether they are single contract or separate with each other

> How to deal with contract modification (i.e. accounting for contract modification)

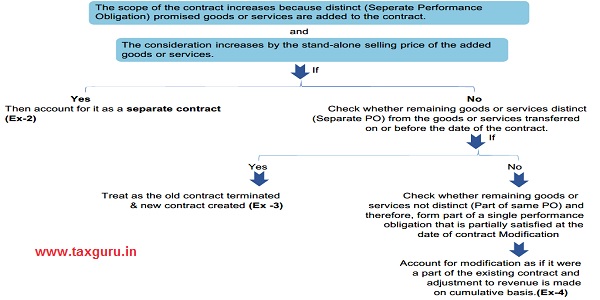

- Contract modification means change in the contract, it can either be price change, scope change or

- First we need to check whether both the following conditions are satisfied –

Example -2:

Suppose we contracted to sell 100 TVs @ 15000 and will supply 20 units per month over a 5 month period (control over each unit passes to the customer on delivery). After delivery of 80 units, the contract is modified to require the delivery of an additional 40 units (i.e 140 units total). At the modification date, the stand-alone selling price of one unit of the product has increased to Rs. 20000 and the price charged for additional 40 TVs is Rs.20000 i.e market value.

Solution –

In this case, contract for additional TV is separate PO and price charged is stand alone price i.e Market Value of TV at the time of purchase of additional units. Hence account for it as a separate contract.

| Particulars | Original | Additional |

| 80 Units @ 15000 | 1200000 | – |

| 20 Units @ 15000 | 300000 | – |

| 40 Units @ 20000 | – | 800000 |

Time of Revenue Recognition –

For Original Contract – When original goods are delivered

For Additional Contract – When additional goods are delivered

Example-3:

Suppose in the above example, price of the additional TV is influenced by the original contract i.e the price is not stand alone selling price. Price charged for additional units is Rs. 12000/TV.

Solution –

In this case, price of the additional TV is influenced by the original contract as the price for the additional unit is not stand alone selling price of the TV at the time of purchase of that units. Hence, account for it as old contract terminated and new contract created.

| Particulars | Original | Additional |

| Revenue to be recognized before the change in | ||

| the contract – | ||

| 80 Units @ 15000 | 1200000 | – |

| Revenue to be recognized after the change in | ||

| the contract – | ||

| 60 Units @ 13000 (W. Note -1) | – | 780000 |

Working Note -1

Use a weighted average to calculate the amount of revenue to be recognized for each of the units delivered after the contract change.

Calculation –

– Amount of revenue ⇒ 780000 (20*15000)+(40*12000)

– Per unit revenue to be recognized on each deliveries ⇒ 13000 (780000/60)

Journal Entries –

For first 80 Units –

Example -4:

We have given a contract to construct the house. Price charged by contractor is Rs. 1000000 and the cost of material is Rs.800000. After 1 year 50% of the work has been completed but due to sudden change in the market, material cost has come down significantly, so I asked my contractor to reduce the price. How would contractor account for this modification?

Solution –

In this case, services are not distinct i.e there is no separate performance obligation and therefore, form part of a single performance obligation that is partially satisfied at the date of contract modification. So, we will account for this modification as if it were a part of the existing contract and adjustment to revenue will be made on cumulative basis.

| Total Revenue | 1000000 |

| Cost of the material | 800000 |

| Profit | 200000 |

1st Year Half work is done, So – Revenue to be recognized 500000 (1000000*50%)

- After 1 year cost of material come down to 700000

- New Revenue is 900000

2nd year – 70% work completed

Revenue to be recognized in 2nd year –

| Particulars | Cumulative Revenue | Revenue already recognized | Revenue to be recognized in 2nd year |

| Revenue | 630000 | 500000 | 130000 |

| Cost | 490000 | 400000 | 90000 |

| Profit | 140000 | 100000 | 40000 |

> Identify Separate Performance Obligation(PO)

- What is Performance Obligation?

– Promise to provide goods and services to a customer are called a Performance Obligation.

– A company would account for a PO separately only if the promised goods or service is distinct. Goods or services are distinct if it is sold separately because it has distinct function and a distinct profit

– Promise in a contract can be explicit or

- A good or service that is promised to a customer is distinct if both of the following conditions are satisfied-

– Customer can benefit from the good or service either on its own or together with other resources that are readily available to

and

– Separately identifiable from other promises in the

- What do you mean by readily available resources?

– That can be sold separately or customer has already obtained

> Determination the Transaction Price

Transaction Price is the consideration that an entity expects to receive from the customer in respect of their deliverables (supplies). It is expected price not agreed price i.e. not always the price set in the contract. But this excludes any amount collected on behalf of third party like – GST because they do not represent an economic benefit flowing to the entity.

Objective

⇓

To predict the total amount of consideration to which the entity will be entitled from the contract.

⇓

For this we need to estimate the Transaction Price.

So, What could be the Transaction Price?

Sales Value, but this value needs to be adjusted after taking into following considerations-

- Variable Consideration including Constraining estimates in Variable Consideration

- Significant Financing Component

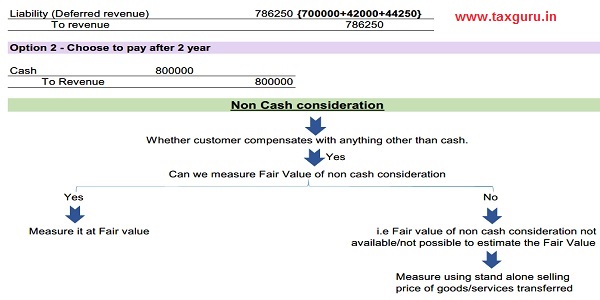

- Non Cash consideration

- Consideration payable to the customer

Variable Consideration

Amount of consideration may vary because of –

- Bonuses

- Fine

- Discounts (Bulk Discount, Cash Discount, Quantity Discount)

- Rebates

- and similar items

IFRS -15’s guidance on variable consideration also applies if –

– The amount of promised consideration under a contract is contingent on the occurrence or non-occurrence of a future event.

– The facts and circumstances at contract inception indicate that the entity intends to offer a price

In case, Transaction price includes Variable consideration then entity determines it either on two basis which better predict the amount of consideration to which it will be entitled –

1) Expected Value – The expected value is the sum of probability-weighted amounts in the range of possible consideration amounts.

This method would be appropriate in case a entity has a large number of contracts with similar characteristics.

2) The most likely amount – It is the single most likely amount of consideration in the range of possible consideration amounts.

This method would be appropriate if the contract has only two possible outcomes i.e. an entity either achieves a performance bonus or does not.

⇓

Apply constraining estimates in variable consideration

⇓

Means while estimating variable consideration i.e “Expected Value” or “Most Likely amount” & including it in Transaction Price we need to consider constraint i.e we should include variable consideration only when it is highly probable that a significant reversal in the amount of cumulative revenue recognized will not occur.

> The entity should consistently apply one method throughout the life of the contract.

> An entity that expects to refund a portion of the consideration to the customer would recognize a liability for the amount of consideration it reasonably expects to refund. The entity would reconsider the refund liability and circumstances each reporting period based on current situation.

Quantity Discount

Example –

> Supplier allows Price discount based on quantity purchased as follows:-

| If quantity purchased ( In a year | Price |

| 15000 | Rs 10 |

| More than 15000 < 60000 | Rs 9 |

| More than 60000 | Rs 8 |

- Case -1 -Till June customer purchased 2000 units only.

- Case -2 -Till June customer purchased 10000

Solution –

Case -1

- Entity will recognize revenue @10 for the qtr ended June as the customer’s purchasing pattern is such, that that it is highly probable that a significant reversal in the cumulative amount of revenue recognized would not occur conclude when the certainty resolves.

Hence, Revenue to be recognized till the qtr ended June 20000 [2000*10]

Case -2

- Entity will recognize revenue @9 for the qtr ended June as the customer’s purchasing pattern is such that conclude that it is highly probable that a significant reversal in the cumulative amount of revenue recognized would occur when the certainty

Hence, Revenue to be recognized till the qtr ended June 90000 [10000*9]

Sale with a Right of return

– When we are selling goods with a right of return, in that case this is not a performance obligation and we will recognize revenue for the transferred products at a consideration which an entity expects to

– We will create a refund liability for estimated return & will update refund liability measurement at end of each

– An asset (and corresponding adjustment to cost of sales) will be created for its right to recover products from customers on settling the refund

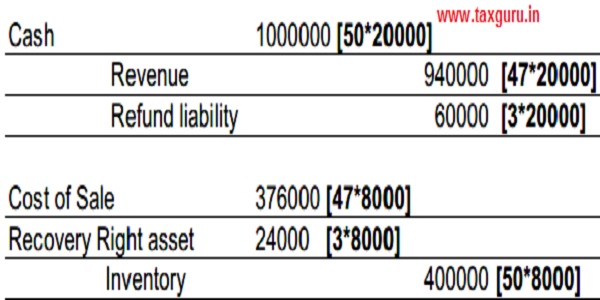

Example –

Suppose entity sells mobile phones on 30 days return policy if returned unused within 30 days . Entity sold 50 cell phones at a price of Rs. 20000 and the cost of each unit is Rs. 8000. Entity estimates return rate to be 3 out of 50 cell phones. How Entity will account for this transaction?

Solution –

We will recognize the revenue for estimated returnable cell phones either at the time when customer accepts the goods or right to return the product lapses.

Entry – If product is actually returned

Significant Financing Component

- We should recognize the revenue at the price that reflects the cash selling price of goods or services transferred. For this we need to adjust the promised consideration for the Time value of money if there is significant financing component.

- We consider it significant if timing difference between performance obligation & payment (Either advance or after delivery) is of more than 12 months

- It is not required that the financing terms should be explicitly mentioned in the

- Even if it is mentioned that interest rate is 0%, we need to consider incremental borrowing rate of company to calculate present

Example –

Suppose a company provides product on 0% interest rate EMI. You purchased washing machine today & required to make payment after 2 years.

| Washing Machine cash price – | 50000 |

| Interest Rate – | 0% |

| Incremental borrowing rate of company – What would be the revenue? | 10% |

Solution-

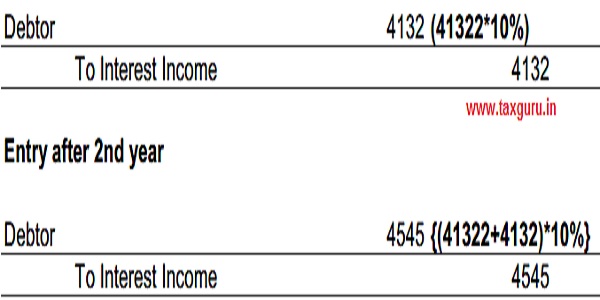

We will recognize revenue at Present Value discounted at the borrowing rate of the company even when the company is providing it at 0% discount.

So, will recognize revenue at → 41322 {50000/(1.1)^2}

Journal Entry –

Entry after 1 year

In Case we have received cash in advance then what will happen?

Example –

Suppose customer has contracted to purchase a machine at the end of 2 year. The contract includes two alternative options i.e either to pay Rs. 700000 now or pay Rs. 800000 after 2 year when the control is transferred. Customer Chooses to pay at the time of contract inception i.e. now. Entity’s incremental borrowing rate is 6%.

Solution –

Option 1 – Choose to pay now (i.e in advance)

We will first create a liability for the amount received

After 2 years when control gets transfer –

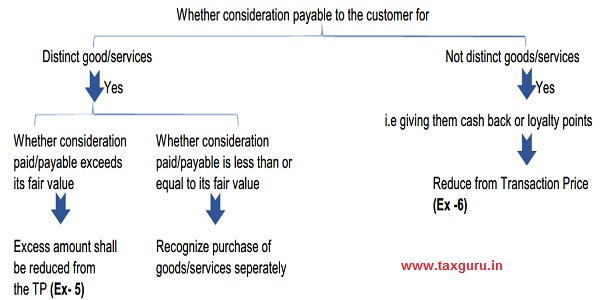

Consideration payable to the customer

- Generally customer pays to seller but in some cases seller pays or expects to pay to customer cash including credits, coupons and rebates

For example – Many online sites nowadays are giving cash back to their customers & some retail stores are giving loyalty points. Like- Pantaloons, Big Bazar, V-Mart etc.

Suppose X Ltd sells goods to Y Ltd for amounting Rs. 100000 and Y Ltd provides X Ltd manpower services, the stand alone selling price of manpower service is Rs. 120000 but X ltd pays him Rs. 130000 for this service.

How X Ltd will account for it?

Solution –

In the given case,

Stand Alone Selling Price (Fair Value) i.e 120000 < Consideration i.e 130000

Hence, we will adjust the revenue of Rs. 100000 from sale of goods for the diff of Rs. 10000 (i.e 130000-120000)

Example -6

Suppose amazon has a policy to give cash back of Rs.1000 on purchase worth Rs.10000. How Amazon will account for it?

Solution –

In this case there is no distinct service. Hence, while recognizing the revenue of Rs. 10000 amazon will adjust the cash back of Rs.1000 and will record the revenue at Rs. 9000 only.

> Allocation of Transaction Price to performance obligation

After determination of Transaction price & Performance obligation, we need to split the TP and allocate it to the individual performance obligation

⇓

We split the TP to PO on the basis of relative Stand alone price.

⇓

If there is discount between bundle price of goods/services and total of standalone price of each goods/services in that bundle, then allocate the discount proportionately to all individual goods/services based on their relative stand alone price.

⇓

If situation arises where discount is related to only particular goods/services in a bundle then allocate discount to only that particular goods/services

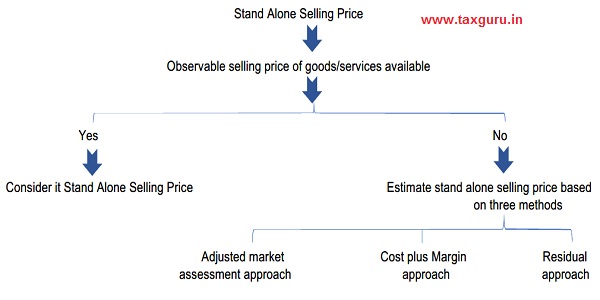

Determination of Stand alone price –

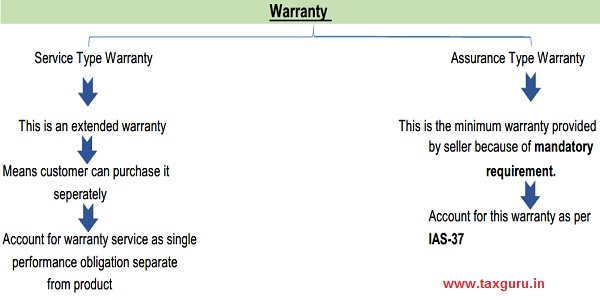

- Determine stand alone price at the inception of the

Example

Suppose entity sell a watch with extended warranty for Rs.10000. Stand alone selling price of watch is Rs.10000 and extended warranty is Rs. 1000 respectively.

What should be the revenue?

Solution –

| Particulars | Stand alone Price | Revenue |

| Car | 10000 | 9091 |

| Extended Warranty | 1000 | 909 |

| 11000 | 10000 |

{10000*10000/11000}

1000 909 {10000*1000/11000}

Example

Suppose a car company sells 20 Cars @500000/car and expects 1 defective piece per 20 car, the cost of which will be 20000/defective car. Cost of production per car is Rs. 300000.

Accounting if seller provides only assurance warranty service of one year –

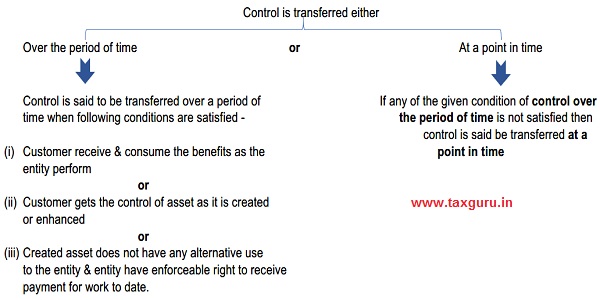

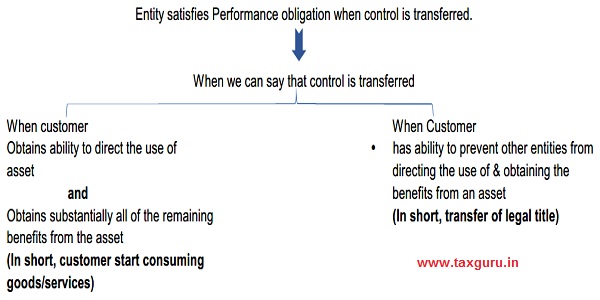

> Recognize Revenue when(or as) an entity satisfies a Performance Obligation

How to determine a time of control transfer?