Few General considerations that we should know before we start with the topic Identification of contracts (First of the five steps for revenue recognition)

Important Definition:

- Customer: A customer is a party that has contracted with an entity to obtain goods or services that are an output of the entity’s ordinary activities in exchange for consideration. A counter party to the contract would not be a customer if, for example, the counter party has contracted with the entity to participate in an activity or process in which the parties to the contract share in the risks and benefits that result from the activity or process (such as developing an asset in a collaboration arrangement) rather than to obtain the output of the entity’s ordinary activities.

a) Example: ‘A’ ltd is a software development company where it sells various software and collaborates with ‘b’ Ltd to provide the cloud services and they will share the profit earned by selling software, as software could not be sold without the cloud. Here “A” Ltd is not the customer of “B” Ltd as they both agree to share the Risk and benefits.

b) Example: ‘A’ LTD sells the software to the customer and receives the hosting services from B LTD and pays hosting cost to “B” LTD for receiving the services. Here ‘A’LTD is a customer and “B” LTD will recognize the revenue as risk and benefits are not shared and ‘A’ is receiving service from ‘B’ LTD which is its output.

Identification of contracts with customers

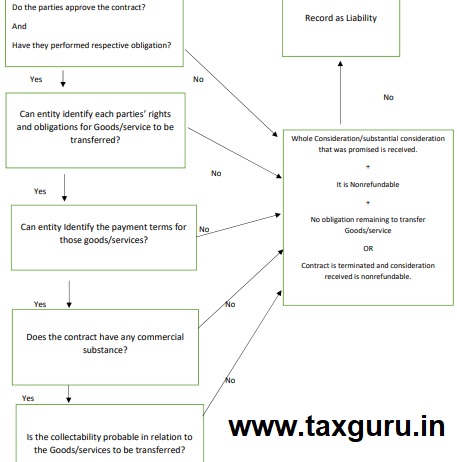

Before we have detailed knowledge with examples about the different issues related to each point lets see the following modal as to how we can Identify if the contract exists and if not how should consideration be treated.

1. The parties to the contract have approved the contract (in writing, orally or in accordance with other customary business practices) and are committed to perform their respective obligations

The first clause basically contains two parts

- Contract must be approved

Let’s take examples for this.

Example 1a: A ltd is software company where it provides software with certain trail period. A Ltd offers 30 days trial period to the customer and if the customer excepts the service before lapse of trial period then it will Invoice for 12 months but in case if the customer does not excepts the services then it cannot be said that customer has approved the contract..

Example 1b: A Ltd provides a 30 days trial and then invoice for the further 11 months for Rs.1200 annually, but in this case, they have the term in the contract that says that if any party terminates the contract then it will have to pay penalty. In this case it can be said that the contract has been approved the contract and A Ltd can recognize revenue even in trial period (provided all the 4 other steps of revenue recognition are followed) that is A Ltd can recognize revenue for an amount of Rs 100 (1200/12) for 30 days trial also throughout the year.

- Committed to perform respective obligations

This part of the Ind AS talks about the respective obligations and not all obligations of the contract.

Let’s take an example for this,

Example 1c: If the company has the term in the contract that a minimum number of users should be there while delivering the software service to the customer, but customer is not able to fulfill the criteria then it can be said that party has not performed the respective obligation, but if in the history also the company is unable to enforce such term then it can be said that contracts still exist as far as customer is substantially committed to perform the other obligations of the contract.

2. The entity can identify each party’s rights regarding the goods or services to be transferred.

These criteria would basically include terms in the contract from which it is evident that the entity is able to identify its rights and obligations and rights and obligation of the other party.

Let’s take an example for this,

Example 2a: There is MSA (master service agreement) which clearly states that entity would provide service to minimum 12000 users annually and in the past the entity is able to enforce such term then alone MSA can be said to establish rights and obligations. But if in the past entity waves of such term then alone MSA would not be enough but it would also need PO or Order form etc. which then in combination would be said to state rights and obligations.

Example 2b: There is MSA which states general terms and conditions but does not specify the quantity that would be delivered, here rights and obligations would be said to be identified when it is accompanied be the PO or order form specifying the quantities.

3. The entity can identify the payment terms for the goods or services to be Transferred

This clause is important not only to determine transaction price but also helps in identifying the collect ability of the customers. A contract must contain the payment terms (fixed/variable) from which entity is able to build an expectation as to what amount they are going to receive.

4. The contract has commercial substance (i.e. the risk, timing or amount of the entity’s future cash flows are expected to change as a result of the contract)

Contract is said to have commercial substance if the future risk or cash flow are expected to change.

Let’s take an example for this,

Example 4a: A Ltd delivers software for free of charge to B Ltd and later on takes back for free. Here, if this clause would not have been into force then entities would have enhanced the revenue as “A ltd” would have recorded the revenue when software delivered to B Ltd and B Ltd would have recorded revenue when delivered back to A ltd, this would have led to enhanced revenue recognition with too and fro movement of the goods. To avoid this situation this clause was included. In short there must be economic consequence from the contract.

5. It is probable that the entity will collect the consideration to which it will be entitled in exchange for the goods or services that will be transferred to the customer.

Determining collect ability is a major task as in evaluating whether collect ability of an amount of consideration is probable, an entity shall consider only the customer’s ability and intention to pay that amount of consideration when it is due. The amount of consideration to which the entity will be entitled may be less than the price stated in the contract if the consideration is variable because the entity may offer the customer a price concession. (Per Ind AS language).

We can take a simple example to understand this,

Example 5a: A Ltd a software vendor enters into an agreement to sell the software and provide post contract customer service for 3 years for 1000 annually that is 3000 is the contract value. But per the history of the arrangement customer is given a bit of concession. For this contract also entity expects that customer would pay Rs. 2500. Then while assessing the collect ability entity must consider 2500 instead of 3000.

Example 5b: Continuing the above example if the customer starts receiving the service and entity determines that it is not probable to collect 2500 and at the end of the first year entity was able to collect only Rs 200, then entity would not recognize revenue of Rs 200, rather it should record it as deposit from customer.

Example 5c: Continuing the above example if entity terminates the contract and stop providing the PCS then entity can record it as a revenue for an amount of Rs 200.

Note :In analyzing the collect ability, if there is a time gap between the performance obligation and payment of the consideration, then entity must identify if there is any financing component because if that is the case then we need to treat it separately, but this would depend upon case to case. Financing component can be said to exist if the promised price and the cash selling price differ. But it would not exist, if the extended payment terms are just done to ensure that the vendor performs as specified under the arrangement rather than to provide financing to the customer even if there is a difference between cash selling price and promised price.

All the above criteria if met in the inception of the contract, then the above conditions need not be reassessed until there are significant changes in the circumstances.

If any of the above criteria is not met, then two scenarios could incur

- Entity should continuously assess the contract (preferably at the end of the reporting period) and till the time all the criteria are not met entity must record the consideration received as liability (as stated in above example 5)

- If any of the above condition is not satisfied and company has received any part of the consideration which is nonrefundable, and entity has terminated the contract then it can record it as revenue. Another case when entity can record revenue even if the above criteria is not met is when the entity has received substantial part of the consideration which is nonrefundable, and it has no liability to provide service or deliver goods in the future for particular transaction.

Combining Contracts

(Per Ind AS 115, para 17 )An entity shall combine two or more contracts entered into at or near the same time with the same customer (or related parties of the customer) and account for the contracts as a single contract if one or more of the following criteria are met:

(a) the contracts are negotiated as a package with a single commercial objective;

(b) the amount of consideration to be paid in one contract depends on the price or performance of the other contract; or

(c) the goods or services promised in the contracts (or some goods or services promised in each of the contracts) are a single performance obligation in accordance with paragraphs.

Let’s take an example to understand the above,

Example 6a: A Ltd enters into a contract with the customer to sell a Customized software for Rs 1000. Total cost to develop that software is Rs 600. Few days later A Ltd entered into the contract with the same customer to customize the software sold earlier for Rs 200. Cost incurred to customize software for the entity comes to be Rs 250. Here, Company A would have incurred a loss of Rs.50 on the second contract, if it was not combined with the first contract. Considering that the contracts were entered into at about the same time, it seems that two contracts are negotiated as a package with a single commercial objective, i.e. the customization is not done at a loss instead the consideration of Rs 1,000 stated for the software includes customization as well. Therefore, Company A should combine the two contracts for revenue recognition.

In the given case, criterion (a) of paragraph 17 for combining contracts is met because the two contracts are negotiated as a bundle with one business objective. The relationship between the consideration in the contracts (i.e., the price interdependence) is such that if those contracts were not combined, the amount of consideration allocated to the performance obligations in each contract might not faithfully depict the value of the goods or services transferred to the customer.

In short, multiple contracts need to be combined and accounted for as a single arrangement when the economics of the individual contracts cannot be understood without reference to the arrangement.

Contract Modification

To understand if the contract modification will lead to separate contract or not let’s take an example,

Example 7a (source of the example – ICAI FAQ): A software vendor enters into a four-year service contract with a customer CD Ltd. for Rs.4,50,000 (Rs.1,50,000 per year). The standalone selling price for one year of service at inception of the contract is Rs.1,50,000 per year. At the beginning of the third year, the parties agree to modify the contract as follows:

(i) the fee for the third year is reduced to Rs.1,20,000; and

(ii) CD Ltd. agrees to extend the contract for another three years for Rs.3,00,000 (Rs.1,00,000 per year).

The standalone selling price for one year of service at the time of modification is Rs.1,20,000. How should a software vendor account for the modification?

In accordance with the above, it may be noted that a contract modification should be accounted for prospectively if the additional promised goods or services are distinct and the pricing for those goods or services reflects their stand-alone selling price. In the given case, even though the remaining services to be provided are distinct, the modification should not be accounted for as a separate contract because the price of the contract did not increase by an amount of consideration that reflects the standalone selling price of the additional services. The modification would be accounted for, from the date of the modification, as if the existing arrangement was terminated and a new contract created (i.e. on a prospective basis) because the remaining services to be provided are distinct. AB Ltd. should reallocate the remaining consideration to all the remaining services to be provided (i.e. the obligations remaining from the original contract and the new obligations). Software vendor will recognize a total of Rs.4,20,000 (Rs.1,20,000 + Rs.3,00,000) over the remaining four-year service period (one year remaining under the original contract plus three additional years) or Rs.1,05,000 per year.