DIGITAL ACCOUNTING AND ASSURANCE BOARD

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

Digital Accounting and Assurance Board

The Institute of Chartered Accountants of India

www.icai.org

INTRODUCTION

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

The Institute of Chartered Accountants of India (ICAI) is a statutory body established by an Act of Parliament, viz., The Chartered Accountants Act, 1949 (Act No. XXXVIII of 1949) for regulating the profession of Chartered Accountancy in the country. ICAI is the one among st accountancy bodies in the world, with a strong tradition of service to the Indian economy in public interest.

Over a period of time, ICAI has achieved recognition as a premier accounting body not only in the country but also globally, for maintaining highest standards in technical, ethical areas and for sustaining stringent examination and education standards. Since 1949, the Chartered Accountancy profession in India has grown leaps and bounds in terms of

- Members and student base.

- Regulate the profession of Accountancy

- Education and Examination of Chartered Accountancy Course

- Continuing Professional Education of Members

- Conducting Post Qualification Courses

- Formulation of Accounting Standards

- Prescription of Standard Auditing Procedures

- Laying down of Ethical Standards

- Monitoring Quality through Peer Review

- Ensuring Standards of performance of Members

- Exercise Disciplinary Jurisdiction

- Financial Reporting Review

- Input on Policy matters to Government

DIGITAL ACCOUNTING AND ASSURANCE BOARD OF ICAI

ICAI has recently constituted “Digital Accounting and Assurance Board” (DAAB) for fostering a cohesive global strategy on aspects related to digital accounting and assurance, through sharing of knowledge and practices among st the members. DAAB is endeavouring to identify, deliberate and highlight on issues in accounting (including valuation) and assurance (including internal audit) issues in the digital world.

The DAAB is focusing on issues in accounting and assurance arising from the high pace of digitisation, including use of artificial intelligence in audit, big data analytics in audit, relevance of sampling, valuation of data as an asset, impairment testing of digital assets, insurance of data – valuation and premium fixation, etc. The Board is taking up initiatives to develop knowledge base through position papers and articles on issues relating to impact of technology on accounting and assurance.

FOREWORD

DIGITAL ERA AND THE CHARTERED ACCOUNTANCY

PROFESSION –SURVEY REPORT 2017

TECHNOLOGY has been a disruptive force in recent times; albeit the world disruption has positive connotation in regard to the disruptions driven by technology. Such disruptions have resulted in the professionals and users of technology realigning and re calibrating for future. This is applicable not only to the newer dimensions of doing business but also to support services providers to the businesses. Equally crucial has been the reflections of technology on the working of the accountancy firms as Enterprise Resource Planning, Big data, Cloud computing, Artificial intelligence, Internet of Things, Drones, Robots and the emerging interface in the workings of a typical chartered accountancy firm which are equitably perceptible.

Firms and professionals who embrace to newer technological challenges and the newer dynamics fast will have a head start in this evolving era. Initial reaction may reflect complexities and resultant impact arising out of such technical innovations. However, such innovations bring with them a new twilight zone of opportunities which are waiting to be explored.

The Institute of Chartered Accountants of India has been endeavoring to equip its members and firms to such emerging dynamics through organizing Pan India programs and realizing the potential ramification of technology to professional working of a typical chartered accountant; the ICAI had put in place the Digital Accounting and Assurance Board as a non standing Committee for identifying, deliberating and putting forth such accounting (including valuation) and assurance (including internal audit) in the digital world related issues for further deliberations within the Standard setting boards within ICAI for taking up such matters at global forums. “Digital Era and the Chartered Accountancy Profession –Survey Report 2017” is a crucial step to take the pulse of the challenges profession faces in digital era, and making the profession digital ready.

CA. Nilesh S. Vikamsey

President, ICAI

CA. Naveen N. D. Gupta

Vice President, ICAI

December, 2017

PURPOSE OF THE SURVEY

THE WORK PROGRAMME of the ICAI revolves and includes equipping its members periodically on all new developments concerning the profession. With regard to developments in area of digitisation, it was considered important to engage with the members and draw their insights from their real life work experience. Digital Accounting and Assurance Board had initiated a Survey in November, 2017 and the instant work captures the responses of nearly 920 respondents sharing their views on the emerging profile of Chartered Accountant professionals in a digitally driven era and the impact on Accounting and Assurance.

The outcome of any survey is based on the quality of response more than the number of members participating. To adduce upfront co-relational analysis, the Board used the purposive sampling as the mode of Survey analysis. The Survey involved inviting the Chartered Accountant firms and their partners to self-assess themselves on their digital competencies. While the questions were by and large structured with majority of questions providing for four options and the firm/ partner were invited to commit to desired responses, some of the questions also provided for open-ended responses to have their statements to assess their capabilities on the digital front.

The objective of this survey was to stimulate discussion about a broad range of emerging and

converging technologies and their potential impact on accounting and assurance. Survey questionnaire comprised ten questions covering in total 45 issues. Through this survey, an attempt had been made to understand our member’s views on technology, the potential it has to improve the services provided by the chartered accountants. This would enable the Board to develop an appropriate strategy on both competency development of members and also to engage in appropriate research as well as publishing position papers on emerging technologies and their impact on accounting and audit. The survey was conceptualized by the Members and Staff of Digital Accounting and Assurance Board. We are thankful to CA. Subh Ghosh, New Delhi and his team member Shri Rishabh Jain for extending support in analysis of the responses.

The Board is ever thankful to the President, Vice President and Council Colleagues for their thought leadership and continued support. The Board thanks the members for their time and sharing their experience by participating in the survey.

CA. M.P. Vijay Kumar

Chairman, DAAB

CA. Sanjay Vasudeva

Vice Chairman, DAAB

December, 2017

KEY FINDINGS OF THE SURVEY

DAAB Survey results indicate our members have a clear positive outlook for the digital future and that technology plays an increasingly important role in their professional work.

- Chartered accountants understand that the digital future is coming fast and the profession needs to get digital ready.

- Majority of the respondents have responded that artificial intelligence, big data, digital service delivery, cloud, internet of things will impact significantly the accountancy profession in the next few years.

- Innovation through artificial intelligence in accounting and assurance will be gradually witnessed.

- Almost half of the respondents have agreed that Internet of Things (IOT) will impact audit evidence.

- Majority of respondents agreed to importance of incorporation of data analytics into audit process. More than 60% of the respondents agreed to connecting data analytics to the existing suite of auditing standards, and also recognised use of data analytics for improving audit sampling.

- Majority of the respondents concurred that increase in volume of data and use of technologies will impact-

√ Nature and Extent of Audit Procedures

√ Nature and Sufficiency of Audit Evidence

√ Risk Assessment

√ Internal Control Over Financial Reporting

√ Fraud Detection

√ Insights for Audit Committees and Investors

- Respondents in high proportion wanted integration of technology in audit process.

- 47% of the respondents agreed that guidance on crypto currency is required; 54% opined that guidance on valuation of data for business combination and subsequent impairment testing was needed.

- Audit firms are getting ready with plan/ strategy to address pertinent issues related to digital accounting and assurance.

- Respondents echoed that auditors required specialized technological skill set which should be developed through an appropriate training.

- Respondents envisaged that there will be huge impact of technology on business models as well as composition and structure of audit teams.

SURVEY PARTICIPANTS PROFILE

Digital Accounting and Assurance Online Survey 2017 received 920 responses from chartered accountants. This report provides a brief summary of the overall results as well as a breakdown by region and size of practice.

- The largest groups of respondents by practice size were from accounting firms with 1- 10 partners (88.86%) followed by firms with 11-20 partners (4.68%).

- Western Region of ICAI (33.18%) has the largest representation in the survey followed by Southern Region (23.39%). Northern Region (18.49%) and Central Region (16.26%) were also well represented. Eastern Region (8.69%) had a lower representation.

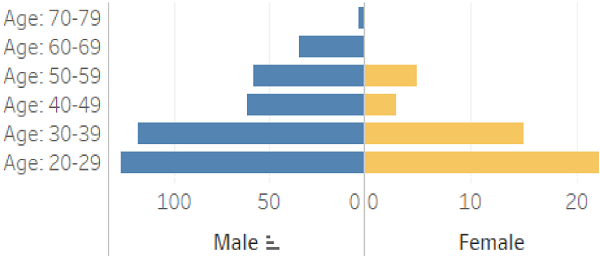

- Male respondents (89.98%) were almost 9 times as compared to female respondents (10.02%). Female representation was maximum in Western region.

- Age group analysis of respondents showed that the majority of the respondents were below 40 years of age.

Note that, for simplicity, the percentages in some tables and charts are rounded, and totals may therefore not tally to 100.

Respondents by Practice Size

Respondents by Region

Respondents by Gender

Gender diversity by Region

Gender diversity by Age Group

ANALYSIS OF RESPONSES

Section I –Technology Trends

Please grade following technology trends which will impact the profession significantly in next 3-5 years as H ( High), M ( Medium) or L ( Low)

1. Artificial Intelligence

2. Big Data

3. Robotics

4. Digital Service Delivery

5. Cloud

6. Internet of Things

> Respondents rated the extent to which six emerging technologies, viz., Artificial Intelligence, Big Data, Cloud, Digital Service Delivery, Internet of Things, and Robotics, > would impact their professional practice over the period of next five years.

> It can be drawn from the survey that all the six technologies except robotics is perceived to have a high impact on the accountancy profession.

> This inhibits a positive response from the respondents, and the profession needs to constantly innovate to embrace these technology tools as it is going to rapidly play an important role over the next few years.

> Powered by these innovative technology resources and tools, it is time to strategize the profession.

Section II –Accounting Issues Warranting Guidance

Which according to you pose accounting issues warranting more guidance-

(i) Crypto currency

(ii) Valuation of Data for Business Combination and Subsequent Impairment Testing

(iii) Any other area

(1 means most urgent, 2 is urgent and 3 is not a priority for now)

This question relates to the latest accounting issues faced by the profession which are warranting more guidance. There is a mixed response from the respondents.

- Crypto currency- 47 % of the respondents stated that there is an urgent need for guidance on crypto currency, 31% stated that guidance on crypto currency is most urgent needed, while 21 % stated that it not a priority for now.

- Valuation of Data for Business Combination and Subsequent Impairment Testing- 54 % of the respondents stated that there is an urgent need for guidance on Valuation of Data for Business Combination and Subsequent Impairment Testing , 37 % stated that guidance on this topic is most urgent needed, while 10 % stated that it not a priority for now.

- Some areas warranting guidance

√ Issues related to e-commerce business profile

√ Website domain valuation and accounting

√ Digital transaction wallets and coupons transactions accounting

√ Drone based inventory and asset verification

√ Capitalization and valuation of Big Data Model or AI Assets which are internally generated

Section III– Impact on Audit Evidence

Internet Of Things (IOT) is set to revolutionise every sector/ industry. Please indicate impact of IOT on audit evidence in the following areas as H ( High), M ( Medium) or L ( Low) –

1) Fixed Asset Verification

2) Inventory Tracking

3) Provisioning for say Warranties based on quality of tickets for the equipments

4) Any other area

Almost 90% of the respondents have stated that Internet of Things (IOT) will have an impact on audit evidence ranging from high- medium, while mere 10% respondents represents a low impact on the audit evidence related to the following items :

- Fixed Asset Verification- 47% of the respondents stated that IOT will have a medium impact on the audit evidence related to fixed asset verification. 44% considered to think otherwise and were of the view that it will have a high impact, while only 9% stated it as a low risk. Majorly respondents believed IOT to have high- medium impact on audit evidence in fixed asset verification.

- Inventory Tracking- Almost 75% of the respondents have stated that IOT will have a high impact on audit evidence in inventory tracking, 24% have responded that it will have a medium impact and 2% considered it as having a low impact.

- Provisioning for say, Warranties based on Quality of Tickets for the Equipments- 51% of the respondents stated that IOT will have a medium impact on the audit evidence related to provisioning for warranties. 40% considered to think otherwise and believed that it will have a high impact, while only 9% stated it was a low risk. Majorly respondents believed IOT to have high- medium impact on audit evidence in provisioning for warranties based on quality of tickets for the equipments.

Section IV–Incorporating Data Analytics Into Audit Process

Are the below issues important for incorporating data analytics into the audit process. Please indicate your response as H ( High), M ( Medium) or L ( Low) –

(i) Connecting Data Analytics to the existing suite of auditing standards

(ii) Recognizing its use as a tool for improving audit sampling

(iii) Understanding nature of audit evidence derived from use of data analytics software

(iv) Customization of off-the-shelf- data analytics software

(v) Other- please specify

More than half of the respondents reported that it is important for incorporating data analytics into the audit process to address the following issues:

- Connecting Data Analytics to the Existing Suite of Auditing Standards- 62 % of the

respondents stated that it is highly important. 35% believed it to be of medium importance, while only 3 % believed that it is less important to address this issue presently. Overall respondents echoed the need for connecting data analytics into the existing suite of Auditing Standards. - Recognizing its use as a tool for improving Audit Sampling- 69 % of the respondents stated that it is highly important. 29 % believed that it is of medium importance, while only 2 % believed that it is less important to address this issue for incorporating data analytics into the audit process.

- Understanding Nature of Audit Evidence derived from use of Data Analytics Software- 68 % of the respondents stated that it is highly important. 31 % believed it was of medium importance, while only 1 % believed that it was less important to address this issue for incorporating data analytics into the audit process.

- Customization of off-the-shelf Data Analytics Software- 49 % of the respondents stated that it is highly important. 45 % believed it carried medium importance, while only 6 % believed that it was less important to address this issue for incorporating data analytics into the audit process.

Following are some other issues stated by the respondents as important for incorporating data analytics into the audit process-

- Development of suitable audit trails and tools considering new IT developments

- Testing the accuracy of big data and compilation of data for statutory compliances

- Measuring even the qualitative aspects like, monitoring internal controls

- Authentication Mechanism for the data transfers prior to the analytics

- Security of cloud data

Section V–Propelling Innovation in Accounting and Assurance

Do you think artificial intelligence/ machine learning will propel innovation in accounting and assurance? Please indicate your response as H( High), M( Medium) or L( Low)-

(1) Deliver Real time insights

(2) Continuous Control Monitoring Systems

(3) Enhance Decision Making

(4) Catapult Efficiency

(5) Other- please specify

More than half of the respondents reported that Artificial Intelligence (AI) as a technology will play an important role in innovation by eliminating the manual process in accounting and assurance sector. Perceived benefits are as follows-

- Deliver real time insights- 60% of the respondents believed that through AI real time reporting can be achieved as compared to traditional practices.

- Enhanced decision making- More than 50% of the population has stated that AI will have high impact in decision making while only 6% believed it to have a low impact.

- Continuous control monitoring system- 66% respondents stated that AI will have a high impact on continuous control monitoring system, while 32% stated that it will have a medium impact.

- Catapult efficiency- Respondents had a mixed view ranging as 46% as high impact and 45% as medium in achieving efficiency through AI, while only 8% perceived that it will have a low impact.

Section VI –Use of Data and Technology in Audit

Do you think that use of data and technology could affect following areas. Please indicate your response as H ( High), M ( Medium) or L ( Low)-

(1) Nature and Extent of Audit procedures

(2) Nature and Sufficiency of Evidence

(3) Risk Assessment

(4) Internal Control Over Financial Reporting

(5) Fraud Detection

(6) Insights for audit committees and investors

More than half of the respondents stated that increase in volume of data and use of technologies will have high affect/ impact on the following areas mentioned below:

- Nature and Extent of Audit Procedures- 73 % of the respondents stated that it will be highly affected. 25% believed that it will have a medium impact, while only 2 % stated that data and technologies will have a low affect on nature and extent of audit procedures.

- Nature and Sufficiency of Evidence- 66 % of the respondents stated that it will be highly affected. 30% believed that it will have a medium impact, while only 4 % stated that data and technologies will have a low affect on nature and sufficiency of evidence.

- Risk Assessment- 70 % of the respondents stated that it will be highly affected. 27 % were of the opinion that it will have a medium impact, while only 3 % stated that data and technologies will have a low affect on risk assessment.

- Internal Control Over Financial Reporting- 65 % of the respondents stated that it will be highly affected. 31% perceived that it will have a medium impact, while only 4 % stated that data and technologies will have a low affect on ICFR.

- Fraud Detection- 69 % of the respondents stated that it will be highly impacted. 25 % believed that it will be having a medium impact, while only 5 % stated that data and technologies will have a low affect on fraud detection.

- Insights for Audit Committees and Investors- 48% of the respondents stated that it will be highly affected. Similarly, 45 % were of the view that it will have a medium impact, while only 6 % stated that data and technologies will have a low affect on insights for audit committees and investors.

Section VII –Integration of Technology In Audit Process

Please rate as H (High), M (Medium) or L (Low) the following factors regarding decision on integrating technology in audit process-

(1) Software cost

(2) Technology capabilities of audit staff

(3) Training cost

(4) Making the audit process more efficient

(5) Audit committee/ Senior management support

More than half of the respondents reported that the following factors mentioned below required high consideration regarding decision on integrating technology in audit process-

- Software cost – 59 % of the respondents stated that software cost has high relevance for decision making on aspect of integrating technology in audit process. 37 % perceived as having medium importance, while only 4% stated it is not of much importance right now.

- Technology capabilities of Audit staff- 64 % of the respondents stated that high decision making is required for upgrading technology capabilities of audit staff, for integrating technology in audit process. However, 32 % perceived it as a factor of medium importance, while only 4% stated that it is not of much importance.

- Training cost- 48 % of the respondents stated that training cost required high decision making for integrating technology in audit process. 47 % perceived it as a factor of medium importance, while only 5% stated that it was of not of much importance in the decision making process.

- Making the Audit Process more Efficient- This factor carried importance for 62 % of the respondents while making decision for integrating technology in audit process. Only 36 % respondents perceived it as a factor of medium importance, while only a small 2% considered it to be carrying a low importance.

- Audit Committee/ Senior Management- Almost equal number of respondents considered buy-in of Audit Committee/ Senior Management carrying high (48 %) and medium (47%) importance for integrating technology in audit process. Only 5% stated that this aspect carried very low importance.

Section VIII –Organizational Strategy To Address Issues

Does your organization (audit department) have a plan or strategy to address the following-

(1) Need for automated support of data mining and analysis, continuous monitoring and other technology based activities

(2) Defined technology skill sets, based on identifying gaps

(3) Ways to measure the effectiveness of technology investment, processes and activities

This question relates to whether the respondent’s organizations (audit department) have a plan or strategy to address the issues mentioned below:

- Need for automated support of data mining and analysis, continuous monitoring and other technology based activities carried importance for 61% of the respondents and they had a plan/ strategy to address. On the other hand 39% respondents currently had no plan/ strategy for the same.

- Similarly, 62% of the respondents had a plan/ audit strategy in place for defined technology skill sets, based on identifying gaps. However, 38% of the respondents denied for having a plan/ audit strategy in place for this factor related to skill set.

- 61% of the respondents have stated that they already have a plan/ strategy and 39% stated that they don’t have a plan/ strategy already in place for the ways to measure the effectiveness of technology investment, processes and activities

Section IX –Impact on Audit quality, Skill Sets of Auditors, Audit Firm Structure

Please share your views on following aspects –

(i) How audit tools may be leveraged to improve audit quality and protect investors?

(ii) How this trend will affect the skill sets required by auditors?

(iii) What impact will technology trends will have on the composition and structure of audit teams and the business model of the firms?

(i) Leveraging Audit Tools to Improve Audit Quality and Protect Investors

Respondents agreed that audit tools and specifically CAAT are the need of the hour for every accounting firm. Views on aspect of leveraging audit tools to improve audit quality and protect investors are as follows-

- Use of audit tools can provide filtered information and better insights for effective decision making, early fraud detection, lapses in disclosures, etc.

- Increased coverage of data for analysis will lead to higher degree of assurance.

- Comprehensive guidance is required to the audit team for executing audit by using audit tools.

- Artificial Intelligence should be integrated with decision making skills.

- Standardization of audit tools will enable greater acceptance and adoption.

- Audit tools will help to focus on important and risk oriented areas, thereby saving time and cost.

- Audit tools should be leveraged based on specific industry requirements.

(ii) Digital Trends Affecting Skill Sets Required By Auditors

Respondents echoed that auditors required specialized technological skill set which should be developed through an appropriate training. Major views are as follows –

- Auditors need to update their skills so that there is more focus on qualitative areas like, analysis, problem solving, etc.

- Auditors should develop their skills on latest technologies lie Big data, Artificial Intelligence, Block chain, etc.

- Data mining skill set will be essential requirement for effective audit.

- Enormous knowledge sharing is required among various accounting firms.

- ICAI should include relevant topics in the syllabus to well equip future members of the profession.

(iii) Impact of Technology Trends on Composition, Structure of Audit Teams and Business Models of the Firms

Respondents agreed that there will be huge impact of technology on business models as well as composition and structure of audit team. Some pointers were-

- Technology will replace the routine audit process, going forward the accounting firm’s structure will be leaner.

- Technological changes will make existing accounting firms more productive and efficient.

- Future models of the firms should be developed and evolved based on the analytical tools available in the market.

- Audit firms will have to invest more in technology tools.

Section X –Change in Demand of SMP Services in Future

How do you expect demand for following services provided by SMPs to change in the future?

(i) Client Accounting Services (Business Process Outsourcing/ Accounting/ Virtual CFO)

(ii) Business Advisory (data analysis, etc.)

(iii) Audit and Assurance

(iv) Tax (including planning and advice)

(v) Other- please specify

Small and Medium Practitioner’s (SMPs) are critically important fraction of the accounting profession. Demand for services provided by the SMPs will be surely impacted by digitization in the near future. Responses on impact of following services rendered by the SMPs are as follows –

- Client Accounting Services (Business Process Outsourcing/ Accounting/ Virtual CFO) – 86 % of the respondents have stated that there will be an increase in Client Accounting Services (Business Process Outsourcing/ Accounting/ Virtual CFO) over the coming years and 14% respondents were of the view that there will be a decrease in demand of these services.

- Business Advisory (data analysis, etc.) – 92% of the respondents have stated that there will be an increase in Business Advisory (data analysis, etc.) over the coming years and 8% have stated that there will be a decrease in the mentioned service.

- Audit and Assurance – 75% of the respondents have stated that there will be an increase in audit and assurance services provided by SMPs over the coming years and 25% have stated that there will be a decrease in the mentioned service.

- Tax (including planning and advice) – 77% of the respondents have stated that there will be an increase in taxation services, including planning and advice, over the coming years and 23 % have stated that there will be a decrease in the mentioned services.

DIGITAL ACCOUNTING AND ASSURANCE BOARD OF ICAI

To unravel the impact of Digitization on Accounting and Assurance, the Council of ICAI has constituted the Digital Accounting and Assurance Board (DAAB), as a non-standing Board of

the ICAI, for fostering a cohesive global strategy on aspects related to digital accounting and assurance, through sharing of knowledge and practices among st the members. DAAB is endeavored to identify, deliberate and highlight on issues in accounting (including valuation) and assurance (including internal audit) issues in the digital world. Digital Accounting and Assurance Board is focusing on issues in accounting and assurance arising from the high pace of digitization, including use of artificial intelligence in audit, big data analytics in audit, relevance of sampling, valuation of data as an asset, impairment, testing of digital assets, insurance of data-valuation and premium fixation, etc.

The Board is taking up initiatives to develop knowledge base through position papers and articles on issues related to impact of technology on accounting and assurance. DAAB Knowledge Page https://www.icai.org/new_post.html?post_id=13422&c_id=432 may be referred for position papers issued and for links to relevant article on digital accounting and assurance. Technology Summits are being conducted with the theme of Empowering Chartered Accountants in digital era. DAAB has also released knowledge management videos

available on ICAI Mobile App https://www.icai.org/mobile/ .

DIGITAL ACCOUNTING AND ASSURANCE BOARD

TERMS OF REFERENCE

(Board for deliberating and initiating solutions for Accounting (including valuation) and Assurance (including internal audit) issues in the Digital World)

Arising out of digital era and its consequences –

(a) to identify, deliberate and highlight issues in Accounting (including valuation) and Assurance (including internal audit) in the Digital World, and security aspect of data and technology;

(b) to act as a facilitator by engaging through relevant committees of ICAI; and wherever necessary with standard setters, Government, Regulators, industry and other accounting bodies in the world; and suggest to the relevant Committee(s) in Institute, the required changes in Accounting Standards, Assurance Standards and Valuation Standards;

(c) to develop knowledge base through position papers, create on line platform, including an annual conference/ round table preferably, on areas identified with a view to raise awareness in all stakeholders, the issues and opportunities arising from these trends; and

(d) to enable setting up a Global Digital Accounting and Assurance Board, as India initiative so that ICAI gets recognition as the global thought leader in Accounting and Assurance in digital world.

Composition of Digital Accounting and Assurance Board 2017-18

Council Members

CA. Anil Satyanarayan Bhandari, Member

CA. Atul Kumar Gupta, Member

CA. Debashis Mitra, Member

CA. Kemisha Soni, Member

CA. Manu Agarwal, Member

CA. Nilesh S. Vikamsey, President, ICAI (ex officio)

CA. Naveen N.D. Gupta, Vice President, ICAI, (ex officio)

CA. Prakash Sharma, Member

CA. Sanjay Vasudeva, Vice-Chairman

CA. Shiwaji Bhikaji Zaware, Member

CA. Shyam Lal Agarwal, Member

CA. M P Vijay Kumar, Chairman

Government Nominee

Shri Vithayathil Kurian

Co-opted Members

CA. Adesh Kumar Gupta

CA. B K Patel

Special Invitees

Shri G Raghuraj, nominee IDRBT

CA. Hemant Joshi

Prof. Naman Desai, nominee IIM- Ahmedabad

Ms. Narmadha R, nominee C&AG

CA. Subh Ghosh

Shri T Chakravarti, nominee SEBI

Digital Accounting and Assurance Board

The Institute of Chartered Accountants of India

www.icai.org